The name was bonds. Infrastructure bonds. And there was a time when investors rushed to buy them as if there was no better place to park their money. The public issues of infrastructure tax saving bonds by financial institutions such as IFCI, IDBI and ICICI Bank and the Rural Electrification Corporation (REC) were, till just a few years back, the most awaited Section 88 event in the tax planning calendar.

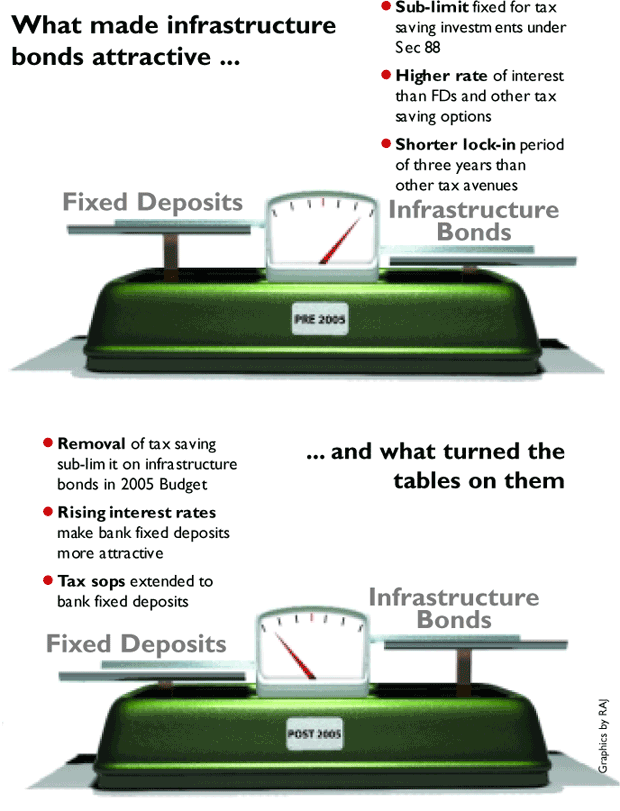

Indeed, infrastructure bonds offered everything that a taxpayer could ask for. A rate of interest that was higher than the prevailing rate offered on bank fixed deposits. A safe avenue for investment. Tax rebate on the amount invested. And a shorter lock-in period than other tax saving options. In short, these bonds were licensed to thrill.

What made infrastructure bonds such a compelling investment option was the sub-limit set under Section 88 of the Income Tax Act. To fully utilise the tax rebate extended to him on an annual savings of Rs 80,000, a taxpayer had to allocate at least Rs 20,000 to infrastructure bonds.

Also, he could invest the entire Rs 80,000 in these bonds and get tax rebate. Besides, the lock-in period of these bonds was only three years compared with six years for NSCs. The sub-limit for these bonds was later raised to Rs 30,000 when the overall limit oftax savings was raised to Rs 1 lakh a year.

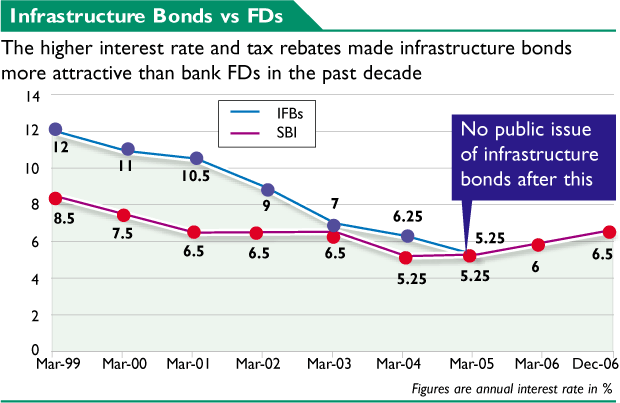

Infrastructure bonds were a good option even if a person was not investing to save tax. In 2000, for instance, the State Bank of India was offering 7.5% interest per annum on three-year fixed deposits while infrastructure bonds gave 11%. If you factored in the tax rebate, the effective annual yield of IDBI’s infrastructure bonds issued in February 2000 came close to 19%.

The infrastructure bandwagon rolled on even after interest rates started their downward journey after 1999. By 2003, the coupon rate of infrastructure bonds had slipped below that of NSCs. But taxpayers continued to pour in money, thanks to the sub-limit set under Section 88. Clearly, with the stock markets in the doldrums (the Sensex stood at 2800 in March 2003), investors were looking for safe and secure options to park their money in.

The Budget of 2005 spoiled the party for infrastructure bonds. It threw out Section 88 and all its paraphernalia of sub-limits, replacing it with an umbrella Section 80 C that allowed taxpayers to allocate Rs 1 lakh to any of the specified investment options. “The change in the rules for tax savings in the 2005 Budget sounded the death knell for infrastructure bonds. People could invest on the basis of their needs and risk appetite,” says Delhibased financial planner Surya Bhatia of Asset Managers.

If you were an aggressive investor, you could opt for equitylinked saving schemes of mutual funds. These schemes have turned out phenomenal returns of up to 55% per year in the past three years. On the other hand, NSCs and Public Provident Fund gave riskfree returns of 8% per annum, which was considerably higher than the 5.25% offered by the infrastructure bonds issued by IDBI in March 2005. Incidentally, there has been no public issue of infrastructure bonds after that.

Infrastructure bonds may have died an unsung death, but what we must acknowledge is that this relic of directed savings helped the government rake up the colossal funds needed for the nation’s infrastructural development in the past decade. Of course, the government has now found new ways of raising funds—through taxes and cess on fuel. But we have a long way to go.

The government could consider coming out with an infrastructure bond issue at a rate comparable with the prevailing bank rate. Sure, equity-linked savings schemes have become a big hit with investors but there is still a huge majority of taxpayers who are risk averse and prefer fixed returns.