Please rotate your device

We don't support landscape mode yet. Please go back to portrait mode for the best experience

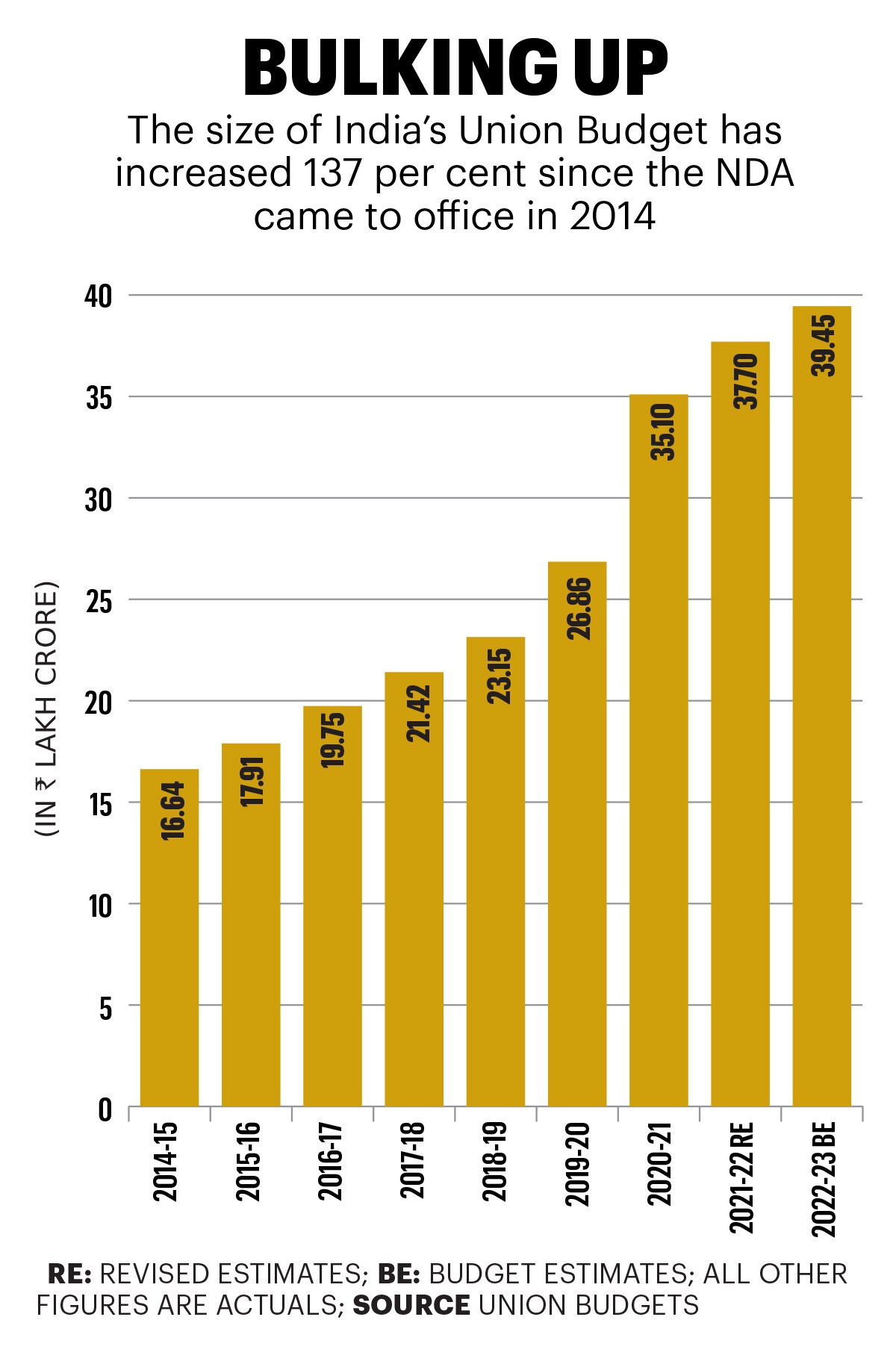

It is that time of the year again. The time of the Union Budget. The time for Finance Minister Nirmala Sitharaman to announce the accounts of the Government of India. And the time for Prime Minister Narendra Modi’s unmistakable touches in economic and social strategy to peep through the pages of the FM’s Budget speech. This time, there’s an added dimension—February 1, 2023 will see the last Budget of the current BJP-led National Democratic Alliance (NDA) government before the next parliamentary elections in 2024. Historically, such occasions have seen governments announce an array of sops to please different sets of vote banks.

