We don't support landscape mode yet. Please go back to portrait mode for the best experience

Most market experts are bullish on Indian equities right now, but some caution never hurt anyone. Now is a good time to take note of some of the headwinds that could make the ride bumpy for investors

“The four most dangerous words in investing are: it’s different this time.”

This oft-repeated quote in reference to the stock market was uttered by legendary investor and money manager Sir John Templeton. The mutual fund pioneer would certainly know. His Templeton Growth Fund launched in 1954 delivered 15 per cent returns annually for 38 consecutive years. The quote may well have been uttered ages ago, but it has stood the test of time. There is no market cycle—especially periods of upswings—when a large section of market experts has not uttered the same four dangerous words: it’s different this time.

Interestingly, it’s no different this time, too!

Both the Indian benchmark indices—the BSE Sensex and the broader Nifty 50 of the National Stock Exchange—touched their respective highs in July, and market experts were quick to point out how the rally in the Indian stock market was different this time around, especially when many other foreign markets were struggling amid global and their own set of domestic headwinds.

The Street’s growth expectations for Nifty 50 remain elevated; a busy political calendar, erratic rains, rising crude, and a potential stimulus in China impacting FPI flows to India are challenges

Amish Shah

Head, India Research

BofA Securities India

For India, the strong domestic growth and consumption story, along with the government’s focus on infrastructure and initiatives like ‘Make in India’ and the production-linked incentive (PLI) scheme, were said to be driving the markets. Further, strong liquidity support from both foreign and domestic institutional investors is also being held up as a huge catalyst. The period between March and July has seen foreign portfolio investors (FPIs) ploughing in more than $19 billion in Indian equities, with the months of May, June and July registering inflows of over $5 billion each. Domestic institutional investors (DIIs)—mutual funds, banks, insurance companies, domestic financial institutions and the National Pension System (NPS)—are also not far behind, with net flows of $11.20 billion in the current calendar year till August 16.

But, is it really different this time? If yes, then there shouldn’t have been any correction, because only the absence of an ensuing fall after record highs would make this market cycle any different. The benchmark Sensex has fallen more than 2,200 points, or nearly 3.3 per cent till August 14, from its all-time high of 67,619.17, touched only on July 20.

