Mukesh Ambani and Gautam Adani pump in the big bucks, pushing India's scattered renewable energy industry to the next level, and hyper-fuelling the country's clean energy dreams for 2030. Nuance: India's two richest businessmen are on the same page

Please rotate your device

We don't support landscape mode yet. Please go back to portrait mode for the best experience

The headline of this story could well have been "The Great Disruptors". But even that would probably not have fully conveyed the extent of the tectonic shift that two canny industrialists have seeded within months of each other. They have not partnered. They probably won't compete directly either. Yet, the impact of their moves could serve to spark long-term change in an area of national and global interest—renewable energy as a source of electric power, with attendant benefits for our planet's environmental health. The two gentlemen in question—Mukesh Ambani and Gautam Adani, two of India's richest men, both ambitious to the point of leaving you incredulous—can sniff out a business opportunity years ahead of the curve. Co-relate the two aspects, and it would appear that renewable energy's time has truly come. It is good for the planet. It is good for business. And now, it is good business.

On June 24, addressing Reliance Industries shareholders at the company's annual general meeting, now a regular jamboree of big announcements, Ambani made public a plan to invest Rs 60,000 crore to set up four giga factories, which "will manufacture and fully integrate all the critical components of the new energy ecosystem". In some detail, the plan is to make solar photovoltaic modules, advanced energy storage batteries, electrolysers and, finally, fuel cells. The investment, he said, "will create and offer a fully integrated, end-to-end renewable energy ecosystem". Another Rs 15,000 crore is to be invested in the value chain, partnerships and future technologies. That adds up to Rs 75,000-crore ($10-billion) investments in the new energy business over three years. Ambani further said that Reliance will "establish and enable at least 100 GW of solar energy by 2030".

Gautam Adani, chairman of Adani Group, declared that his group would invest $20 billion in renewable energy over the next decade. Primarily into power generation business of solar, wind. A small part is expected to go into hydrogen power.

Mukesh Ambani, chairman of Reliance Industries, plans to invest Rs 75,000-crore ($10-billion) in the new energy business over three years. Of it, $8 billion in four gigafactories, storage of intermittent energy, production of green hydrogen, fuel cell factory. The balance $2 billion, for value chain, partnerships and future tech, including upstream and downstream industries.

In a late-night statement on November 19, Reliance said the proposed investment to be made by Saudi Arabia's Aramco in its O2C (oil-to-chemicals) business would be re-evaluated. Importantly, this has been attributed to the "evolving nature of Reliance's business portfolio". The deal, announced over two years ago, envisaged Aramco picking up a 20 per cent stake in the O2C business of Reliance.

The statement also makes a mention of Jamnagar, now the base for a major part of the O2C assets, as the centre for "Reliance's new businesses of renewable energy and new materials, supporting the net-zero commitment". The thrust on renewable energy, with this announcement, is a clear indication of a new strategy within Reliance.

Meanwhile, on September 21—three months after the Reliance AGM—Gautam Adani addressed the JP Morgan India Investor Summit and declared that his group would invest $20 billion in renewable energy generation, component manufacturing, transmission and distribution over the next decade, embellishing an already significant body of work done by the Adani Group in the past few years. With a portfolio of 25 GW (including operational and in-the-pipeline projects), Adani said this investment "puts us well on track to be the world's largest renewable power generating company by 2030". The billionaire went on to point out that of the group's current EBITDA from utilities, 43 per cent comes from the green business. "Our actions clearly indicate that we are putting our money where our mouth is: Over 75 per cent of our planned capex until 2025 will be in green technologies," Adani said.

The duo's proposed cumulative investment of $30 billion (a mammoth Rs 2.23 lakh crore) will shake up the 15-year-old renewable energy ecosystem in India, and will go across every form of renewable energy, be it solar, wind, hybrid or even hydrogen. Their paths, however, look different. Ambani's use of the world "enable" is leading most people to interpret that part of his grand plan is to be a key equipment supplier. On the other hand, Adani is already into power generation, transmission and distribution, and will continue on that path, adding more parts to the whole on the way.