Such a picture is unlikely to be painted this time. For one thing, despite some shifts in political alignments and the BJP’s not-so-impressive performance in some state elections, no real opposition force seems to have evolved to a point to pose a serious challenge to a dominant NDA government at the Centre, led by a still-very-popular Prime Minister. For another, while India’s economy is doing well—the fastest-growing major economy in the world, no less (in the G20, only Saudi Arabia is growing faster)—several headwinds are blowing vigorously, and would serve to thwart any adventurist possibilities.

Narendra Modi

Prime Minister

India

Resilient is the word being used to describe the country’s current economic footing, even as the developed world goes through major convulsions—war in Ukraine and consequent mass migration, jobs and lives lost, and rising supply chain pressures; high inflation in the US, the UK and other developed economies; the return of Covid-19 in China and some western countries; the real possibility of softened prices of crude oil and other commodities spiking again; and some others. Naturally, such global tremors would not leave India untouched.

While India’s current economic growth is looking good in the face of these headwinds, there are unmistakable signs of long-term growth slowing down. Plus, because of inflation, the subsidy bill for fuel, fertiliser and food has shot up big-time, and the increasing trade deficit because of crimping exports is hurting. Then, the post-pandemic consumption boom due to pent-up demand is now at the end of its tether. And the return of Covid-19, although not predicted to hurt India too much, is another factor the government will consider as it works out its allocations and spending thrust for the next fiscal.

But there’s one big, bright spot. The government’s coffers are looking better than before—it expects an additional Rs 3-3.5 lakh crore in tax collections this fiscal. Apart from helping keep the fiscal deficit (difference between a government’s total revenue and total expenditure) under control, it would also allow some manoeuvring room to the FM for spending in key areas, including infrastructure and social spends. More revenue-generating moves might also be in the offing to reduce the pressure on tax collections to fund the fiscal deficit.

Nirmala Sitharaman

Finance Minister

India

So, what would be the big thrust areas of Budget 2023-24? “The government brought 35 per cent jump in capital expenditure [in the previous Budget], largely on infrastructure. I would think it would want to continue that,” says Sanjay Kumar, Partner at Deloitte India. “Another good thing is that capex is going up and revenue expenditure as a share of Budget is coming down. That according to me is the right way to proceed on any national budget.” Ranen Banerjee, Partner and Leader-Economic Advisory Services, PwC India, says that growth and jobs are the top priorities for the government, and whatever additional revenues are generated would likely be spent on further capex. “It not only adds infrastructure, but also adds jobs. Construction is the fastest job generator,” says Banerjee, adding that he expects lots of support for another job-generating engine, the MSMEs, and for the agricultural community. “The allocations may go more towards programmes and schemes that can be completed within the next year.”

GROWTH, GROWTH, GROWTH

The top priority before the government is to steady India’s slowing GDP growth. In 2016-17, GDP grew 8.3 per cent, and the next three years saw that sliding to 8 per cent, 6.5 per cent and 3.7 per cent, respectively. In FY21, GDP contracted 6.6 per cent because of Covid-19, and bounced back to a strong 8.7 per cent in FY22. This was partly because of the contracted low base of FY21, bur more because of the explosion of pent-up demand after the lockdowns got over, with the absolute GDP reaching a record Rs 147.4 lakh crore (approximately $1.84 trillion). But in FY23, growth is expected to moderate. India’s National Statistical Office (NSO) predicted 7 per cent GDP growth in FY23, while other agencies have predicted anything between 6.5 and 7 per cent. And while the NSO has pegged FY24 growth at 6 per cent, others have largely kept it around 5 and 6 per cent. Nomura’s estimate, for instance, is 5.1 per cent.