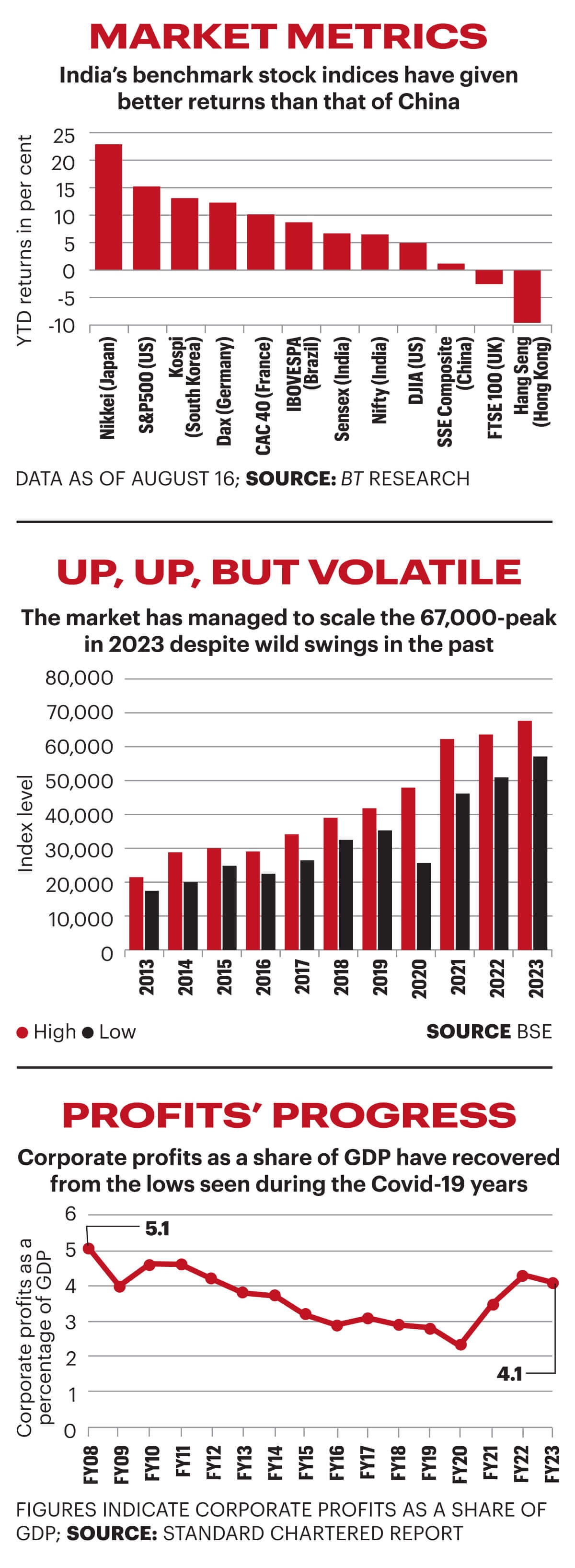

Incidentally, the Indian benchmark—that was amongst the best performing ones in the current calendar year (CY23) when it touched its new high in July—currently lags in returns when compared with global and Asian peers including the S&P 500 of the US, Japan’s Nikkei, South Korea’s Kospi and Brazil’s Bovespa. (See chart Market Metrics.) History is replete with instances when markets have moved in cycles, and each cycle has comprised of an upswing and a downswing; only the periods of the swings differ, but the composition stays the same. And, hence, some of the most successful stock market investors—including the legendary Warren Buffet—have repeatedly said that it is just not possible to time the market to get the maximum returns.

There is little doubt that equities have proved to be the best asset class in terms of returns over the long term, but one should never forget another important adage, perhaps more relevant than what Templeton said: “Stock market investments are subject to market risks.”

[The risks are] global equity correction/derating as bond yields rise; higher oil prices which hurt India’s twin deficits; and the risk that mass market consumption does not revive as expected

Sanjay Mookim

India Strategist and Head of Research

J.P. Morgan

Business Today reached out to some of the most prominent market experts—domestic and foreign brokerages, mutual funds, portfolio managers and well-known individual investors—to gauge their views on what they feel the market could have in store in the coming months. More specifically, the aim was to understand the key risks that investors should bear in mind while investing, even as an increasing number of individuals, especially retail ones, take the plunge into the capital markets and put their hard-earned money in stocks.

There is no dearth of risks, both on the global and domestic front, is the firm conclusion of the experts. But in this instance, the proof of the pudding lies not in gorging on the current good run in the markets blindly, but in understanding the risks thoroughly and navigating them smartly, they say.

Inflation, elevated expectations of earnings growth, rising crude prices, the hawkish stance of central banks globally (especially the US Federal Reserve), any slowdown in FPI and DII flows, the possibility of recession, or recession-like scenarios in some developed markets, the impact of a potentially deficient monsoon, and political surprises at the upcoming state and general elections are all top contenders to be the biggest risks facing the markets. “A busy political calendar in the coming months remains a risk. We could see volatility in the markets as some of the key states go for state elections,” says Amish Shah, Head of India Research of BofA Securities India. “Further, one could expect near-term headwinds from erratic rains weighing on inflation, rising crude prices impacting margins in select sectors, and a potential economic stimulus in China impacting FPI flows to India,” he adds, though he believes that the risks are transitory and likely to normalise over a year’s time.

Indeed, as India’s inflation has been on a steady climb recently, with July seeing the consumer price index (CPI) jump to a 15-month high of 7.44 per cent, from 4.87 per cent in the previous month. (See graph Uphill Run.) On the other hand, crude oil prices—though much lower than the highs they touched around the middle of 2022 (they had stayed above the $110 a barrel-mark in most weeks between February and July 2022)—are still hovering around $85 a barrel. It was mostly below $80 between April and July this year. (See graph Calm before the storm?)