Nobody is venturing into it [hydrogen energy] because of high costs and lack of an ecosystem. It is a chicken-and-egg situation

Vinay Rustagi

MD, Bridge to India Energy

Two months after Adani's talk, this November, India announced at the 26th United Nations Climate Change conference (better known as COP26) that it would put in place 500 GW of non-fossil energy capacity by 2030 (we have 148 GW as of September 2021). The estimated investment needed (see India's Hard Drive) is $260 billion or Rs 18 lakh crore, about nine times what Ambani and Adani have collectively announced. That huge gap presents a once-in-a-lifetime opportunity for others—the government and the private sector. "We see India's renewable energy opportunity to be more than 750 GW over the next two decades," says Rahul Goswami, Managing Director, Greenstone Advisors, an advisory firm with a focus on renewable energy.

Ambani and Adani have obviously seen this opportunity. Neither of the two groups responded to detailed questionnaires from Business Today.

Ambition or Audacity?

Over a period of four days this October, Reliance New Energy Solar spent $1.2 billion on three buyouts and a manufacturing deal. Two investments—Ambri and REC Group—were in the US and Norway, while Sterling & Wilson Solar was in India. Each deal gave Reliance a strategic foothold in the renewable energy manufacturing story. In investing $142 million in Ambri Inc., Reliance New Energy Solar joined Paulson & Co. and Bill Gates, apart from others. Based in Massachusetts, Ambri is exploring alternatives to lithium ion for longer-duration battery storage systems. That was followed by the other deals (see Reliance's Key Moves) that gave them a presence in manufacturing of solar modules, solar wafers and hydrogen electrolysers. Sterling & Wilson Solar was a distress sale for the overleveraged Shapoorji Pallonji Group and gave Reliance a presence in O&M (operations and maintenance) in India and global markets, too.

According to Vinay Rustagi, MD, Bridge to India Energy, a renewable energy consulting and research company, Reliance getting into manufacturing can rapidly change the dynamics. "The solar manufacturing business in India is highly fragmented with many sub-scale players operating... basically, they are module assemblers with capacities as low as 10 MW. In a scenario like this, disruption is inevitable," he says. Assuming Reliance starts production in 2024 with 20 GW annual capacity, it could hit 120 GW of production volume by the end of the decade. "With scale, they could offer integrated solar solutions to end consumers at prices far below other players. Their strong consumer connect on the back of retail and telecom offerings is going to be very helpful," Rustagi says.

To Sidharth Jain, Managing Director, MEC+, a management advisory firm specialising in renewables and cleantech, Reliance, with its manufacturing plans, is adopting a logical strategy since it is in line with the market dynamics: "They want a presence in materials, engineering and also be a serious player in the global energy market. Complementing that is its financing arm, which can be a huge differentiator."

They [Reliance Industries] want a presence in materials, engineering and also be a serious player in the global energy market

Sidharth Jain

MD, MEC+

A couple of things do stand out here. The thrust on solar is one. Plus, an "integrated, end-to-end" model is about manufacturing, with transmission or distribution of power not finding a place. An industry veteran points towards how important scale is to Reliance. "If they have to think big on renewables, being across the manufacturing chain is the way to do it," he explains.