The global numbers, expectedly, are uncomforting. The World Bank expects global GDP growth to slow to 1.7 per cent in 2023—the lowest since the 2008 economic crisis—and the developed economies to grow just 0.5 per cent in 2023 (compared to 2.5 per cent in 2022). And the WTO expects global trade to grow just 1 per cent in 2023, compared to 3.5 per cent in 2022.

Enterprises invest when they reach capacity or see an opportunity. We just need simple laws, ease of doing business, etc.

Nadir Godrej

MD

Godrej Industries,

Chairman

Godrej Agrovet

What steps can the FM take in Budget 2023-24 to support growth and spur demand in such a situation? “In the backdrop of a global growth slowdown and geopolitical uncertainty, ICRA anticipates that the FY24 Union Budget will focus on supporting domestic economic growth, with a continued impetus towards infrastructure and capacity development,” says Aditi Nayar, Chief Economist at ICRA Ratings. “We expect a double-digit hike in capex to Rs 8.5-9 lakh crore. Given the relatively higher multiplier of such spending, this would play an important role in supporting investment demand and, thereby, growth.”

While the capex push has held up economic growth to a large extent, the fact is that the demand that is generated—for materials, jobs, etc.—is through government push, and not organic demand through industry expansion. “You have to get back to a revival of private investment if you want to see sustained growth in India,” says Ajay Chhibber, Senior Visiting Professor at Indian Council for Research on International Economic Relations (ICRIER). “That can only happen with a reasonable current account deficit (CAD), if the fiscal consolidation is done. We cannot sustain a CAD of 3 per cent of GDP; the markets will not allow it because India will appear much too risky then.”

Explaining that private investments comprise both corporate and non-corporate (such as construction, real estate, etc.), he says non-corporate investments are likely to be driven by more public spending in infrastructure. As for corporate investments, as Nadir Godrej points out, enterprises invest when they reach capacity utilisation or see an opportunity, and they don’t need much encouragement from the government. “We just need simple laws, ease of doing business, and so on,” says the MD of Godrej Industries and Chairman of Godrej Agrovet, adding that while there has been some improvement in ease of doing business, more needs to be done.

The government needs to up the quantum of credit guarantees for infrastructure projects... It will make private investors more comfortable

Arindam Guha

Partner, Leader–Government & Public Services

Deloitte India

PwC’s Banerjee is hopeful of private capex coming in in FY24, because corporates are deleveraged, and so have the capacity to invest. Plus, he feels that in Q1 of FY24, corporates will start to invest because people will start talking about greater growth in FY25. “The gross fixed capital formation (GFCF, an indicator of investments in an economy) will continue to be boosted by the government next year also, and an addition delta will come in from the private sector capex,” he says. So, there is an increasing view that the government must bring in policies and incentives to attract more private capex in infrastructure. Deloitte’s Kumar says financial institutions like pension funds could be urged to put their corpus into infrastructure projects. “People can get better returns and with more assurance,” he says.

Regulatory challenges and procedural delays have made several private companies give up on infrastructure investments—even ongoing projects—over the years. Experts feel conscious and concrete action needs to be taken on these fronts to attract more private capital. Arindam Guha, Partner, Leader–Government & Public Services, Deloitte India, says the government needs to up the quantum of credit guarantees for infrastructure projects. “The only prominent credit guarantee mechanism is through the IIFCL (India Infrastructure Finance Company Limited). If you look at their performance in the last three-four years, it is not even in the thousands of crores, vis-à-vis an NIP (National Infrastructure Pipeline) investment which we know is significant,” says Guha, adding that many other countries have much higher credit guarantees. “It will make private investors more comfortable. The moment you have guarantees on loan repayments subject to specific clauses, the credit quality of projects goes up.”