Sanjay Mookim, India Strategist and Head of Research at financial services giant J.P. Morgan, believes that higher oil prices—that hurt India’s fiscal and current account deficits—is one of the key risks. “India’s macro conditions have improved as the current account deficit has fallen sharply. Inflation has also fallen with lower commodity prices. Both of these can reverse if oil were to move higher,” he says. This assumes significance as higher oil prices fuel inflation, which in turn leads to central banks raising interest rates to control inflation, a move that is not particularly liked by the stock markets.

The US Fed, unarguably the most powerful central bank globally, has already said that there are enough data points to build a case for further rate hikes. “Most participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy,” states the minutes of the US Fed’s July 25-26 policy meeting. Deepak Jasani, Head of Retail Research at HDFC Securities, believes that the Fed’s hawkish stance is another key risk facing the Indian stock markets. “High inflation and a more hawkish commentary or action from the US Fed than what the market is expecting, geopolitical events, or global debt related repercussions, could impact the global risk appetite going forward.”

In a similar context, Mahesh Patil, Chief Investment Officer of Aditya Birla Sun Life AMC, says that future policy actions by the US Fed and the overall volatility in the global macro environment may be a dampener in the near term. He adds that the current boil in crude prices—up around 15 per cent in the past five months between March and August—can affect the Indian markets as they are actively tracked by domestic as well as foreign investors.

So, crude prices, again!

Future policy actions by the Fed and overall global volatility; spike in food and vegetable prices leading to higher-than-expected inflation; and a rise in expectations of a China stimulus [are risks]

Mahesh Patil

CIO

Aditya Birla Sun Life AMC

It’s not only about oil prices. All the risks are closely interlinked, even those related to earnings growth outlook and, as Patil points out, the liquidity flows coming from FPIs and DIIs. Rakesh Arora, Managing Partner of Go India Advisors and former head of India research at global financial firm Macquarie Group, says a deep recession in the US and Europe could force FPIs to pull money out of the domestic market on risk-off trade and inflation coming back. Further, a spike in oil prices could also lead to more interest rate hikes and squeeze corporate margins.

Interestingly, Arora, and a clutch of other leading market experts, believe that a surprise political outcome in the upcoming state and general elections could make the markets more jittery than usual. “Key state elections are coming up early next year. If the BJP’s position is seen as shaky, the markets can start thinking of an unstable government being formed in the 2024 general election,” says Arora. Elections in Madhya Pradesh, Chhattisgarh, Rajasthan, Mizoram and Telangana are scheduled for the coming months, with the general elections likely to be conducted around April-May 2024.

Jiten Doshi, Co-founder and Chief Investment Officer of Enam Asset Management Company, agrees that one of the key risks facing the stock markets is political in nature, in the form of an “unexpected electoral outcome in India and its medium-term effects on policy”.

Meanwhile, the run-up to the general elections, combined with a busy state election schedule, typically gives rise to periods of intense volatility, though it is also known to dissipate rapidly. Gaurav Dua, Head of Capital Market Strategy at Sharekhan by BNP Paribas, also has a bullish view on the markets, but lists possible recession in developed markets, rising crude oil prices, and the forthcoming state elections as three key risks for the markets. “If the outcome [of the elections] is far worse than market expectations, it could have a meaningful impact on markets. However, it is generally seen that the known risks do get absorbed quickly. It is always the unknown risks that can lead to a sharp correction.”

Interestingly, there is a silver lining associated with the electoral risk in terms of the government’s enhanced focus on infrastructure spending to brush up its credentials before the elections. “Calendar year 2023 is a pre-election year. It has been observed that benchmark indices perform relatively well in the pre-election years… Support could continue from the government, which is keen to stimulate investment activity in newer sectors,” says Jasani of HDFC Securities. He adds that initiatives like the PLI scheme can help boost manufacturing by wresting some supply chains away from China, propel exports, and attract rapidly-growing industries like semiconductors, electric vehicles and renewables that are of strategic geopolitical importance.

