Investment gurus sprout at the hint of a financial crisis, but their spiel doesn’t necessarily translate into sage advice. So when you come across Parag Parikh’s Value Investing and Behavioral Finance right after the global financial turmoil, you wonder if the market veteran, who penned his first book Stocks to Riches in 2005, merits attention.

The book is not for you if you’re looking to double your money, but go for it if you are an equity investor keen to balance financial intelligence with your emotional quotient. By trying to analyse the human behaviour involved in investing decisions, Parikh tries to induce reason into what can be an ambiguous process for a lot of people.

The book spans 12 chapters, starting with a short, inspiring analysis of success and failure and the reason some people succeed while others don’t, a question we ask ourselves every time we face a setback. People’s unwillingness to delay gratification is what leads to failure, claims Parikh. They also tend to look for the fastest and easiest routes to success without considering the long-term repercussions. The key to riches, he says, is the ability to exert self-discipline and not get carried away by market sentiment. Don’t buy into hot tips and don’t sell when TV analysts talk about the tumbling market. Success can only be achieved if you are willing to stick your neck out and act differently, says Parikh.

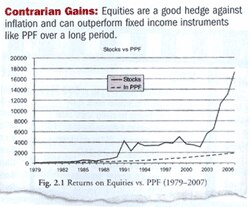

Chapters 3 and 4 carry strong evidential data supporting value and contrarian investing, which Parikh advocates. While investing in equities is considered riskier than in bonds, in reality, inflation could eat into the returns of a fixed income even as equities offer a hedge against inflation (see Contrarian Gains). Only, in case of the former, the return, or the interest component, is known, while the return from equities can be volatile as the prices are driven by earnings growth and investor sentiment.

The change in PE ratios is nothing but a change in psychological behaviour, says Parikh. No wonder you often see a deviation in corporate performance and shareholder performance. This is supported by data for 1994-97, where company earnings grew at 36% compound annual growth rate, whereas shareholder return was only 2.7% (after dividends), which is an anomaly. The data for 1994 shows that the year was marked by extreme optimism, with investors willing to pay high prices, resulting in high PE ratios. Then, 1995-97 saw rationalisation of prices and subdued returns. Had investors entered the market during this period, the returns would have been higher. It is the acquisition price that determines market returns, otherwise you would be trapped in the growth phase, says Parikh.

Such irrational exuberance prevailed again in the Indian stock markets in 2008-9 when investors ignored the signs of global doom. The lesson: for a rational investor who thinks in terms of the business behind the stock, the best time to buy is when it is available at a deep discount to its value.

As Parikh’s book was completed in May 2008, the data may seem dated, especially in light of the market volatility in the first half of 2009. Yet, Parikh has captured various bull and bear market periods, drawing inferences that will help investors take informed decisions.

{mosimage}Since we seem to be entering a phase of exuberance, it may be worthwhile to note some of his mantras. The majority of IPOs, says Parikh, are a product of the bull market. Promoters try to make the most of this time by offering stocks at high prices, making IPOs redundant for a value or contrarian investor. Be it the bull market of 1993-96, the IT sector boom in 1999-2000 or the period starting 2004, the maximum amount of money was raised during these periods. “New issues earn lower returns for investors than comparable stocks,” says Parikh.

If you want to identify a bubble or the strategies to adopt when the market is unrealistically high, read chapter 11. Many of Parikh’s mantras seem rhetorical and may not be actionable. Psychology plays an important role in driving decisions and a conscious effort needs to be made to think differently, which is difficult, not impossible.

Those familiar with Daniel Kahneman would relate to Parikh’s behavioural finance theories. In fact, he refers to noted investment gurus and their strategies. A hint to speed readers: as you rate your financial and emotional quotients, pick one topic at a time. It will lessen the data overload.