Please rotate your device

We don't support landscape mode yet. Please go back to portrait mode for the best experience

As we unhurriedly head for the photo shoot for this article, the query comes, softly: “Do we really need to do this?” On affirmation from this correspondent, our protagonist resigns himself to his fate, and poses, hesitant and unsure, for a series of photos taken by BT’s cheery photographer. Sensing the opportunity, his communication personnel also jump into the act, happily snapping away with their phone cameras, lamenting the fact that their boss doesn’t pose for the cameras for internal events and messages. The shyness in the photo shoot is quite contrary to the interview that precedes it, where the boss takes questions with a quiet, confident calm, parrying curveballs with assured élan. Quite clearly, Dheeraj Gopichand Hinduja is more interested in focussing on his work and letting others take the limelight, a trait that comes through clearly in the interview, where he repeatedly emphasises the key role played by his people in the performance of Ashok Leyland, India’s third-biggest manufacturer of commercial vehicles (after Tata Motors and Mahindra & Mahindra or M&M) and second-biggest manufacturer of trucks (after Tata Motors).

Dheeraj Gopichand Hinduja

Executive Chairman

Ashok Leyland

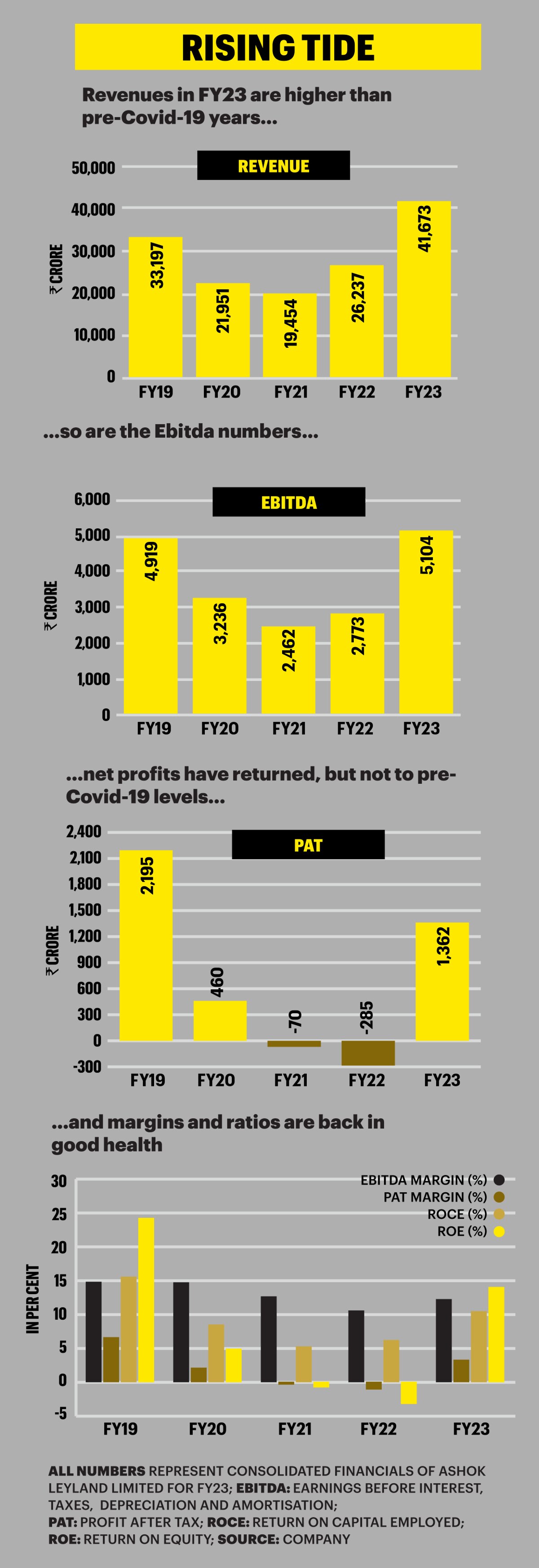

It is a performance that the 52-year-old third-generation scion of the UK-based Hinduja family, frequently ranked among the richest in the UK, can be justifiably proud of. Ashok Leyland, the flagship company of the Hinduja group that employs more than 100,000 people across several countries in a wide array of businesses, including automotive, energy, infrastructure, finance & banking, IT & ITES, media and healthcare, has just turned the corner and roared into the black, with its consolidated net profits clocking Rs 1,362 crore in FY23, after suffering losses of Rs 285 crore in FY22 and Rs 70 crore in FY21. On the way, it has had to deal with multiple challenges, including a surprising fall in demand before Covid-19, then an expected fall in demand during the pandemic amid several other bottlenecks wrought by it, and a churn in the CEO office, among other things.

There is a large segment—sub-2 tonnes—where we are not there, and it is also quite profitable. So, this is one area we have been contemplating whether we should get in or not for the past few years

