In 2025, Ericsson came out with a set of interesting numbers—Indians are the biggest consumers of data, with an average of 36 GB per user per month. Whether it is enterprises storing data on the cloud, consumers streaming live sports or watching the latest web series—all this is generating copious amounts of data.

This, in turn, is driving demand for data centres at an unprecedented pace. Existing players are ramping up expansion plans and newer, nimbler companies are entering the segment in a bid to tap the growing demand for AI data centres.

In February, Yotta Data Services, a provider of hyperscale data centres, sovereign cloud, and AI compute infrastructure, announced an investment of $2 billion to deploy Nvidia Blackwell GPUs or Graphics Processing Units to form one of Asia’s largest AI superclusters. Last year, information and communications technology company Sify Technologies announced an investment of $5 billion to modernise and expand its data centre operations. This is only the beginning.

Purushothaman KG, Partner and Head of AI and Technology Transformation, KPMG in India, believes this is a significant transition. “The India data centre story is, at its core, a story of the country’s pivot towards a digital economy. This shift is being driven not only by India’s role as a global exporter of technology services, but also by the rapid expansion of a domestic consumer base that is increasingly consuming digital and technology-led services,” he says.

India’s data centre capacity is currently pegged around 1.4 GW and projected to double by 2027, going by the capacity under construction, and can grow five-fold by 2030 if the projects are fast-tracked, according to a report by Macquarie Equity Research. But this barely makes a dent in how India stacks up against the rest of the world. Consider this: the global data centre capacity is about 122 GW, which puts India at just over 1% of the global capacity. Given the volume of data being generated and processed in India, the current capacity is simply not enough, especially as the boom in AI applications across sectors is expected to generate more demand. This is fundamentally changing how data centres will be required to be built, run and operated.

Rajiv Ranjan, associate research director, International Data Corporation (IDC), says Tier II cities are poised to be at the forefront of this transformation. “We expect more AI workloads to get deployed in the next three-four years, driving the demand for edge data centres in Tier II cities and in locations that are closer to customers or where data is generated. Higher demand and deployment of AI-optimised servers in colocation data centres will drive the power consumption very fast. Enterprises will have to build higher power capacity data centres with higher rack power density,” he says.

This is how it works: AI workloads typically require a high-density GPU environment, which needs more power and advanced cooling techniques as compared to traditional workloads. According to the 2026 Global Data Outlook report by JLL, AI workloads, both inferencing and training, are projected to grow to 50% of the overall data centre workload by 2030, from 23% in 2025, even as overall workloads grow from 103 GW to 200 GW.

The Indian market is dominated by colocation data centre providers like Yotta, Sify Technologies, NTT, Equinix and others, where the operator provides a shared infrastructure space with the companies bearing the responsibility of sourcing their own computing equipment. “AI service providers are looking at India as a big market, and they are shifting a lot of workloads into this country,” says Manoj Paul, MD, Equinix India, adding the company is focused on tapping the growing demand for AI inferencing.

NEW USE CASES DRIVING DEMAND

In addition to the growth in AI-driven applications, there’s also a change in how customers are using data centres. More enterprises are storing data on the cloud and there’s a huge increase in industrial IoT applications which are processed and stored in these data centres. A mix of cloud computing, hyperscale deployments and increase in high-performance computing workloads are adding to the demand. “Data centres are increasingly supporting latency sensitive applications such as real time analytics, digital services, and industry specific AI use cases across banking, manufacturing, healthcare, and media. Together, these use cases are shifting data centres from static infrastructure environments to highly dynamic, performance-driven platforms that are central to customers’ digital and AI strategies,” says Alok Bajpai, Managing Director, India, NTT Global Data Centers.

Enterprises are also placing new demands on their co-location partners to cater to their changing business dynamics, like flexibility in how much space they require and seamless interconnectivity among different service providers. All these factors are translating into a change in infrastructure requirements with the need for larger facilities with higher power and cooling requirements.

Sify Technologies, which already runs 14 data centres in India, is planning another 11 facilities across the country. “These upcoming centres are being built to support AI-ready infrastructure and edge deployments, ensuring we stay aligned with the next phase of digital growth,” says Roopesh Kumar, Head—Data Center Projects at Sify Technologies. While existing data centres can be retrofitted, industry experts say that’s not necessary since we are at an early stage. However, all new projects are being designed while being cognisant of these changing requirements. “The shift towards AI-driven workloads is directly shaping our future plans—from how we select sites and secure power, to how we phase development and invest in long-term capacity,” says Bajpai. The company is re-engineering existing platforms to support AI-ready infrastructure, which means designing campuses with higher power density and advanced cooling technologies.