The infrastructure build-up will need to be backed by world-class logistics infrastructure and processes. “Last year’s Budget for the transport and logistics sector was a defining moment because of the PM GatiShakti [National Master] Plan. The Budget had also proposed a unified logistics interface platform for data exchange among various operators via APIs to achieve regulatory and operational streamlining,” says Zaiba Sarang, Co-founder of iThink Logistics, an e-commerce shipping solutions company, while pointing out that the logistics sector accounts for approximately 14.4 per cent of India’s GDP, and is expected to have a market value of $380 billion by 2025. “During the NLP (National Logistics Policy) launch, it was stated that the logistics sector costs approximately 14 per cent of India’s GDP, and that the goal of this initiative is to reduce the cost to a single digit. As a result, the Budget for this year will aim to reduce the cost of logistics by introducing new subsidies and other initiatives.”

While unveiling the NLP last September, PM Modi had mentioned that India’s logistics costs were double that of developed economies and they needed to be brought down. NLP’s four key platforms—Integration of Digital System (IDS), Unified Logistics Interface Platform (ULIP), Ease of Logistics (ELOG), and System Improvement Group (SIG)—would integrate data from seven ministries to provide real-time information about cargo movement, and make it easy for logistics companies to connect with the government to resolve any challenges. “Infrastructure development for logistics across highways, warehouses, and ports should continue to be given high priority by the government in the Union Budget,” says Yogesh Patel, CFO of Mahindra Logistics. “The Budget should provide sufficient funding for several initiatives across the logistics ecosystem, as defined by the NLP.” And when earlier programmes such as PM GatiShakti, Sagarmala and Bharatmala policies are used in tandem with the NLP, the resultant efficiencies are expected to ultimately result in lowering the cost to GDP for the industry.

The government understands that what agriculture is to the rural economy, real estate is to the urban economy

Dhaval Ajmera

Director

Ajmera Realty

The other, related area of focus, especially considering India’s climate change commitments as well as long-term strategy to reduce oil imports, is to create greater momentum towards alternative modes of transport such as vehicles using ethanol-blended petrol and electric vehicles (EVs). “India’s 2070 net zero commitment means the role of ethanol in coming years is only set to grow. Given this, the price at which oil marketing companies buy ethanol (from sugar and grain companies) needs to be revised upwards to ensure the momentum of investment in this sector is not lost,” says Atul Chaturvedi, Executive Chairman of Shree Renuka Sugars. “Moreover, the 20 per cent blending target of ethanol by 2025 should be revised to 30 per cent by 2030. Sugar mills should also be allowed to open petrol/ethanol pumps near their premises.”

As for EVs, with significant rise in their sales and the upbeat commentary from both the government and the private sector on its future prospects, Budget 2023-24 is expected to bolster the subsidies and allocations for the sector, including bringing in measures to boost consumer demand. “The EV industry still faces various operational roadblocks including infrastructure, high taxes, and high battery and component costs, leading to elevated EV prices. With the upcoming Budget, it is expected that the new policies designed by the government will resolve these issues,” says Ankur Khaitan, MD & CEO of TACC, a subsidiary of HEG Limited, which is setting up manufacturing capacity for graphite anodes to be used in lithium-ion batteries. Khaitan also hopes for some EV-consumer-friendly moves such as reduction in road tax for EVs, lowering of 18 per cent GST on EV conversion kits, an extension of the Rs 1.5 lakh tax deduction on interest of EV loans, etc.