SHENU AGARWAL

MD & CEO

Ashok Leyland Ltd

Ashok Leyland waged a multi-front revival strategy. “The important thing we’ve been doing, knowing that the industry goes through cycles, is to ensure that the growth momentum and the profitability of the company should not suffer. And that’s why we started diversifying into different segments like LCVs (light commercial vehicles), international operations, our parts business, defence business, power solution business,” says the mild-mannered Hinduja, a BSc (Hons) graduate in economics and history from University College, London, and an MBA graduate from Imperial College, London University. The company launched new platforms and products in the midst of the pandemic, strengthened its people practices and created a fresh programme for developing managers, widened its reach in the north and east of the country where its presence was low, strengthened its international business, created a pipeline of products for the future that would run on different fuels, and cut costs.

These moves pushed up Ashok Leyland’s vehicle volume sales by more than 50 per cent in FY23, steering the company back on the path of profitability. But even as it looks prepared for the future, Ashok Leyland needs to plug gaps in its portfolio of products, ensure a new management development programme does not wither, tackle the industry’s expected decelerated pace of growth in FY24 following two years (FY22 and FY23) of strong uptick in sales, and keep a sharp eye out for changes in the demand cycle that might impact its business.

FY21 was debilitating not only for Ashok Leyland but also for the industry. Interestingly, the slowdown came into being a year before even the pandemic, which surprised industry veterans, including Hinduja. Pointing out that the industry enjoyed a four-five year upcycle after a slowdown in FY13, Hinduja says everyone expected the boom to last till the end of FY20, given that new BSVI emission norms were to come into effect on April 1, 2020. “Everyone was feeling that this momentum would continue till March 31, 2020. But the industry started slowing down, much to the surprise of all of us,” he says. “But I would think that because we had five good years, there was bound to be this slowdown.”

We have been able to raise prices [in the current year] even as we gain market share, and that gain has not been just a number, it has been the increase in presence across the country

