It is often said that if an offer seems too good to be true, it probably is. But what if the offer is from one of India's most respected banks and a public sector entity to boot? The State Bank of India's announcement of home loans at 8% has customers rubbing their eyes in disbelief. What's more, SBI has promised that the rate will be frozen for the next 12 months. So, where's the catch? As per the fine print, this rate is applicable only to new loans sanctioned before 30 April. The existing home loan customers of SBI do not get any benefit.

| |

|---|---|

| Mukul Kapoor, Engineer | |

| Outstanding loan | Rs 14.08 lakh |

| EMI | Rs 17,134 |

| Interest rate | 10.75% |

| Remaining term | 12 years 5 month |

Still, this is a golden opportunity for the existing borrowers from other housing finance companies to switch from a high rate to a much lower one. Experts say that if the difference in interest rate is over 2 percentage points, it is advisable to refinance a loan. Given that many lenders are charging existing customers between 10.75% and 13% (see table), the new rate offered by SBI is at least 3 percentage points lower. SBI's offer has set the stage for a rate war. It is only a matter of time before others follow suit.

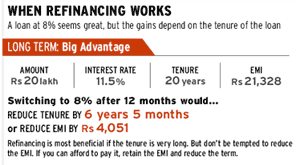

However, the difference in interest rate is not the only criterion that should guide your decision to refinance your home loan. Refinancing involves preclosing the existing loan and applying for a new one, so you need to factor in the preclosure penalty and processing charges also. Typically, the preclosure charges are 2-4% of the outstanding amount, while the processing fee of the new loan is roughly 0.5% of the amount. Financial planners say that you should add the preclosure and processing charges to the outstanding loan amount and then calculate the EMI of the new rate. "Only then can you know whether refinancing is beneficial or not," says Jaideep Lunial, a certified financial planner.Another thing to consider before refinancing is the tenure of your existing loan. Switching to a new rate is most beneficial when the loan has a long tenure of 15-20 years. As the tenure reduces, the benefits taper off. If the loan has less than three years to go, there is hardly any advantage because the preclosure and processing charges eat into the savings from the lower rate.

| How costly is your loan? | ||

|---|---|---|

| Lender | Rate for existing borrowers (%) | % difference over SBI’s 8% offer |

| ABN Amro* | 13 | 5 |

| HDFC** | 11.25 | 3.25 |

| ICICI Bank | 11 | 3 |

| Axis Bank | 10.75 | 2.75 |

| Allahabad Bank | 9.75 | 1.75 |

| SBI | 9.25 | 1.25 |

| Corporation Bank | 9.25 | 1.25 |

| * Loans above Rs 20 lakh; ** Loans above Rs 30 lakh | ||

When you switch to a new loan at a lower rate, you have two options. You can either reduce your EMI or truncate your loan tenure. The first option is tempting because it can ease your cash flow and leave you with more surplus money every month. But it is best to keep the EMI amount unchanged and reduce the loan tenure to optimise the gains from refinancing. In case of SBI, keep in mind that the low rate being offered right now is only for a limited period. After a year, you would be paying the prevailing interest rate. So, don't be lulled into a false sense of comfort. Instead, try to repay the loan as fast as you can.

Before you approach a new lender for refinancing the loan, talk to your own bank first. Chances are that your bank will be willing to readjust the interest rate if you pay the refinance charges. Right now, SBI has not extended the offer to its existing customers. But other banks often allow customers to migrate from one rate to another on payment of certain charges.

In many ways, this is a better option than going to a new lender. For one, you don't have to go through the tedious paperwork or get the property valued all over again. A couple of phone calls and one visit to the bank is all it takes. Revaluation of a property presents its own set of problems. Till last year, banks were willing to lend up to 90% of the value of the property. Today, you get only up to 80%. If you took a loan of Rs 45 lakh to buy a house costing Rs 50 lakh a year ago, and want to get it refinanced, a new lender may not give more than Rs 40 lakh. Worse, if the property price has come down, you may not get even that. So, take all aspects into account when you refinance.