FISCAL CONSOLIDATION VS NEED TO SPEND

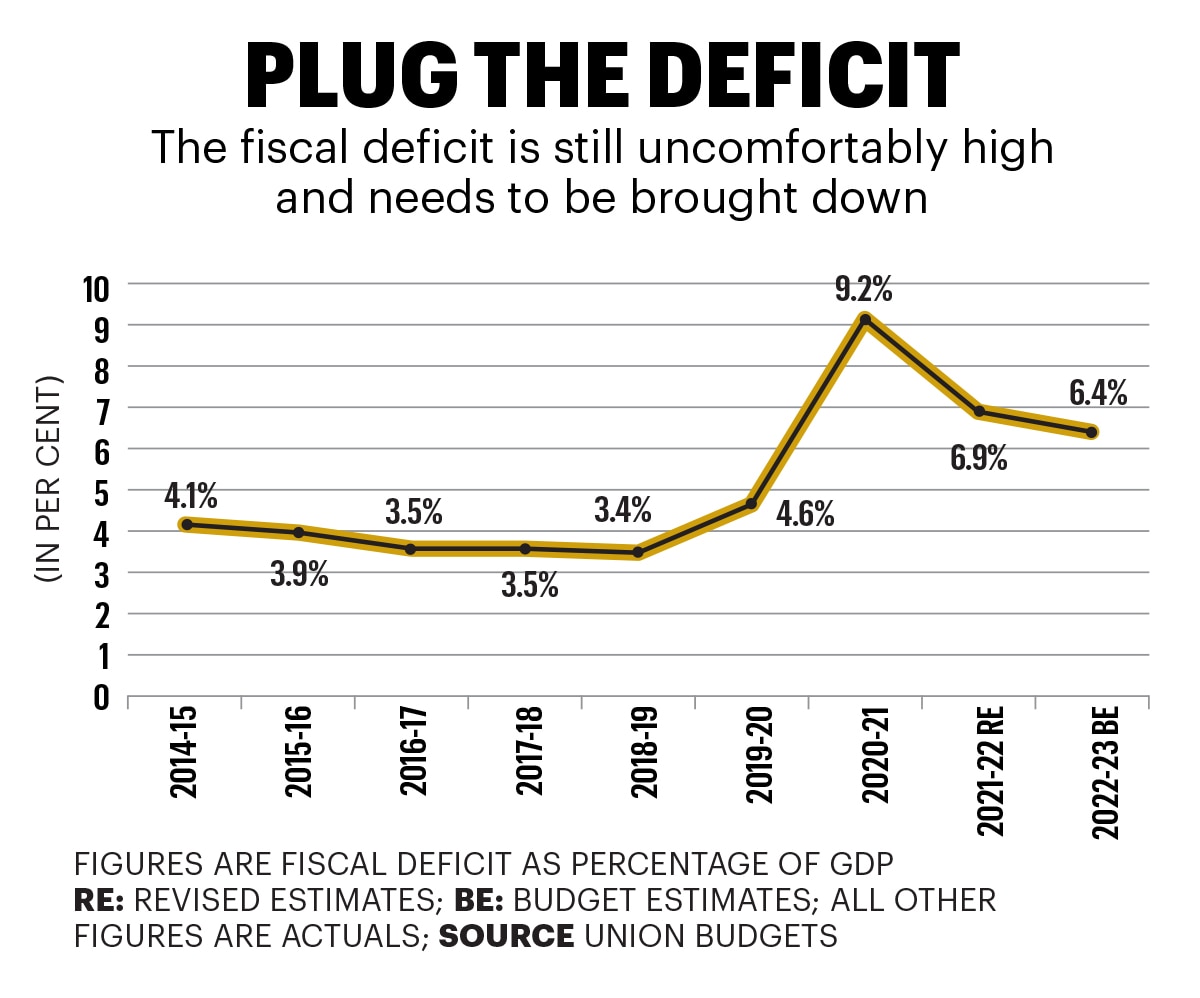

India’s tax receipts have been rising in recent years, ever since the introduction of the GST in 2017. In 2021-22, data from the Ministry of Finance shows that tax revenues exceeded the Budget estimates by Rs 5 lakh crore or 34 per cent to Rs 27.07 lakh crore. This fiscal, too, the government has publicly said it is expecting Rs 3-3.5 lakh crore in additional taxes, thanks to higher GST collections. This has several benefits. One, it helps keep the fiscal deficit under control. The deficit, which has already shrunk from 9.5 per cent in Covid-19-impacted FY21 to 6.9 per cent in FY22, is expected to fall further to less than 6.4 per cent of GDP in FY23. In fact, Goldman Sachs expects the fiscal deficit for FY23 to be 5.9 per cent. The government’s target is to bring that to 4.5 per cent of GDP by 2025-26.