GOPAL MAHADEVAN

CFO And Whole Time Director

Leyland Ltd

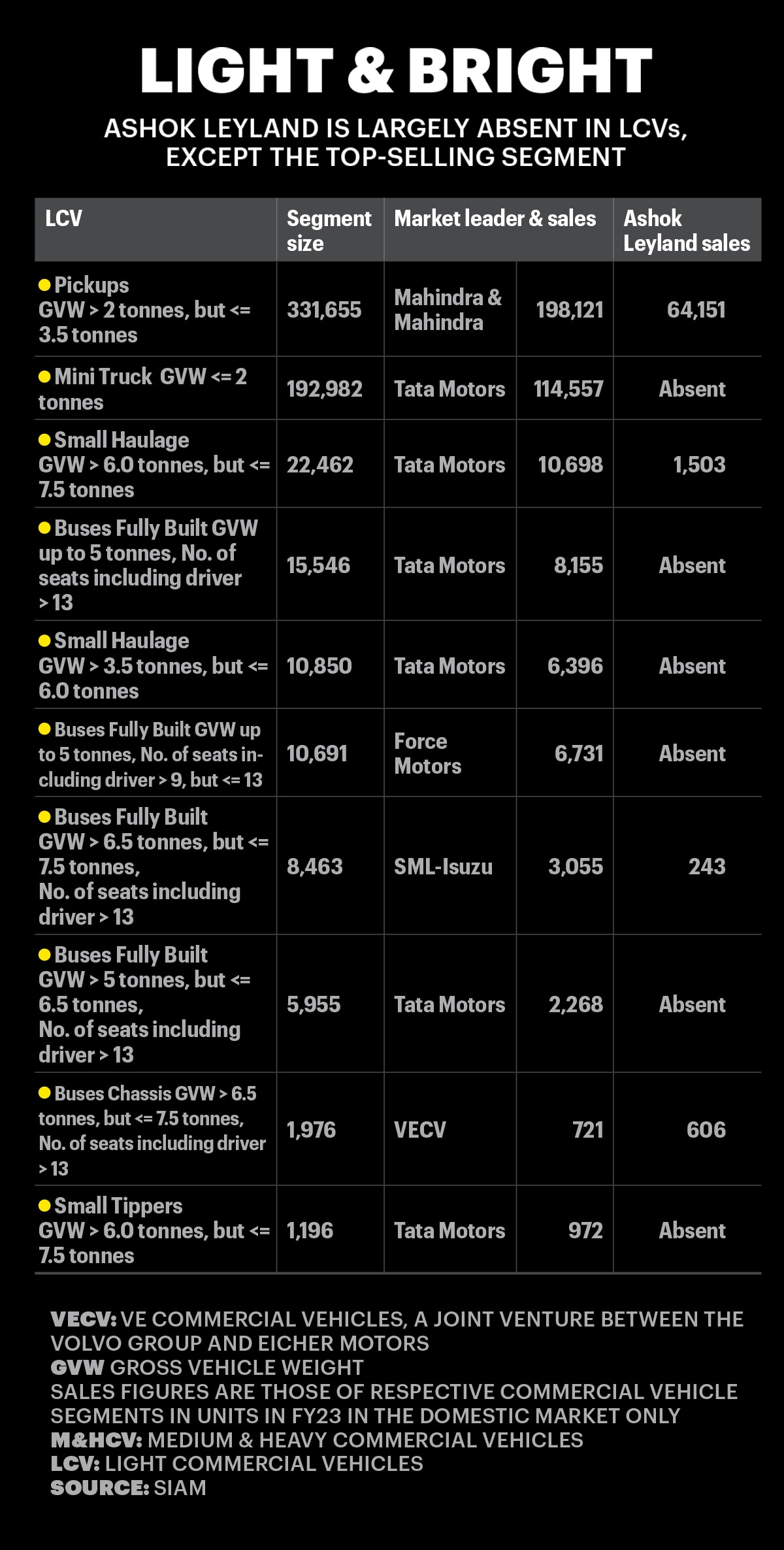

The FY20 fall actually coincided with the dip in India’s economic growth that year, when GDP growth slid to 3.87 per cent from 6.45 per cent in FY19, per data from CMIE Economic Outlook. That year, commercial vehicle sales fell 28.76 per cent, with goods carriers of all sizes, including large trucks, tippers and haulage (technically called M&HCV or medium & heavy commercial vehicles) as well as small trucks, pickups, etc. (called LCV or light commercial vehicles), bearing the brunt of the fall, plunging 47.48 per cent and 20.74 per cent, respectively. (It is pertinent to note that goods carriers comprise more than 90 per cent of India’s CV market and therefore dictate market movements.)

The FY20 slowdown rapidly degenerated into a free fall once the pandemic and the lockdowns struck. As the country went off the roads, sales of trucks, buses and smaller commercial vehicles such as pickups and even passenger carriers (buses, mini-buses, etc.) plunged like never before, sending the industry’s numbers down a further 20.77 per cent in FY21. Overall, from a peak volume sales of more than 1 million vehicles in FY19, overall CV sales had plunged by almost half to 568,559 units by the end of FY21.