COMBATING MANY CHALLENGES

The first change is the massive power requirements because of the compute capacity required. “The GPU infrastructure that we deploy for AI has a much higher rack density and draws a lot more power than traditional workloads,” says Sharad Sanghi, Co-founder and CEO, Neysa, an AI-acceleration cloud provider. He has been closely involved with the evolution of this industry in India and points out that initially, data centres would have a capacity of about 40 kW per rack depending on the number and the kind of servers. Now, this is going up to over 150 kW, so there is a significant shift in the energy density of the rack, which means conventional cooling techniques cannot be deployed. Neysa provides GPU compute, storage and network services, along with software and third-party integrations to enterprise customers, and currently uses NTT as a third-party data centre. Demand from neocloud providers is adding to the increased capacity requirements of the traditional operators. Neocloud companies are specialised, high-performance cloud providers focusing on GPU-as-a-Service to power AI training and inference.

Hence, the basic build of a data centre needs to change, with higher floor clearance for the changing rack space. With power consumption going up significantly, the cooling methods are evolving as well.

Air cooling is effective only up to a certain power load; newer AI data centres will have to be liquid-cooled to remain efficient. This shift is opening an opportunity for newer players to make inroads into the segment.

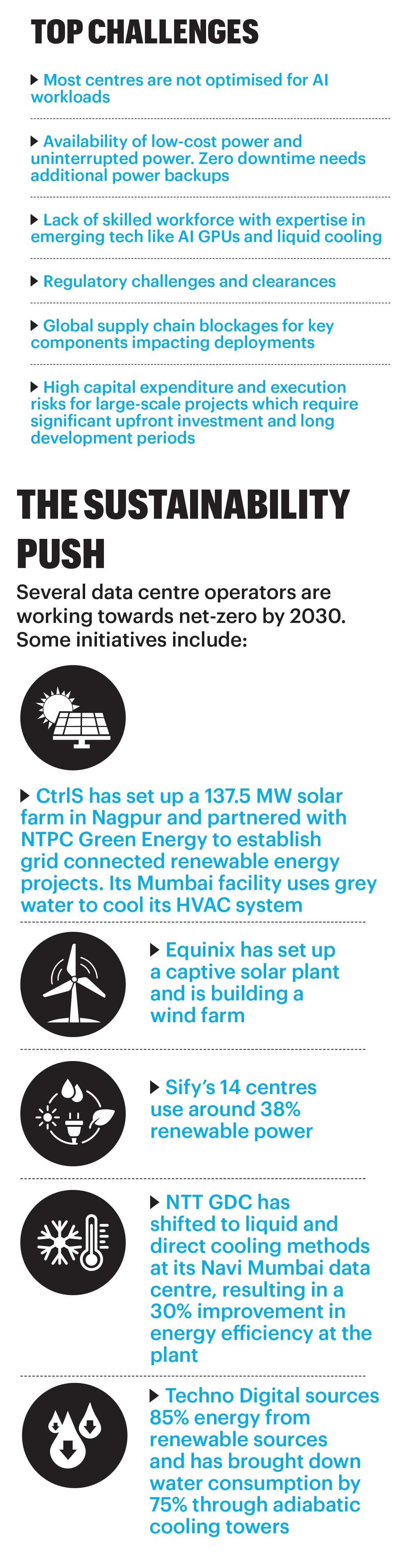

Techno Digital, which recently launched its first facility in Chennai, is a spin-off from Techo Electric & Engineering Company, which has been working with data centre providers in India on their power requirements. “If you’re going to talk about 1000s of megawatts getting consumed in a single location, it becomes a business of power and that’s the problem that we are trying to solve,” says Ankit Saraiya, Director and CEO, Techno Digital. The focus is also on sourcing power from sustainable sources. Techno Digital’s next facility coming up in Noida will have the first 100% carbon neutral hyperscale design, powered through renewable energy sourcing.

NEWER HUBS

Another major transitional point is the focus on Tier II cities. At present, a majority of data centres in India are in Mumbai and Chennai because of access to subsea cables for latency, or minimal lag, as well as proximity to the financial centres (Mumbai), which are the biggest users of these facilities. Mumbai alone hosts over 50% of the country’s data centre capacity, but this is slowly changing. Companies are setting up smaller or edge data centres to be closer to consumers.

Many of these are expected to come up in places like Jaipur, Bhubaneshwar, Vizag and Patna, either to be close to the coast, a large industrial cluster (for edge processing) or a large consumer base.

RackBank, another new entrant in the data centre business, is setting up its first facility in Raipur, largely on account of reliable and low-cost power supply, as well as access to relatively cheap land and local talent. Being in central India means that whichever direction the data is moving, the latency is unilateral, says Founder & CEO, Narendra Sen. The company is rethinking how a data centre is constructed by creating a horizontal structure using pre-engineered buildings. “We’ve reduced the building time to six-seven months. Rather than a traditional real estate mindset where you think of going vertical, we are thinking from the technology side, so we’re building horizontal sites, as they are denser,” he says.