But as Deloitte’s Guha points out, the deficit would be well above 10 per cent when both central and state government deficits are consolidated. That would translate to higher total public debt—estimated at 80 per cent of GDP—even though state government revenues are also climbing. Plus, falling export growth and relatively lower fall in import growth is increasing the trade deficit, which is contributing to a rise in the CAD, currently at a high 4.4 per cent of GDP in the July-September quarter. That is the highest CAD India has seen since April-June of 2013. Continuing GDP growth at around 5-6 per cent, even if it is slowing, does provide hope that the deficit will be kept under control over the next few years, with the foreign exchange reserves of the RBI, at nearly $563 billion in December 2022, providing additional succour.

Growth and jobs are top priorities for the government, and any additional revenues would likely be spent on further capex

Ranen Banerjee

Partner and Leader Economic Advisory Services

PwC India

The argument, therefore, is on the mechanism to increase revenue to fund the government’s spends, instead of borrowing. Increasing taxes is the most straightforward option, but that is not easy with elections looming on the horizon. So, what else can be done? “We expect tax buoyancy to moderate in FY23 and FY24, implying that gross tax revenue growth is likely to be in line with nominal GDP growth,” says Nayar of ICRA. “In such a scenario, the government could focus on garnering additional revenues from other sources such as asset sales and monetisation. Besides, it should also limit growth in revenue expenditure, thereby curtailing the revenue deficit, while continuing to focus on growth-supportive capex.”

Chhibber of ICRIER says that the government needs to accelerate its privatisation programme. “India has roughly $500 billion worth of capital in its public sector undertakings. About one-third is in the Maharatnas, which you can’t touch. But the other two-thirds you can accelerate. Although there have been one or two successes, mostly it has been LIC’s share sale that has brought them some money.” The other area, according to Chhibber, is to find a way to rationalise the subsidies that the government gives, such as on fertilisers and food.

Some of that intent was seen in December 2022, when the government decided to end the Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY) scheme, and instead made PDS (public distribution system), or the ration system used largely by rural people and the poor, totally free. Experts say this not only reduced the subsidy that the PMGKAY was continuing to draw, but was also a strong show of intent on the welfare front, an expected thrust with elections looming in 2024.