The recovery since has been sharp, with volumes improving to 716,566 in FY22 and 962,468 in FY23, almost touching the peak FY19 numbers, with every possibility that the peak will be scaled next fiscal, even though growth will likely not be as spectacular. Both heavy and light vehicle categories recorded impressive growth, with M&HCV volumes growing 49.23 per cent, and LCV volumes, considering they comprise more than two-thirds of all CV sales, clocking an even more impressive 26.78 per cent. “The drivers of growth were a pickup in mining, infrastructure and construction activities, and the continued growth we have seen in e-commerce and logistics, which have resulted in very healthy utilisation of fleet levels,” says Arti Roy, Associate Director of ratings agency CareEdge, adding that on top of this, replacement demand has been improving. This rising tide has lifted all boats in the CV industry, with the industry overall growing volumes at 34.32 per cent in FY23, and majors Tata Motors and M&M clocking 21.34 per cent and 40.35 per cent volume growth, respectively.

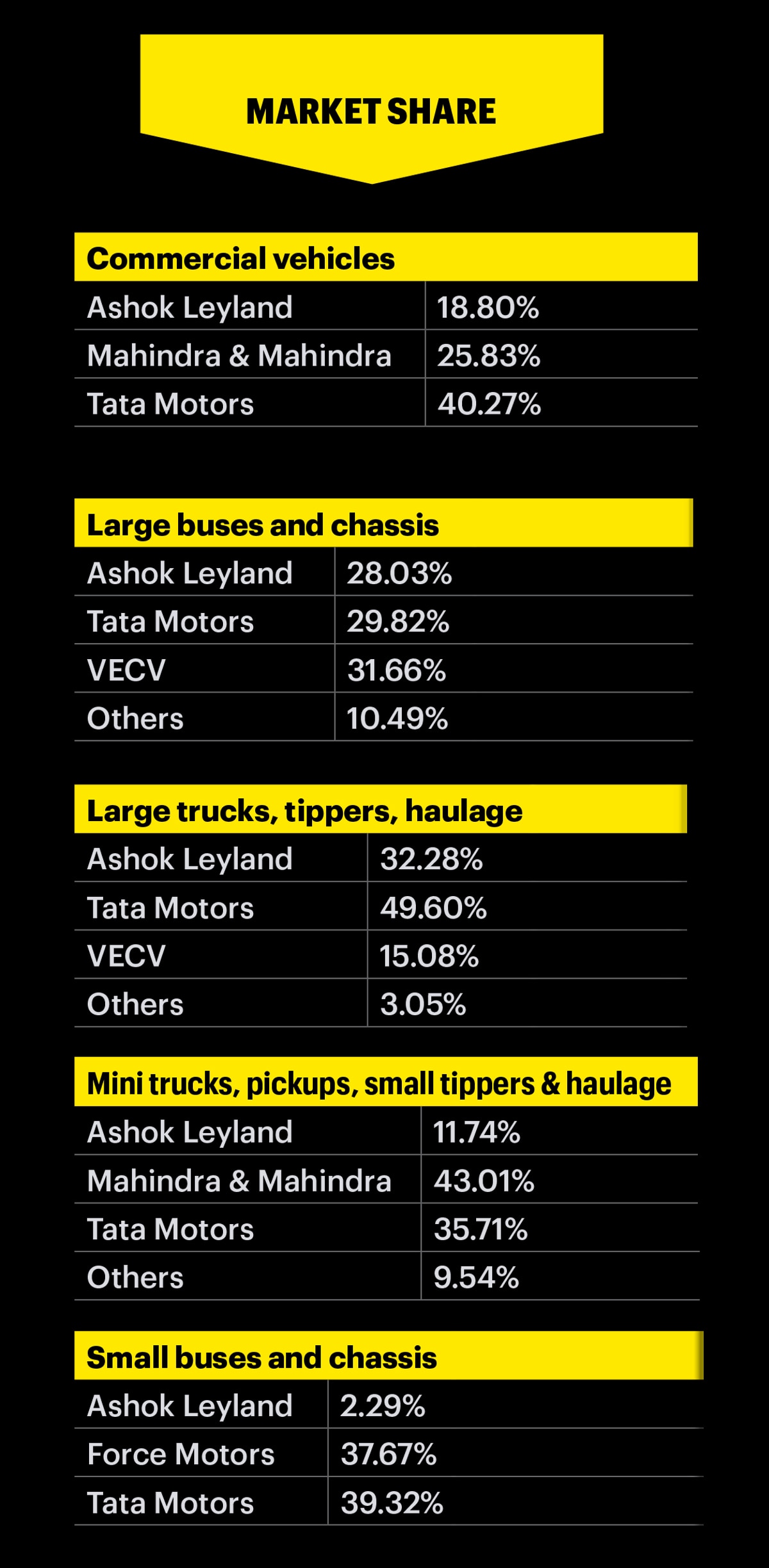

But it was Ashok Leyland that raced atop the growth peak, clocking an impressive 54.22 per cent volume growth across all segments combined. This has come on the back of an improved product portfolio both in M&HCVs, which is its traditional business, and in LCVs, where the bulk of its sales come from primarily one segment that it entered in 2012. Some bold moves helped. During the pandemic, in April 2020, Ashok Leyland introduced the AVTR range of modular trucks (customers can choose from a variety of options and virtually create a truck of their own), which helped its market share in M&HCVs climb to almost 32 per cent in FY23 from 27 per cent in FY22. And in the lone LCV segment where it performs well, it introduced the Bada Dost pickup in September 2020 to complement its smaller cousin, Dost. “AVTR has done very well, customers are extremely happy about it,” says Gopal Mahadevan, CFO and Whole Time Director of Ashok Leyland. “The [relatively low] total cost of ownership and other comfort, the drivability, the flexibility that modularity brings in, are all being felt by the customers today.”

The domestic CV industry is likely to record volume growth of 8-11 per cent in FY24... This will include muted export volumes, expected because of the global uncertainty and inflation

