Price: Rs 295 Pages: 316 |  Price: Rs 395 Pages: 366 |

By: Nassim Nicholas Taleb Published by: Penguin group Language: Easy Style: Illustrative and argumentative Visuals: Graphs and tables Target audience: All investors Quick read tip: Skip the technical chapters if you are not number savvy. You will not lose out on the argument | |

Nassim Nicholas Taleb would hate this as he dislikes tracing patterns, but one can’t help draw the parallel. Twenty-one years ago, on 19 October 1987, he was “intellectually vindicated” when the US markets experienced the largest single-day percentage drop of 22.6%. On 29 September 2008, he would have experienced Pyrrhic victory again as the US markets plummeted 777 points, the largest one-day drop in terms of points.

The first fall was completely unforeseen (according to the Taleb thesaurus, such an event is called a black swan), and while the markets had been roiling since this January, the Fall Day in September wasn’t exactly on the radar.

But Taleb had accounted for them. In fact, he actually profited from the first drop (we don’t have the update on his fortunes in the latest crash). That is because he is a “practitioner of uncertainty”, a believer in the unforeseen. He not only sees what has happened, but also what could have happened. Therefore, Taleb can protect against remote, though not impossible, events that can hurt his interests and exploit all rarities that favour him. Taleb recognises randomness without seeking patterns. Which is why he would loathe the attempt to string together two market falls spaced across nearly two decades. Another reason would be that it is a work of a journalist. Taleb hates three sections of society— the media, Nobel awardees and MBAs— because they create maximum “noise” trying to impose a meaning to everything, thus destroying randomness.

The journey into the world of the abstract and the random in Fooled by Randomness and The Black Swan will help you filter out archaic but widely accepted ideas like the Gaussian curve, and see the importance of what does not make news. Why should you put in the effort? Because it is highly probable that you do not understand the impact of probability and black swans in your life unless you are told.

If you factor in probability, history as you know it till now, changes. It is not freed of the hindsight bias, but at least you know that there is one. You realise that Darwinism is not true in all fields of life—that for every computer that became a technological marvel, there are hundreds of trashy machines that never made it. That principles derived from controlled experiments do not pan out in real life. That you just can’t predict, because prediction necessitates knowledge of the future. Effectively, you become an epistemocrat, that is one who suspects his knowledge.

This philosophy is more relevant today as the world becomes an ‘Extremistan’—a cosmos with great inequalities, where one observation, which could be a black swan, disproportionately impacts the aggregate.

By its inherent nature, the world of finance fits this description to the T. The range of variables is very wide. So black swans, like the 1987 US market crash, have a great impact. But we ignore them because of low probability. In an attempt to find a pattern, we indulge in standard deviation calculations, which have nothing ‘standard’ about them as the result will change for different subgroups of the sample size. Going by Taleb’s philosophy, words such as ‘bull’ and ‘bear’ seem superficial. Let’s assume that there is a 70% chance of the market going up and a 30% chance of a decline. You gain by Re 1 if it rises and lose Rs 10 if it declines. A rational investor should be bearish on the market despite a higher probability of a bull run because the outcome of the probability is so different. This asymmetry in results eludes us.

If randomness is so ubiquitous, why isn’t it so obvious? Because our minds are not wired to accept the abstract. Our memory must compress information for storage and this requires the information to be logical— the nemesis of randomness. The cause-and-effect relationship and incorrect risk assessment kills possibilities. Not to forget the ‘gambler’s tick’, our natural reliance on mild superstitions that blocks out the black swans.

The two books don’t merely rhapsodise on randomness but also suggest ways to beat it— by hyperaggression or conservatism towards black swans, depending on their nature.

The content is gripping and you will marvel at Taleb’s tight and racy writing, which blends autobiographical anecdotes with financial jargon effortlessly. Give yourself time to understand his style and it will be fun to jump centuries as Taleb juxtaposes mythical characters with modern researchers.

This is the age of probabalists. Events like the Mumbai terror attack or the current global crisis make us realise that we have to be prepared for the black swans. We must delve into the realm of the unknown and the unexpected. Taleb’s philosophy never seemed so right. It is impossible to summarise these books, so read them. It will be the beginning of knowing what you don’t know—or what the review did not tell.

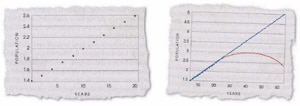

THE NON-RANDOM MIND  Joey seemed happily married. He killed his wife. Which event is more likely? Which is the model that fits the data represented by Graph 1? |

Read our review of the book Investment Fables