Similarly, Arora says that the government has already stepped up infrastructure spending, and execution on the ground is expected to gather steam going ahead.

[The risks are] adverse developments in the international arena; a muddled economic performance from India; unexpected electoral outcome in India and its mediumterm effects on policy

Jiten Doshi

Co-Founder & Chief Investment Officer

Enam AMC

When the benchmark BSE Sensex touched its all-time high of 67,619.17 on July 20, it had rallied a little over 11 per cent, compared to its 2022 close. More importantly, it had surged nearly 18.5 per cent from its low of 57,084.91 touched earlier this year. At its peak, it was among the best performing equity benchmark indices globally, though the ensuing correction has brought it to the middle of the pack.

As mentioned earlier, the rally was on the back of strong support in the form of factors like ample liquidity from FPIs and DIIs, resilience of the Indian economy, a better-than-expected economic recovery post-Covid-19, the strong balance sheets of corporates, and initiatives such as the PLI and ‘Make in India’ that are boosting manufacturing.

Experts say that while there are quite a few headwinds, there are a number of positives as well that can keep the market momentum going. The strong liquidity support is a big plus right now, with both FPIs and DIIs pumping in huge amounts of money to enhance their equity exposure in India. Incidentally, experts do not expect any quick reversal in these flows in the near future. “Given that India remains an oasis in a world of uncertainty around growth, inflation, interest rates, as well as geopolitical tensions, it would be reasonable not to expect any sharp outflows from the Indian markets in the absence of any negative developments,” says Tejas Gutka, Fund Manager at Tata Mutual Fund, while adding the caveat that India’s relative valuation premium could also act as a cap to high inflows.

Even prominent investor Vijay Kedia, MD of Kedia Securities, is “extremely bullish” on Indian equities. He lists strong FPI participation, private sector capex, and softening of inflation and interest rates as the key positives for the markets. “Over the next one year, the first six months should be bullish while the next six would be uncertain due to elections. After the elections, sentiment should improve as there is an in-built momentum in the economy, and therefore the next two to four years look very promising,” he says, while forecasting the Sensex to hit the 70,000-mark by the end of 2023.

Similarly, Anish Tawakley, Deputy CIO for Equity and Head of Research at ICICI Prudential Mutual Fund, says that over the next one year, the economy is well positioned for a cyclical recovery to be led by home-building. Though on a valuation basis, he believes, the Indian markets are not cheap and there is a froth building up in mid- and small-caps. Positive for the medium- to long-term, he expects capital spending to increase in the home-building sector, and consequently corporate capex to pick up as well. “We expect home-building activity to pick up and create a virtuous cycle. Home-building creates employment and it consequently creates demand for manufactured goods. As demand picks up, corporate capex will also pick up,” he adds.

A cyclical recovery is indeed imminent if one looks at metrics such as profitability as a share of the gross domestic product (GDP). For instance, the cumulative profit of NSE 500 companies as a share of the GDP has recovered and is close to the pre-pandemic levels. It has risen from 3.5 per cent in FY21 to 4.1 per cent in FY23, states a recent report from Standard Chartered. (See chart Profits’ Progress.) “Long-standing policy reforms, political stability, significant infrastructure investments and technological advancements are likely to aid improvements in per-capita income, boost discretionary consumption demand and enhance corporate profitability,” the report adds.

Discretionary spending is also a big positive on the list of most experts, due to which they are bullish on sectors that stand to benefit from such spending. Citing capital expenditure in sectors such as industrial, capital goods, infrastructure and cement, Sneha Poddar, AVP of Research, Broking and Distribution at Motilal Oswal Financial Services, says financials, automobiles and consumption will also show growth.

Foreign stock markets turning bearish; sentiments in local market turning euphoric [are risks]. Over the next year, the first half should be bullish while the next would be uncertain due to elections

Vijay Kedia

Managing Director

Kedia Securities

“In the case of auto, all the categories are expected to see growth as the festive season approaches, and rural demand is expected to see an improvement on the back of normal rains, better crop realisation, and easing inflation worries,” she says, adding that the capex theme will continue its dream run with the government’s strong thrust on infrastructure development, and the green shoots visible in private capex.