RackBank is not the only one which sees the potential in moving away from the metros. Techno Digital has tied up with PSU RailTel to set up 102 facilities across the country by 2030 under a 20-year revenue sharing partnership, in a move that Director and CEO Saraiya says will truly democratise access to high quality digital infrastructure. These would range from 0.5 MW to 1 MW in most cases, with the option to scale up as needed.

The established players are a bit more cautious about this shift, while being open to the possibility of eventually moving out of the metros. “Edge data centres are primarily populated by content delivery platforms. These networks don’t process data, just relay it, so the storage and processing requirements are considerably lower,” says Rahul Dhar, President—Global Data Center Operations & Enterprise Delivery of CtrlS.

NTT, too, is considering expansion to smaller cities in the future. “Smaller and emerging cities can make sense where there is strong power availability, improving connectivity, and support from state governments, particularly for AI, cloud, and enterprise workloads. Any expansion into these markets will be driven by long-term demand and infrastructure readiness,” says Bajpai.

Industry watchers expect this shift to become more widespread over the next two years, as the demand for AI inferencing, coupled with industrial and consumer demand, kicks in.

POLICY BOOST

The recent budgetary announcement proposing tax incentives for companies hosting their data in India has brought much cheer to the industry. The move aims to position India as a global AI and cloud hub—similar to what Singapore and Malaysia have done—by offering a tax holiday till 2047 to foreign cloud providers using domestic data centres. “The tax exemption sends a clear signal to investors by reinforcing India’s structural cost and efficiency advantages in data centre operations. It is expected to encourage existing facilities to scale international services, while prompting new and marginal players to adopt hybrid operating models that balance offshore capacity with increased deployment within India to optimise returns,” says KPMG’s Purushothaman.

Despite the challenges, India is among the lowest cost countries when it comes to building and running a data centre. Neysa’s Sanghi points out that this also allows these companies to tap into India’s skilled talent pool. “These incentives make it possible for companies to make India their regional hub,” he says.

A CHALLENGE LOOMS: SUSTAINABILITY

A data centre boom comes with its own set of hurdles, environment being a primary one. In several countries like the US, there is a backlash against data centres because of their resource-hungry nature. Cities are protesting heavy power and water consumption—often rivalling the amount consumed by the rest of the town. This is where the focus on green data centres and sustainable practices will pay off, say industry watchers.

Companies are putting in place a slew of initiatives to offset their carbon footprint. “Most customers are conscious about their carbon footprint and would like to partner with someone who can help them meet their net zero targets,” says Paul of Equinix. Even for enterprises where this may not be a priority at present, data centre operators know that having a strong sustainability footprint can give them an edge. Most companies are putting in place a series of measures to offset their carbon footprint, like using renewable power and shifting to more efficient cooling methods. CtrlS has set up a solar farm in Nagpur and uses grey water to cool its facilities in Mumbai. Equinix too has set up a captive solar plant and is in the process of building a wind farm.

This is still an industry in transition, and a lot of the technology being introduced, like liquid cooling and high-density cooling, is comparatively new to India, where cooling requirements are a bit different from places in North America and Europe.

“We are a hot and humid country and are trying to learn from our peers and understand what works,” says Dhar of CtrlS. Talent is another issue. There aren’t enough skilled workers who know how to work with these new cooling systems or high-power GPUs, and companies are collaborating with training institutes to design the curriculum so that it is in sync with what the industry requires. “We don’t have the talent proportionate to what we are going to need in the future, so we have to change the way we are developing our manpower,” says Dhar.

Meanwhile, the global AI boom has also resulted in supply chain challenges worldwide. “Hardware availability and affordability continue to be a challenge for the industry, particularly for advanced AI infrastructure. High performance GPUs and specialised equipment remain constrained globally, and pricing reflects strong demand from hyperscalers and AI-driven workloads,” says NTT’s Bajpai.

Then there are the regulatory challenges, with every step—from land acquisition, environmental clearance, power connectivity and construction—requiring clearances. The industry is hoping for a single-window clearance system which, when coupled with the tax incentives, can have a truly transformational impact on the industry.

Ashish Nadkarni Group Vice President and General Manager, Global Domain Lead, Enterprise Infrastructure, IDC, cautions that ultimately data centre operators need to think long and hard before deciding how to route their investments. “It’s one thing to build a data centre that is optimised for AI workloads and another thing to build a data centre that is meant for general purpose use, and AI just happens to be one of the workloads,” he says. The latter can be more attractive for companies depending on their requirements, at least in the near term, and that is a decision data centre operators must take.

What’s clear is that the demand for data centres will only accelerate—and the real opportunity lies beyond the metros. As digital adoption deepens across India, Tier II towns are emerging as critical growth hubs. Companies that build robust infrastructure early in these rising markets will be best positioned to capitalise on the next wave of the data centre boom.