Quiet Moves

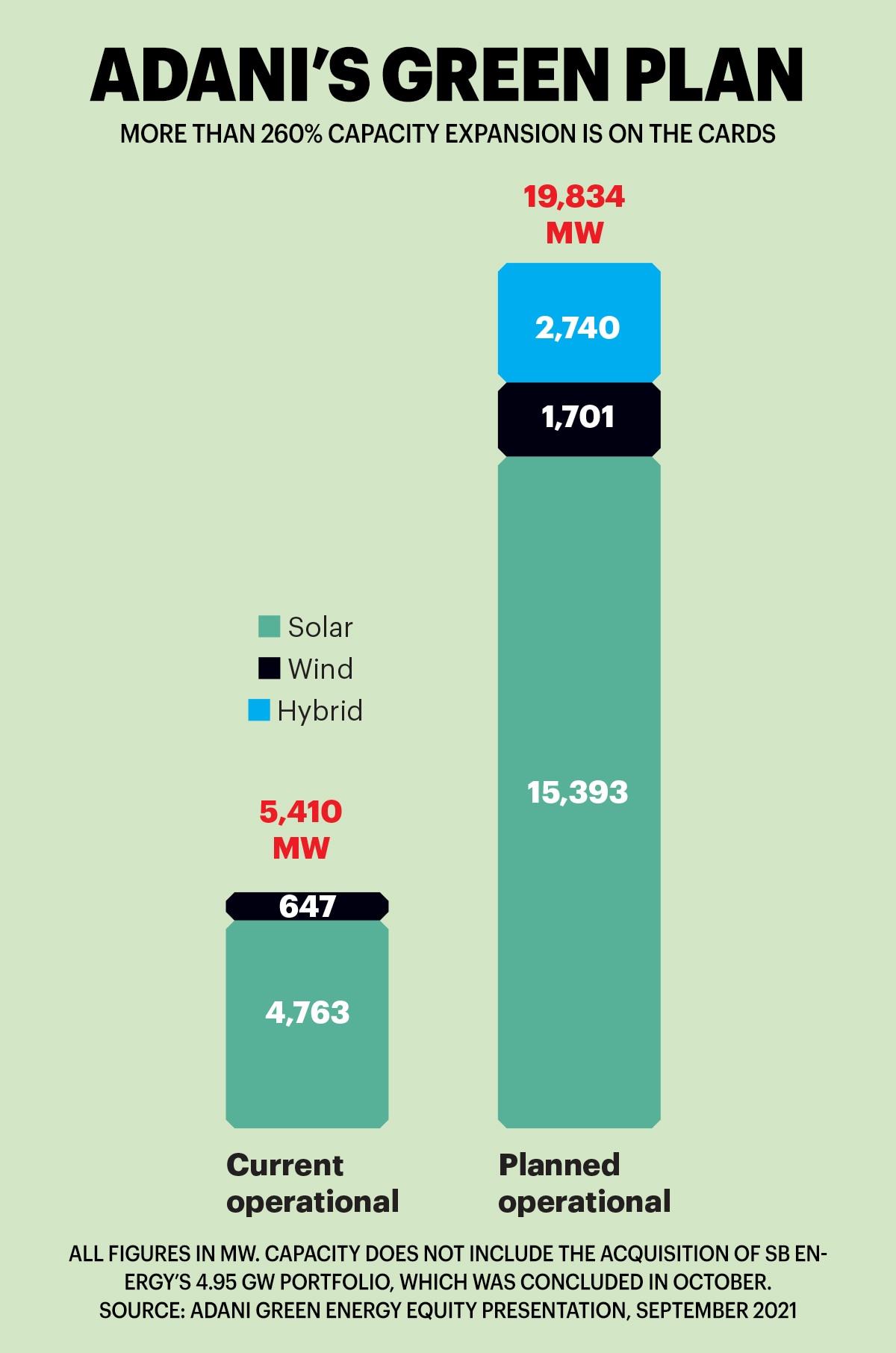

For Adani, the renewables piece takes his overall power story forward. According to an equity presentation made this September, he is sitting on a capacity of 5.4 GW, with another 13.4 GW in the pipeline, taking the total to marginally short of 20 GW. The renewable energy business is routed through Adani Green Energy (AGEL), an entity that was listed in mid-2018 after a demerger from Adani Enterprises. In October, AGEL acquired the portfolio of SB Energy (a joint venture between SoftBank Group and Bharti Enterprises) for an enterprise value of $3.5 billion, making it the largest deal in the sector. It brought to the Adani fold another 4.95 GW—4.18 GW being solar, 324 MW of wind and 450 MW, hybrid of wind and solar—taking AGEL's total capacity to over 24 GW. Smaller acquisitions include a 150-MW wind asset from Inox and 40 MW of solar from Essel Green Energy. That pace of inorganic growth has seen AGEL raising money as well.

For a cumulative fundraise of $2.5 billion, AGEL brought in French energy major Total as an equity investor with a 20 per cent holding this January, with Total also picking up 50 per cent in AGEL's operating solar assets. Apart from this, another $750 million was raised in September through the sale of green bonds to finance its under-construction projects—the deal structure allows AGEL to draw up to $1.7 billion. On November 23, the company's stock closed at Rs 1,406.95, with a market capitalisation of over Rs 2.2 lakh crore. One investment banker who has worked with the group says it is very difficult to convince investors to put in money for a traditional energy project. "Be it banks or investors, the preference is not for hydrocarbons. There is pressure from all quarters including limited partners to back green energy. Returns may not be very high but that is not of any great concern," he says.