Arti Roy

Associate Director

Careedge

Mahadevan also points to the cost-rationalisation initiatives the company has undertaken on multiple fronts—across materials, design, sourcing and distribution—and other moves taken to strengthen the balance sheet. “One of the most important things that we have been able to do in the current year has been to raise prices even as we gain market share, and that gain has not been just a number; it has been the increase in presence across the country, which means we have gained our share of the customers’ wallet in almost all zones in the country,” he says. The company also consciously worked towards reducing its debt and has now wiped out its standalone net debt of Rs 3,289 crore in FY21 to turn cash-positive in FY23.

For the future, Hinduja says the company has prepared itself well by working on various projects for different fuel options for the future: “We’ve got Switch Mobility (a subsidiary) for electric vehicles, buses and light vehicles. We don’t know which of the alternative fuel strategies would work for the future, whether it’s hydrogen, CNG or LNG, and also which fuel type would be the most optimal in which segment. So, we’ve kept the strategy to ensure that whatever the requirements of the customer and depending on the cost of the fuel as well, Ashok Leyland should have end-to-end alternative fuel product options.” He believes the AVTR platform provides a competitive edge in this area, with the modular platform having the ability to change from pure diesel to take on cylinders for LNG, CNG, and even Hydrogen with nominal modifications.

At the same time, there are internal deliberations going on for long-term introduction of some new products, especially in some “white spaces” that Ashok Leyland faces, according to Shenu Agarwal, MD & CEO of the company. “There is a large segment—sub-2 tonnes—where Ashok Leyland is not there, and it is also quite profitable. So, this is one area we have been contemplating whether we should get in or not for the past few years,” he says. “The problem is that this market is not new, it is very mature and there are established players with significant market share. So, it’s not just the technology, but also your reach and understanding of the customer that are at stake.”

