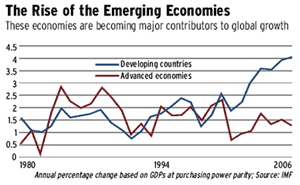

You have heard about the clash of civilisations; now read about the collision of markets. Mohamed El-Erian, argues that the global financial crisis is only the effect. The cause is the process in which "the markets of yesterday collide with those of tomorrow". What lies beneath this meltdown is a series of hand-offs, such as the earlier debtor nations building wealth and buying assets and influence, and new financial products coming into play.

| |

|---|---|

| When markets collide | |

| Price | Rs 350 |

| Pages | 344 |

| Author | Mohamed El-Erian |

| Publisher | Tata McGraw-Hill |

| Target audience | Serious students of investing |

| Quick read tip | Go through the first three chapters, which give a good overview and are bereft of the 'home' bias that comes in later |

| Language | Difficult |

| Style | Academics |

| Visuals | Graphics, tables and charts |

This collision, like all clashes, produces noise. But the crux of El-Erian's argument-and the point relevant to investors worldwide-is that within this noise are signals. The investors who are able to understand these signals are the ones who will be able to prosper in the emerging, chaotic, new economic world order.

El-Erian tries to provide his readers with the anchors, the analytical tools, necessary to find safer havens in the stormy financial seas that they must encounter. He should know. El-Erian is the co-CEO and c-CIO of PIMCO, one of the largest investment management companies in the world. He has also spent 15 years at the International Monetary Fund, and earlier, managed a $35-billion endowment at The Harvard Management Company.

The book is aimed at the mid-level audience- it's too simple for an academician and complicated for the lay reader-and tries to explain that sensible investors too need to observe market data and spot the anomalies. After the screening, investors should analyse the noise episodes, recognising that there will be false positives when they try to find the signals. They must not forget that though most causes will be cyclical factors, occasionally they will be long-term structural changes that will fundamentally alter the approach to be taken.

El-Erian's effort to deconstruct the collision process and our understanding of it is fairly comprehensive; the problem begins when he suggests solutions. He tries to create a simple portfolio that will stand the test of time. Similar to the detailed asset allocation model of David Swenson, who manages the endowment at Yale, this one too has a mixture of low correlated assets. But with the economies intertwined and constant change, the fear is whether the model is sturdy enough.

Also, tactically, each individual needs to change his asset allocation and cannot stick to just one model as a strategy. Though conventional wisdom has been that equity in emerging markets is not too correlated to the US equity, the fact is that the US recession is taking a toll on both the Chinese factories and the Indian call centres.

Similarly, when share prices of a particular company, or even an industry, come down, you see the debt being downgraded (for instance, the construction industry). So having equity and debt, which is traditionally seen as a risk reduction technique, may not help. Besides, the recent craze of stripping all cash flows and creating separate assets out of each has increased volatility and trading expenses while reducing the returns for the end investor.

Another surprising fact is that though El-Erian wants to create an asset allocation plan consistent with forward-looking realities, in Chapter 6, he quotes Jeremy Siegel's study on equity returns and agrees with his historical view that the market offers an attractive 'equity risk premium'. It's a classic example of what Peter Lynch calls 'looking at the rear-view mirror and driving'.

Currency risk, differences in accounting and governing structures, rule-of-law concerns, etc, only find a passing reference. However, it's a fact that there is less disclosure in Japan than the US. In India, shareholders are not given information about any transactions conducted in scrip by top executives, while it is mandatory in the US. The book is clearly aimed at the money managers in the US. Hence, perhaps, the 'home bias' in the portfolio. Could an Indian fund manager (even assuming full convertibility) create such a portfolio? Doubtful.

One cannot feel the 'recency' bias-the allocation to commodities is 11-15%. Swenson allocates 30% to the US securities; El-Erian, just 15%. Swenson has no commodities; El-Erian does. If it's because the commodities market has performed better in the past three years, no logic for the weightage is provided. He talks about construction bias in indexing, passive positioning, identification and assessment, all of which are bound to leave the common investors confused. He also refers to Sovereign Wealth Funds, but doesn't say how they will react to meltdowns.

The book is a neat primer and too good to ignore if you are a serious student of investing. Keep your analytical eyes wide open, but investment expectations low-and you won't be disappointed by the returns.