Please rotate your device

We don't support landscape mode yet. Please go back to portrait mode for the best experience

just say ‘steel’, and the affable T.V. Narendran’s eyes light up instantaneously. And if the conversation veers around to Tata Steel, he gets seriously involved. This, after spending more than three decades with the same company. Clearly, the enthusiasm has not dropped even a puny bit for the CEO & Managing Director of Tata Steel. Seated in the second floor of Bombay House, a heritage structure and headquarters of the diversified Tata group, Narendran, 57, is formally dressed, yet informal in approach. The large conference room is quite typical of the group—austere, understated, yet graceful. He sits behind a long table, from a different era, which blends well with a set of modern pushback chairs. At one end of the room are products from several Tata brands, among which are Tetley tea and Himalaya water.

Look at Vietnam or, for that matter, nothing is starker than China. Even when the growth rate was 10 per cent, steel consumption stood at 15 per cent only because more investment went into infrastructure-led growth.

T.V. Narendran

CEO and MD

Tata Steel

This is where many a strategic discussion takes place, often culminating in critical decisions. It could be for a big-ticket acquisition or for looking at disruptive technologies or just ways to relook at the existing cost structure. Narendran himself has a frenetic work schedule. Travel takes him to Jamshedpur (where its first and biggest steel plant is located), Mumbai and to Europe as well, as he jostles for space to think through a multi-pronged global strategy that is increasingly beginning to hinge on India. It is a life across time zones, but Narendran manages some time to indulge in reading and playing the drums. The latter stems from an interest in percussion and it was well into his corporate career when he decided to learn the instrument. Today, he does jamming sessions in Jamshedpur and smiles easily when he speaks of it.

Through all this, the honcho maintains a laser-sharp focus on the domestic market to ensure that Tata Steel makes all the right moves. It is a critical time for the company, “an opportunity of a lifetime”, he says, and the right strategy can set it up for the next couple of decades, if not more.

Why all this brouhaha over India? After all, its European operations—Tata Steel UK and Tata Steel Netherlands BV, which it bought as Corus in 2007—even today generate nearly half its consolidated revenues— Rs 1,14,486.32 crore of consolidated revenues of Rs 2,41,441.93 crore in FY22; nearly 20 per cent of its consolidated net profit of Rs 41,100.16 crore in FY22 also came from Europe. So, why this shift? For one thing, the Europe business is facing challenges related to labour unions and weak demand, among other things.

Tata Steel Plant

Jamshedpur

At the same time, at the core of the steel story in India is one word—infrastructure. The build-up of the country’s infrastructure has been nothing short of remarkable over the past few years. In this year’s Union Budget, Rs 10.7 lakh crore was allocated for capital expenditure in FY23. This follows allocations of Rs 5.54 lakh crore for FY22 and Rs 4.12 lakh crore for FY21. Narendran points out that every Budget for the past three years has had a 30-35 per cent higher allocation on infrastructure. “Construction accounts for 60 per cent of steel consumption and [then there is] automotive, which is another 15-20 per cent,” he says.

Narendran, a Tata Steel lifer who joined the company right after passing out from IIM Calcutta in 1988, expects steel consumption in India to be at least equal to the GDP growth rate, if not get past it. The thumb rule for any country is that its steel consumption should outstrip the GDP growth rate. In India, as Narendran says, it is a tad behind. “Look at Vietnam or, for that matter, nothing is starker than China. Even when the growth rate was 10 per cent, steel consumption stood at 15 per cent only because more investment went into infrastructure-led growth.” Leveraging the Indian infrastructure growth story, therefore, makes immense sense for Tata Steel.

Founded as a single steel plant in Jamshedpur, the company now has additional steel manufacturing capacities in Kalinganagar and Angul (both in Odisha), because of its own greenfield plant in Kalinganagar that was commissioned in 2015, and buyouts of Bhushan Steel, Usha Martin and Neelachal Ispat Nigam in the past four years. Almost two decades ago, the company had gone on an overseas acquisition spree, with Corus being the big one, bought at the time for $13 billion.

There’s another ‘small’ matter, of market share. The company that founded the steel industry in India way back in 1907, and led the market for much of its independent history, fell behind when its focus moved to Europe in the mid-2000s. Upstart JSW Steel and public sector Steel Authority of India Ltd (SAIL) garnered greater capacities, and forced Tata Steel down the pecking order to third position a few years ago, though it is at second spot currently. Now, Narendran makes light of the market share battle, preferring to focus on profitable growth instead, but the fact is that there is a certain ring to Tata Steel being India’s market leader that has been missing lately.

That game is now getting played out in right earnest. Whether that is happening incidentally because of the infrastructure opportunity or as a deliberate strategy is of not much consequence, but Tata Steel’s domestic capacity—after a spate of acquisitions since 2018 totalling a mammoth `51,000 crore—is now more than 20 million tonnes. That puts it ahead of SAIL and only behind JSW Steel (27 million tonnes). That gap would ordinarily be large, but it is one that Tata Steel would hope to cross in the next five years as it leverages several advantages it has garnered in recent times—capacity and, more importantly, huge tracts of land from its acquisitions that it can leverage to add even more capacity, and the fact that it is the only company that has access to precious, captive iron ore.