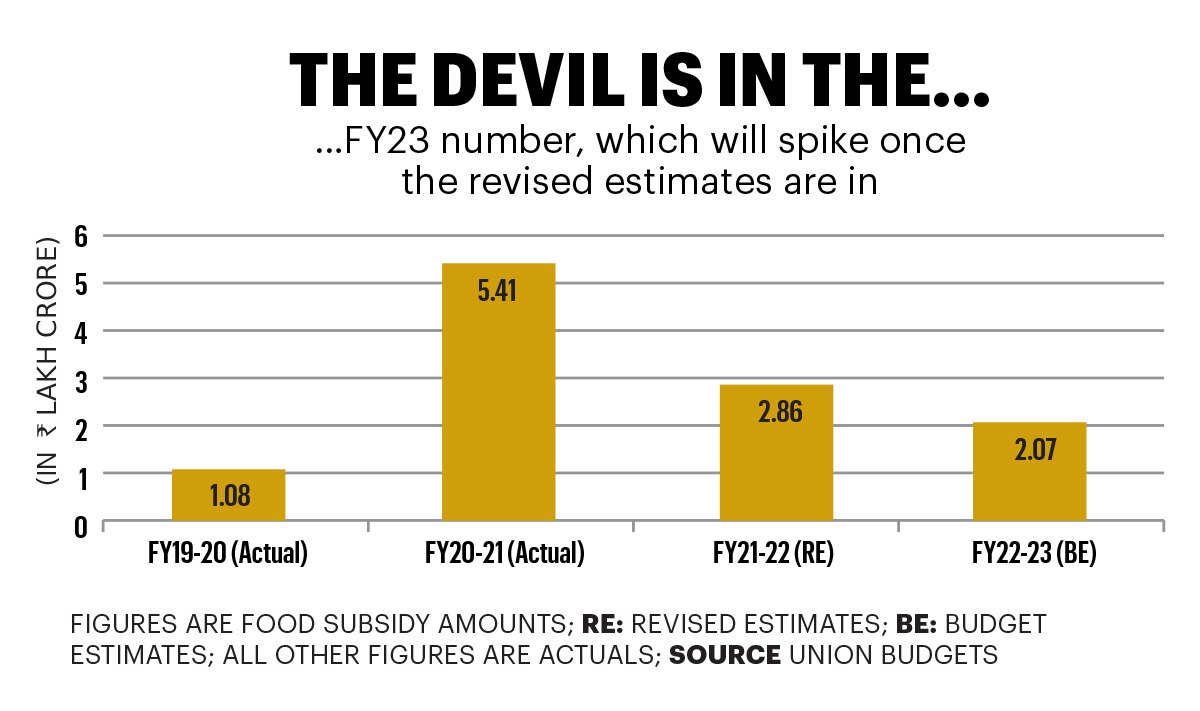

The overall subsidies in FY23—including for food, fuel and fertilisers—have shot up significantly because of inflation. In fact, he government recently had to take approval from Parliament for gross additional expenditure of Rs 4.36 lakh crore—towards various subsidies including for food and fertilisers, and the key rural job scheme, the Mahatma Gandhi National Rural Employment Guarantee Scheme or MGNREGA—of which more than Rs 3.25 lakh crore would be cash outgo, and the rest would be funded through savings of ministries or enhanced receipts. As result, the budgeted subsidy for FY23 of Rs 3.18 lakh crore—of which Rs 2.07 lakh crore is for food—is likely to shoot up big-time, perhaps even double.

An objective to reduce subsidies might seem counter-productive, when the rural markets are yet to economically recover from Covid-19 and other challenges. But Nadir Godrej says to bring back growth in rural India, it’s time to start reducing subsidies and have cash transfers. “The fertiliser subsidy is far too high now and there are new technologies coming—like nano urea, coated urea… perhaps we should only subsidise the newer technologies which require less consumption, so the burden on subsidies will be less and it will be more sustainable products.” Pointing out that both the kharif and rabi crops have been good this year, Godrej is hopeful of rural demand improving this year.

Finally, jobs are going to be critical for any government in an election year. While India’s biggest employer—agriculture—will undoubtedly be supported, the other big employment generator, real estate, is also expected to get a further push, especially in rural India. Last fiscal, the government’s flagship scheme Pradhan Mantri Awas Yojana (Gramin) received Rs 48,000 crore in allocations—Rs 20,000 crore in Budget 2022-23 and then Rs 28,000 crore through supplementary demand for grants. Under this scheme, 29.1 million pucca houses were to be built in rural areas with basic facilities such as toilets and electricity connections by March 2024. Of this target, more than 21 million houses have been constructed, and about 8 million remain as of December 2022. There is certainly a case for this to see more allocations in Budget 2023-24 to meet the final target.

Housing in urban areas, too, can generate substantial employment. “The government understands that what agriculture is to the rural economy, real estate is to the urban economy in terms of employment and the indirect impact to 227 industries like steel, cement, etc.,” says Dhaval Ajmera, Director of mid-sized Mumbai-based realtor, Ajmera Realty, pointing out that there is a need to cut the 6 per cent stamp duty on property registration to 3 per cent. “We have seen in the past that at 3 per cent, the government’s revenues are not impacted. You may be at par in terms of revenue earned, but a lot of assets will be generated, flats will get sold, you will start getting an annuity income in terms of property tax, etc.” Adds Jitu Virwani, Chairman and Managing Director, Embassy Group: "The government could consider incentivising homeowners by exempting 100 percent of the rental income up to Rs 20 lakh per annum, which would aid in increasing disposable incomes and encourage homebuyers to invest in real estate. A hike in the tax rebate on home loan interest from Rs 2 lakh to Rs 5 lakh will add momentum to housing demand." Several other sectors are also hoping for a range of incentives. Turn the page to the next article, where BT has brought you a bird’s-eye view of the expectations of a variety of industries, and read about them.

As we all wait for the Finance Minister to rise to speak on February 1, one can hope that her speech, and Budget document, will have enough to help retain India’s tag of the world’s fastest-growing major economy.

Story: Alokesh Bhattacharyya

Producer: Arnav Das Sharma

Creative Producers: Raj Verma, Nilanjan Das

Videos: Mohsin Shaikh

UI Developer: Pankaj Negi