Agarwal has a point. The sub-2-tonne (GVW or gross vehicle weight) category of goods carriers is dominated by Tata Motors with popular products such as the Ace, among others. For perspective, Tata Motors sold 114,557 vehicles in this segment in FY23, which comprised almost 30 per cent of its sales, a staggering number considering the wide range and reach of Tata’s LCVs. And even in the top-selling LCV segment with GVW between 2 tonnes and 3.5 tonnes, where Ashok Leyland sold 64,151 units of Dost and Bada Dost pickups to corner 19.3 per cent share, it is up against the might of M&M with its array of pickups and a market share of almost 60 per cent. “There are more white spaces on our product portfolio, for example, from 3.5 to about 9-10-11 tonnes, even going up to 15 tonnes where we are not that strong, and that will also need some product interventions, not just market side interventions,” says Agarwal. (See infographic The Competitive World of Ashok Leyland for a more detailed analysis of its sales and white spaces.)

Going forward, the company also has strong plans for international markets. Hinduja says the company became a Top 10 player in M&HCV globally in 2018, and now after having made some progress in the LCV category, is working towards achieving the Top 10 status in CVs overall as well, which is a much more difficult ask. One part of the strategy towards achieving this objective is to create left-hand drive options for its new products including AVTR and Bada Dost, and many of its new buses as well. In fact, so well have Ashok Leyland’s buses done in the Middle East that it is now planning a second plant in the region in addition to its existing one at Ras Al Khaimah in the UAE, which was commissioned in 2011-12.

“Our products are now capable and suitable to take into markets that we play in—the Middle East, Africa, some of the Asean markets that we’re entering into. The product range that we have today gives us many new markets, many new opportunities, and you automatically attract a lot of new dealers [in those markets] as well,” says Hinduja, adding that the company needs to be able to compete with global competitors such as the Chinese, Koreans and Japanese, which trade quite strongly within these markets. “Of course, there are challenges but our price positioning is very competitive, and product offering is very robust.”

The other concern is a churn in the CEO position in recent years. Vinod Dasari, who was with the company for 14 years, quit the corner office in November 2018 and his successor Vipin Sondhi also left a couple of years later, leaving Hinduja to battle the vagaries of the pandemic without a CEO for the most part. Current CEO Agarwal joined the company last December but he has worked mostly with tractor companies earlier and has had no exposure to true-blue CVs, and is now warming up to the new job. “These things happen. When you look at the team, not only at the senior management level but at the mid-tier as well, the strength of Ashok Leyland is its people, its team. Now you might ask, why aren’t the CEOs coming from within Ashok Leyland as well? So, there might be some course correction that we need to do,” says Hinduja.

The company has now developed a new succession programme to help senior team members with their development, help middle managers chart out their career growth paths and also find youngsters who have the potential to make it to the top in the next 10-12 years. And it is the senior management team that is helming this drive. “They are working very closely in identifying the future leaders of this company and they are very involved in their development as well,” says Hinduja.

He will need all the smarts of his senior team and other managers as Ashok Leyland navigates the treacherous world of commercial vehicles in the near future. Already, Roy of CareEdge points out that the pent-up demand that drove a major part of the growth over FY22 and FY23 has now faded out, and growth will be more muted. “The domestic CV industry is likely to record volume growth of 8-11 per cent in FY24,” she says. “This will include muted export volumes, expected because of the uncertain global environment and also the inflationary concerns that are going on.” Not to forget that tough competitors like Tata Motors and M&M are also working on their own plans to sustain their growth momentum and gain more market share.

Going by its recent track record, the 75-year-old Ashok Leyland is likely to face up to these challenges bravely, and with calm fortitude. Just like Hinduja.

Story: Alokesh Bhattacharyya

Producer: Arnav Das Sharma

Creative Producers: Anirban Ghosh, Raj Verma

Videos: Mohsin Shaikh

UI Developer: Pankaj Negi