In terms of sectors, most experts are confident about real estate, building materials, capital goods, banking and financials, industrials, consumer durables, speciality chemicals, fast moving consumer goods (FMCG) and pharmaceuticals, at the current juncture. They cite the strength of the Indian economy as the reason.

“India’s macros are in good shape,” says V.K. Vijayakumar, Chief Investment Strategist of Geojit Financial Services. “The economy is in a sweet spot. The banking sector is in the pink of health, the corporate sector is deleveraged, private capex has started, and CAD (current account deficit)] and FD (fiscal deficit) are under control. India has been the fastest growing large economy in the world in 2021 and 2022, and it will continue to be the fastest growing large economy for many years to come.”

Separately, sectors that most experts advise one to be careful about include IT and IT services, metals, utilities and commodities. To be sure, most of them say that the bearish outlook on these sectors is transitory in nature due to a combination of global and domestic headwinds, and a reversal of certain macroeconomic indicators will again make some of them the flavour of the season.

For instance, in the case of metals, Sujan Hajra, Chief Economist and Executive Director of Anand Rathi Shares and Stock Brokers, says that while the prices of several commodities, including crude oil and food grains have recently risen, most metal prices have remained weak due to concerns about demand. “Metals are a cyclical sector globally, and demand from China has a significant impact on the sector’s performance… At the moment, however, the Chinese growth outlook doesn’t appear promising… We anticipate that the sector will underperform over the next 12 months.”

Incidentally, irrespective of the market cycle, there will always be certain sectors that most experts would be bullish about, while advising investors to stay away from certain others. So, what does that mean for investors, especially now when the markets have already corrected to a large extent after touching record highs?

[The risks are] possible recession in developed markets; rising crude prices; forthcoming state elections. If the outcome is worse than market expectations, it could have a meaningful impact

Gaurav Dua

Head, Capital Market Strategy

Sharekhan by BNP Paribas

“We expect the current equity cycle to be analogous to the 2003-2008 bull cycle, when output growth rose sharply, inflation stayed stable and improvements in productivity drove a rise in investments,” states the Standard Chartered report. During that period, higher investments did not lead to a widening of the current account deficit as the rise in savings was led by an improvement in public savings (fiscal consolidation), and private corporate savings, the report adds.

In a similar context, Neeraj Chadawar, Head of Quantitative Equity Research at Axis Securities, says the Indian economy will continue to remain in the sweet spot of growth, which would in turn be the biggest driver of Indian equities going forward. “The improvement in the balance sheets of India Inc. is another positive attribute, and a significant one at that, as it will ensure that Indian equities are on track to deliver double-digit returns in the next two to three years, led by double-digit earnings growth,” he says.

Chadawar is not alone in being bullish. Amar Ambani, Group President and Head of Institutional Equities of YES Securities (India), is also “extremely bullish” on Indian equities, and believes that the long-term ‘margin of safety’ for Indian equities looks high. “Our self-sustaining consumption story, the government’s ongoing infra focus, and the expected pick-up in private capex from the PLI schemes, and the China+1 paradigm playing out are among the key long-term positives,” he says, adding that when FPI inflows come in strongly (like they did back in 2006) to complement the ongoing domestic liquidity flow into financial assets, Indian equities will definitely see euphoric growth.

The stock market seems to be an interesting place to be in right now. Whether one is a seasoned investor, or just a newbie making his or her first few bets, growth and returns ultimately boil down to how one perceives the risks, and whether they have done thorough due diligence before investing. At the end, one is reminded of what billionaire investor George Soros said: “It’s not whether you’re right or wrong that’s important, but how much money you make when you’re right, and how much you lose when you’re wrong.”

UI Developer : Pankaj Negi

Creative Producer : Raj Verma

Videos : Mohsin Shaikh