Why Nations Fail. K.P. Krishnan, the Indian finance ministry's point man for all things capital markets, is re-reading the book by two US economists Daron Acemoglu and James Robinson. Krishnan's second dive into the acclaimed book since its release last summer is to find answers to the deep problems his employer, the government of India, faces with

an economy in a tailspin. The answers are simple, really. The Massachusetts Institute of Technology and Harvard economists argue that the economic success - or failure - of a country depends on the strength of its political and economic institutions.

But an anodised steel-like institutional framework is something India sorely misses. Years of political ineptitude have corroded the resilience of the world's thirdlargest economy by buying power. This despite warning lights on the government's dashboard going off regularly for at least two years now. When it rains, it is said, it pours. By the time India's stock markets closed on August 16, trading desks were in shock - the Bombay Stock Exchange's benchmark index, Sensex, had lost nearly four per cent, the sharpest single-day fall in four years.

The gradual decline began in early 2008, after the rupee-dollar rate touched 39. The rupee has been floating down like a feather against international currencies for nearly four months now. Between April 30 and August 23, Indians had to pay nearly one-fifth more for the US dollar, the world's preferred currency. The dollar was worth Rs 63.22 end of trades on Friday, August 23, and Deutsche Bank predicts it could touch Rs 70 in a month. Credit Agricole says it will not recommend buying the dollar at below Rs 75.

Krishnan, the bureaucrat who was part of a crack team that decided on India's response to the 2008/09 global meltdown, was anything but rattled at a recent seminar in Mumbai. At least, he didn't show it. The battered rupee, he said, "is a passing threat… this is a short-term threat." The next day, August 21, the pound sterling breached the Rs100 mark. The Indian currency has depreciated nearly one-fourth vis a vis the pound sterling since mid-March: Rs80.71 on March 12 versus Rs100.32 on August 23.

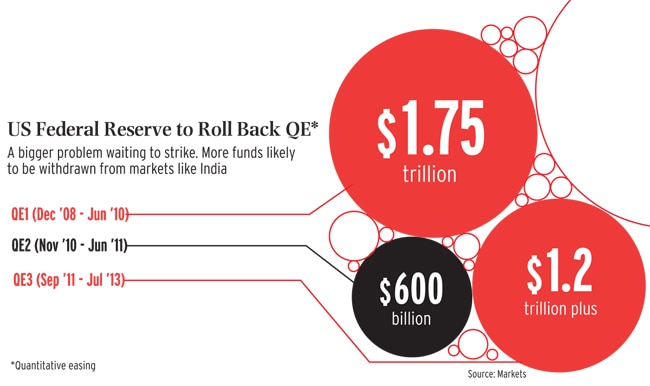

With its current account deficit (CAD) - the difference between exports and imports of goods, services and transfers - at an all-time high and a currency that had not shed value despite years of high inflation, it was only a matter of time before investors lost their unbridled optimism from the days of a once-robust economy. The trigger for that volte face came from half way across the world. On the back of intermittent signs of a recovery, the US Federal Reserve has hinted the end of low-cost money on tap, which means monetary tightening and consequent rise in the interest rates there. That was the cue for global funds to suck back billions back into the world's biggest economy from emerging markets. India was not spared. Between August 16 and 22, nearly foreign institutional investors were net sellers of Rs2,975 crore worth shares. FIIs are restive in other markets such as Indonesia, Brazil and Mexico.

Vulnerable IndiaClearly, the

Indian economy is in a much more vulnerable state than it was at the start of the financial crisis in September 2008. Then, India had a credible response to the meltdown set off by the collapse of investment bank Lehman Brothers. In a series of measures, the government infused liquidity into the system, cut duties, and overall boosted demand. The stimulus cost an estimated Rs 1.85 trillion. (One trillion equals 100,000 crore.) Such spending could be afforded only because India was growing at a fast clip: GDP growth was 9.4 per cent in 2006/07 and 9.3 per cent 2007/08, the two years preceding the Wall Street meltdown. And tax revenues had jumped 20 per cent in each of the years. The stimulus worked wonders: after a relatively slower GDP expansion of 6.7 per cent in 2008/09, growth bounced back to 8.6 per cent and 9.3 per cent each in the following two years.

Cut to today: GDP is growing at a much slower rate of five per cent with predictions that it will dip to a sub-five per cent level. Which means, the state treasury is looking less healthy, especially when expenses are rising at an unexpected pace. For instance, India sets aside more than one-third of its import bill for crude oil imports. Oil prices have risen about $12 a barrel in the last three months - a $1 increase in crude prices is a $900 million hole in India's trade balance - but they are expected to stay around $110. That's the good news but the bad news is that some 20 million tonnes per annum (mtpa) new refining capacity coming up in the West Asia region will mean a lower demand for India's fuel exports, which brought in nearly $59 billion in 2012/13.