Founded as a single steel plant in Jamshedpur, the company now has additional steel manufacturing capacities in Kalinganagar and Angul (both in Odisha), because of its own greenfield plant in Kalinganagar that was commissioned in 2015, and buyouts of Bhushan Steel, Usha Martin and Neelachal Ispat Nigam in the past four years. Almost two decades ago, the company had gone on an overseas acquisition spree, with Corus being the big one, bought at the time for $13 billion.

Now, it’s all about India. “Nowhere else in the world do you see 5-6 million tonnes being added each year,” says Narendran. “Even when I look back at 2015 or 2016, which was the lowest point in steel prices, India still had a 20 per cent Ebitda margin. That was in a down cycle and it is a clear indication of our structural strength but we did not have scale.”

The domestic focus finds favour with those who track the company. To Bhavesh Chauhan, Research Analyst at IDBI Capital, the important part is not just the acquisitions but the turnaround of Bhushan Steel and Usha Martin. “It also means lesser dependence on uncompetitive European operations. Going forward, Europe’s contribution will continue to drop,” says Chauhan.

In the last two years though, they [Tata Steel] have deleveraged meaningfully as the steel cycle is on an upswing. Going forward, they will continue to invest in growth capex and yet bring down leverage since steel prices are still robust despite a 30 per cent fall from the peak.

Bhavesh Chauhan

Research Analyst

IDBI Capital

The other positive is that Tata Steel’s new direction coincides with large steel exporters of the likes of China, Japan and Korea being forced to take a relook at their exports, driven primarily by issues related to carbon footprint. “The other two players are Russia and Ukraine,” says Narendran. “So, if you take a look at the top five exporters of steel, they have their own compulsions to take a different view on the export market, leading to a more balanced world trade.”