According to experts, the next 4-5 years in the renewable energy space will be about solar and battery storage, while the next decade would be about hydrogen and fuel cells

On the anvil is a 3X increase in renewable power generation capacity over the next four years (see Adani's Green Plan). Less than a fortnight after the JP Morgan summit, Adani spoke at the TiE sustainability summit, where he said the overall organic and inorganic investments in green energy will range between $50 billion and $70 billion. "This will include investments with potential partners for electrolyser manufacturing, backward integrations to secure the supply chain for our solar and wind generation businesses, and AI-based industrial cloud-based platforms."

A senior official at a rival renewable energy company points out that Adani has been setting up its own projects and also acquiring assets such as SB Energy. "But this is not a very profitable business apart from the inherent risk of dealing with distribution companies (often called discoms and owned by state governments). Going by Reliance's initial announcements, they do not appear to be keen on this," said the official, who wished to remain anonymous.

In fact, based on public announcements and insights from industry trackers, Reliance could well remain in solar for a while. The preference is to stay away from businesses high on regulation and focus on a global market where equipment supply looks more attractive. However, Adani, by virtue of a long presence in power, operates through group companies not just in renewables but in transmission and distribution, too. A few weeks ago, it got the nod to acquire Essar Power's 1,200-MW thermal project in Madhya Pradesh.

The Bigger Picture

The excitement around renewable energy has been around for a while, but India has had its difficult moments. Many an ambitious entrepreneur came in only to realise that it was arduous to create a robust business model. Instances of people shutting shop or putting assets on the block are many. The market size was overestimated, and a combination of delayed payments and revoked power purchase agreements did the business in.

The story seems to have changed substantially but still comes with challenges. At the core of this large business opportunity is domestic manufacturing. While India is among the top 10 solar module producers globally—installed capacity of photovoltaic (PV) modules is around 16 GW apart from 3 GW of cells—the story has a few bumps. "India lags behind its biggest competitor, China, not just in module manufacturing but also in the production of other raw materials such as wafers, cells and polysilicon," says Vibhuti Garg, Energy Economist, Lead India, Institute for Energy Economics and Financial Analysis (IEEFA). "Besides, the capacity utilisation domestically is only 40-45 per cent and the estimated operational capacity is only about 7 GW." The fact is, current production capacity can meet just 35 per cent of the total domestic demand for manufacturing across the board—PV modules, cells, wafers and polysilicon among others—which also throws open a huge opportunity. "India needs to develop domestic solar manufacturing capacities and reduce dependence on imports to avoid any disruption in the future," says Garg.

India needs to develop domestic solar manufacturing capacities and reduce dependence on imports to avoid any disruption in the future

Vibhuti Garg

Energy Economist, Lead India, Institute for Energy Economics and Financial Analysis

Meanwhile, the government is also playing its part. The Ministry of New and Renewable Energy has imposed basic customs duty of 25 per cent on imports of solar PV cells and modules, which will kick in from April 2022. There is also a production-linked incentive scheme to the extent of Rs 4,500 crore for high-efficiency solar modules. "This will incentivise domestic and global players to build large-scale PV capacity here and help India leapfrog in capturing the global value chain," maintains Garg.

Gaurav Sood, CEO, Sprng Energy, a renewable energy platform set up by private equity fund Actis, agrees that some of the measures taken by the government do augur well. "It does support local manufacturing to compete with other country-based manufacturers. But it also results in increased tariffs to the end consumers," he says.

Massive investments are required in building the infrastructure for the production of competitive hydrogen and then for its storage, transportation and consumption

Gaurav Sood

CEO, Sprng Energy

With the government lending a hand on the back of a huge market, it makes sense for the big boys to come in. Goswami of Greenstone Advisors says India is in the midst of the second phase of a long-term opportunity in the sector: "This will last for several decades." He breaks down the evolution of renewable energy in India, with the first phase having smaller developers building 5-25 MW projects. "This has transitioned to a market where utility-scale projects are typically at least 50 MW in size and greater than 100 MW on an average."

And now, the two billionaires' moves are ringing in the next phase. If you can visualise fuel cells taking over the turf of internal combustion engines or hydrogen generating electricity in a cost-effective manner, the time ahead has a lot to look forward to. "Their entry into the sector signals an inflection point," says Goswami. "We are moving towards fewer, larger groups aiming to build businesses in a different league of scale than what has previously been observed in the sector. The strategies for both the groups differ but appear to focus on leveraging and creating synergies, as opposed to a sole focus on standalone solar or wind project development."