If that's not all, the impact of the depreciating rupee will blow a hole in India's finances. "In rupee terms, if this slide continues, the effect will be huge," says Vandana Hari, the Singapore-based Editorial Director at energy specialist Platts Asia. Each rupee that the Indian currency depreciates on the US dollar, Rs10,000 crore gets added to the country's import bill (about Rs6.7 trillion in 2012/13). The dollar has become expensive by nearly Rs 11 since May. CAD, at $88 billion was 4.7 per cent of GDP in 2012/13, nearly double the 2.5 per cent level that RBI thinks is sustainable. Finance Minister P. Chidambaram is confident he will keep CAD under $70 billion this fiscal year but not all - the markets, for sure - are convinced.

Much of that scepticism emanates from what some think as policy failure over rising gold imports in recent years. Today, gold is the second largest import item after crude and petroleum products, beating electronics to third place. The surge in gold imports is both a consequence of unabated inflation which gold is used as a hedge against, and a rise in prices of the yellow metal. CAD is usually covered by foreign inflows - both institutional investors and foreign direct investment (FDI) - or by dipping into the country's forex reserves.

With capital flows drying up, India will tread the slightly-risky path of using debt to finance CAD. "We have no option but to rely on debt inflows in the immediate term," says Paresh Sukthankar, Executive Director at HDFC Bank. A recent report by ratings firm CRISIL showed corporate India had a outstanding foreign exchange debt of over $200 billion as of March 2013, of which close to 45 per cent is short term. The short-term foreign debt outstanding in March 2013 is nearly $100 billion, which is to be redeemed by March 2014. Forex reserves stood at $279 billion as of August 13.

In simple terms, this means a 2008-like strategy is not an option before India. "After and in 2008 and 2009, we survived because of the stimulus, which was a consumption stimulus. But we are not in that position anymore," says Devendra Kumar Pant, Chief Economist, India Ratings and Research.

The government's response to the rising CAD and overall sagging economy has proven to be too little, too late. To be fair, Chidambaram saw things early. Soon after he moved ministries to Finance from Home in July 2012, the government took bold decisions on easing rules for business - widely billed as "reforms 2.0". The reference was to the first set of economic reforms that Manmohan Singh, today prime minister, ushered in as finance minister in 1991.

Chidambaram was at the forefront of the changes announced that seemed to shake the government out of the stasis it was in. With an aim to trim subsidies, diesel prices were raised by Rs5 a litre and supply of subsidised cooking gas was capped. Up to 51 per cent overseas ownership was allowed in multi-brand retail and 49 per cent FDI permitted in airlines. Other changes eased FDI in telecom and oil and gas. But save for the Rs2,058-crore deal between Abu Dhabi-based Etihad Airways and India's Jet Airways, little came by way of foreign inflow. Without growth, foreign investors will shun India, says Samiran Chakraborty, Head of Regional Research, South Asia, Standard Chartered Bank. "The message that is going out is that we will push for reducing inflation and financial stability, and that growth is sacrificial." So much so that the government's recent measures of higher import duties on gold and silver, clamping down on foreign investment by companies, easing external commercial borrowings limits, and permitting quasi sovereign bonds have had little effect on the ground.

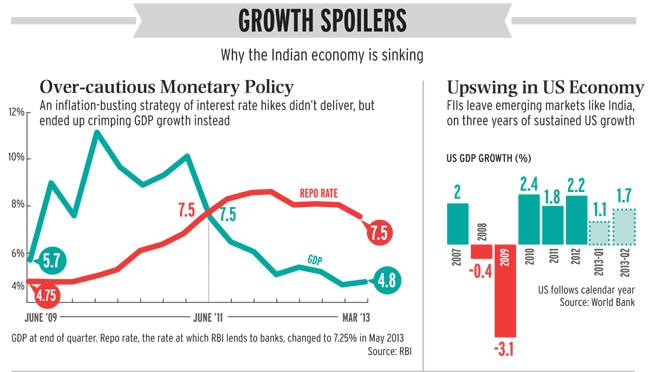

Caution: Pain AheadPartly, it is monetary policy that tripped Chidambaram's efforts over the past year. In much of his five-year term, RBI Governor D. Subbarao, due to retire on September 4, single mindedly waged a war against inflation. Questions are now being raised on the pace of interest rates hikes and whether his stance on inflation, widely seen more due to India's supply constraints and less a function of excess money sloshing around, was the optimal one. In the second week of August, in a debate in the Rajya Sabha on the state of economy, Chidambaram said the RBI must focus on growth and employment.

But that is easier said than done with consumer price inflation running in double digits for over a year. A direct casualty is crimped household consumption and savings. Even wholesale price inflation, indicative of the pace of price rise in the broader economy, which was on a downward spiral for some time, has started to inch up and is hurting business.

Gujarat food processor Kamdhenu Foods is unable to take large orders in recent months. "We couldn't accept an export order for 6.5 tons of bitter gourd slices because its price has jumped up from Rs10 a kilo three months back to Rs25 a kg now," says Bipin Shah, General Manager.

With fuel prices set to rise soon, bankers say resultant inflation will again put pressure on interest rates. The recent monetary tightening is already having a spillover impact: Axis Bank, HDFC Bank and ICICI Bank have hiked lending rates.