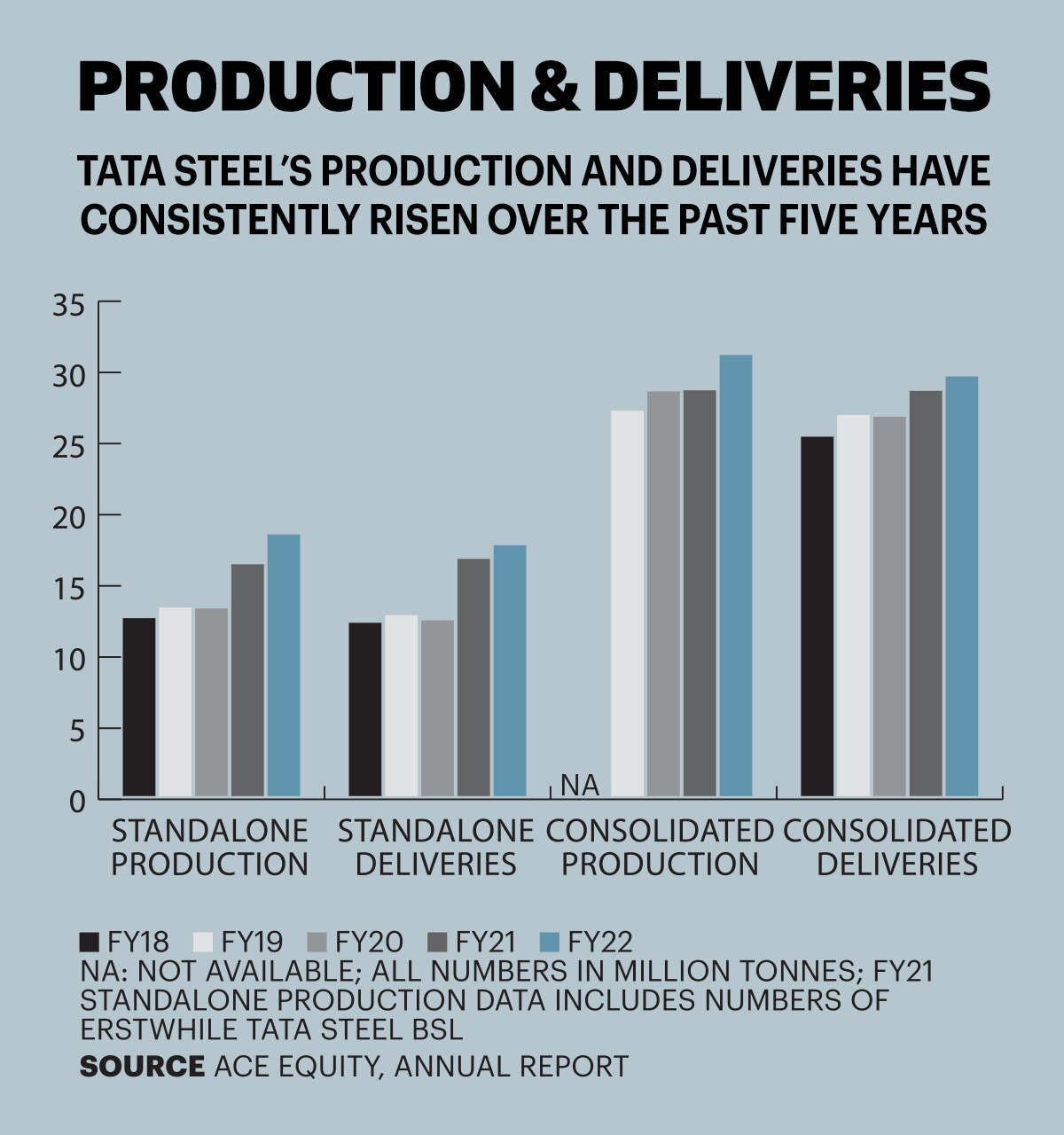

From a domestic point of view, Chauhan points out that over the past five to seven years, it has been a story of consolidation of market share among the top four players (see graphic Steel-ing a March). “Looking ahead, they are all expanding. Over a period of five to 10 years, we will only see a further increase in market shares,” says Chauhan. According to him, leverage was high for Tata Steel in 2019-20 (see graphic Financial Metrics). “In the last two years though, they have deleveraged meaningfully as the steel cycle is on an upswing. Going forward, they will continue to invest in growth capex and yet bring down leverage since steel prices are still robust despite a 30 per cent fall from the peak,” he says.

At a 1:1 debt equity ratio, they [Tata Steel] can spend between Rs 40,000 crore and Rs 50,000 crore on capex every year. This means that they can add 4-5 million tonnes of capacity every year.

Rakesh Arora

Founder

Go India Stocks

Tata steel’s India buyout story had an unhappy beginning, although it spurred the company to do better. Losing the bid for Electrosteel Steels in 2018—it was finally picked up by Vedanta—was the tipping point. Narendran says: “We did not put in our best bid.” The approach to a potential acquisition of Bhushan Steel (again in 2018), therefore, needed to be different. “It was to bid at a number, which we should not regret losing,” he explains. Eventually, Tata Steel paid `35,200 crore and clinched it. “We did not want to put `32,000 crore and lose it to someone for Rs 33,000 crore, when we knew we could make it work at Rs 35,000 crore. These opportunities are few and far between, plus it was a clean asset,” he says categorically. The beleaguered Essar Steel in western India—finally acquired by ArcelorMittal Nippon Steel—was also on the block but Tata Steel let it pass. “Assets in the east allowed us to leverage our iron ore. Essar is a good asset but the port issue surrounding it is quite complicated.”

In the pecking order for Tata Steel, Bhushan Steel was right on top followed by Electrosteel, and then Bhushan Power and Steel, which was picked up by Sajjan Jindal’s JSW Steel. Tata Steel then bought over Usha Martin’s steel business in 2019 and Neelachal Ispat Nigam earlier this year.

The strategic rationale for each acquisition comes out quite clearly. Bhushan Steel brought forth flat products (largely used in building and construction), a segment where Tata Steel needed a larger presence. “Bhushan Steel was producing only 3 million tonnes before the acquisition and for infrastructure-led growth, this is a vital piece. Besides, with export duty, long puts us in a better position since it is more about local trade,” points out Narendran. Interestingly, the erstwhile owners of Bhushan Steel visited Tata Steel’s Jamshedpur plant in the past and replicated most of it at their Angul plant housed in Odisha. In that sense, Bhushan Steel was an asset known to the Tatas. “The advantage of inorganic growth is that you get cash flows immediately. Today, Bhushan Steel produces more than we do in Kalinganagar, where it has taken us 10 years to get to where we are,” he explains.

The story of contrasts is interesting to say the least—at the time of the buyout, Bhushan was producing 3 million tonnes per annum and with minimal capex, that number is at 5 million today apart from being cash positive. Kalinganagar was started in 2005 and had issues for five years before revenue started only in 2018. “When you build a greenfield project, the ecosystem too needs to be created. You take care of the land, schools and hospitals. Though inorganic involves paying a little more, the business case is often stronger and one hits the ground running,” says Narendran.

Koushik Chatterjee, the company’s Executive Director & CFO, thinks Tata Steel, over the past decade, has had a “pretty sharp strategy and been clinical in execution”. Citing the case of Bhushan, he makes it clear why it made sense. “It was that one asset with a clear potential to align well with our line of business. Be it strategy, proximity or the ability to be leveraged in the future, it was a good fit,” he says. Again, he picks up the case of Usha Martin (Jamshedpur), where the attraction was long products. “It was a specialised product and that makes it interesting.” At `4,094 crore, it was a good buy.