Renewable energy is at 6-8 per cent [in terms of return on equity]. For a foreign investor, it is attractive because that is more than what they make in developed markets

A. Issac George

Director & CFO, GVK Group

According to A. Issac George, Director & CFO, GVK Group (which has a presence in naphtha, thermal and hydro), the return on equity from a well-run thermal power project could be 14-16 per cent. "Renewable energy is at 6-8 per cent. From the perspective of a foreign investor, it is attractive simply because that is more than what they make in developed markets," he says. To his mind, the potential returns from renewable energy will not be commensurate with the investments that go in, and that is where big-ticket investments and patience go together. "We have to get it right on domestic production and, at the same time, the imports from China need to drop dramatically. At this point, it is clearly a wait-and-watch game," he insists. That said, George still sees an opportunity since grid stability, an imponderable in the case of solar, could augur well for gas-based projects. "It will be a fresh lease of life."

However, making a business plan with renewable energy at the centre is how most players are going about it. "Unique operational approaches such as smart grid will only create more opportunities for solar cell manufacturers and energy storage producers," explains Mohan Lal Kolhe, who teaches smart grid and renewable energy at the University of Agder in Norway, adding that hydrogen can replace fossil fuels and is a good energy carrier. "Today, most of it is produced through natural gas reforming and it can be done through electrolysis. The technical challenges in hydrogen relate to its production, storage, transportation and safety."

Unique operational approaches such as smart grid will only create more opportunities for solar cell manufacturers and energy storage producers

Mohan Lal Kolhe

Professor, Smart Grid & Renewable Energy, University of Agder, Norway

H For hydrogen

To many, hydrogen is a transition that is inevitable, albeit a long way from now. The backdrop is really about India being a cost-sensitive market. "Today, green hydrogen production costs are quite high," says Sprng Energy's Sood. "Massive investments are required in building the infrastructure for the production of competitive hydrogen and then for its storage, transportation and consumption." So, just how expensive is hydrogen? According to Garg of IEEFA, the cost today for fossil hydrogen is $2.5 per kg and for green hydrogen, $7 per kg. "Reliance aims to bring down the cost of producing green hydrogen to $1 per kg in a decade. This will revolutionise the clean energy solutions in other sectors apart from power," she says.

An ambitious target, but Reliance is also known to spring a surprise to completely transform a market it enters. The partnership with Stiesdal is with the strategic intent of both developing and manufacturing electrolysers. MEC's Jain says this arrangement can bring a lot to the table. "Stiesdal is a technology pioneer and is known for its work in the offshore wind industry. They have engineered a low-cost electrolyser and understand technology really well. It is a team of experts and a serious disruption in hydrogen is very much possible."

Maybe a lot more is required in the case of hydrogen. Sood maintains a substantial cost reduction needs to be brought in the entire value chain (electrolysers, fuel cells, among others). "Once fuelled by competitive renewable energy, green hydrogen can be a significant solution in the clean energy mix," he adds.

The combination of technology and deep pockets is ideal and it is what Reliance did with Jio very successfully. To Garg, Reliance's entry into clean energy will disrupt the market as the group can bring in new, expensive technology. "Now these technologies can be developed in India, driving the costs down. They will help build economies of scale, and its strong market position allows it to access global capital at cheaper rates," she says.

The moves on hydrogen are being made by both Adani and Ambani. Rustagi says hydrogen today is where solar was 15 years ago. "Nobody is venturing into it because of high costs and lack of an ecosystem. It is a chicken-and-egg situation," he explains. There is little doubt we are at the cusp of an interesting phase with several promising technologies. To him, the first phase (the one we are in the midst of currently) will be about solar. "It will be followed by battery storage, hydrogen and fuel cells in that order. The ensuing 4-5 years will be about solar and battery storage, while the next decade will see hydrogen and fuel cells in play," is his view.

That is some food for thought as one disruptive phase makes way for another. Without a doubt, the renewables story has never seen more turbulent times. But it could well be for all the right reasons.

Story: Krishna Gopalan

Producer: Vivek Dubey, Arnav Das Sharma

Creative Producer: Raj Verma, Nilanjan Das

Videos: Mohsin Shaikh