The banking sector, already under stress due to higher bad loans, is getting shocks from new industries as the effects of a decelerating economy spread. State Bank of India, the country's largest lender, got a shock in the first quarter of 2013/14 from the rising slippages in the agricultural sector. There is another looming danger in infrastructure loans. "There are issues of asset liability mismatches in the banking industry because of shorter maturity deposits and longer term loan to infrastructure companies," says S. Viswanathan, a managing director at SBI.

Unfortunately for India, then, options that will yield immediate benefits are limited. The economy is unlikely to shake off its sluggishness in the medium term - until 2015/16 or even later, according to some. Sonal Varma has a list of big ifs to see the needle will move on the economy. "If you start making the right moves, if there is change of guard and if there is a clear focus in reviving growth, it will take about 12 to 18 months for things to start turning," says Varma, Executive Director and India Economist at Japanese financial house Nomura. "The rupee is a symptom of the problem, there is a crisis of confidence and the credibility of policymakers has taken a hit."

The Congress Party-led United Progressive Alliance government just does not have enough time or numbers with to kickstart large-scale reform measures with general elections scheduled before the summer of 2014 and key sections of the UPA are already in election mode, as also the principal opposition coalition, the National Democratic Alliance, led by the Bharatiya Janata Party. Result: a polity distracted from the needs of the economy. "We don't have a thought leadership for the society that will emerge tomorrow. We need to do quite a few things to make this [growth] work," says Kishore Biyani, Chairman at retailer Future Group. Pre-election surveys show regional parties gaining strength at the hustings, likely increasing political instability at the Centre - which doesn't portend well for the economy.

Where does the economy go from here? GDP growth is already at a 10-year low of five per cent in 2013/14 against 6.2 per cent the previous year. CRISIL is downright bearish. "All our forecasts - growth, inflation, fiscal deficit and CAD - are under revision and they will be revised unfavourably," insists D.K. Joshi, Chief Economist at the firm. One voice sounds ominous ahead of the release of GDP data for the April-June quarter on August 30. "The way the Indian economy is going, it is testing my optimism," Kaushik Basu, Chief Economist, the World Bank, said recently at a seminar in New Delhi. Basu, who was Chief Economic Adviser to the government of India until a year ago, is predicting a 4.8 per cent growth for April-June.

Still, two factors hold out some hope. The biggest drag on the economy comes from the services sector and industries, which together make for about 85 per cent of India's GDP. But it is agriculture, despite its smaller contribution to the economy, which could stop the economy from stalling. The Indian Meteorological Department has recorded normal to excess rainfall in 30 of the country's 36 meteorological sub-divisions between June 1 and August 14. The area-weighted rainfall has been 13 per cent above normal.

There has been a notable rise in area under cultivation of pulses (25 per cent more), coarse cereals (15 per cent) and oil seeds (15 per cent) this season from 2012/13. Total crop area sown has increased over nine per cent. "If you compare agriculture output, we will achieve the same growth that we did in 2011/12, which will have a deeper impact on inflation," says Himanshu, an agrieconomist who teaches at New Delhi's Jawaharlal Nehru University. (He goes only by his first name.) Farm output in 2011/12 grew 2.5 per cent from the year before - it was 1.9 per cent in 2012/13. Nomura has a four per cent target for agriculture this year. "I expect very strong agriculture growth this year, which should help the rural economy," says Adi Godrej, Chairman of the locks-toshampoos Godrej group. Farming is the primary economic activity for some 70 per cent of Indians.

The second set of strands in the wind that augurs well for the economy is the five state polls and the general elections. Odd as it sounds, elections are good news for the economy, for money - often black, unaccounted for cash that otherwise will not find its way into the system - boosts growth. "Five states are going for election, and with a general election, election spending will provide a stimulus," says Ajit Ranade, Chief Economist at Aditya Birla Group, which runs metals to telecom businesses. Other small gains to be had in the coming quarters include the impact of a falling rupee on exporters.

Then, there is the man being billed as the one with the silver bullet: Raghuram Govind Rajan. The RBI governor-designate has not spoken of his new assignment and little in his academic past indicates his monetary DNA, if any. But the street has already set expectations for him. In the first six months, says Rajesh Mokashi, Deputy Managing Director at ratings agency Care Ltd, Rajan's priority should be to balance inflation and growth dynamics. In the longer term, he should focus on asset quality in banking, fix potential asset-liability mismatches on bank books, and issue new banking licences.

Time will tell if Rajan can deliver growth even while reining in inflation. But, to be sure, India's fundamentals are strong in the medium and long term. Hundreds of thousands, if not millions, are joining the middle class even at a five per cent rate of GDP expansion. Its workforce is adding a million every month, making it the youngest among major economies. Sanjeev Sanyal, global strategist at Deutsche Bank in Singapore, points out that China has reached the end of its demographic boom. "This offers a good opportunity for India to take the place vacated by China," he says. But, he adds, India has to get its act right in terms of governance, property rights and primary education. In other words, building institutions - the biggest takeaway from Why Nations Fail. Sometimes the best fixes are found in truisms.

BT RETRO

|

| {mosimage} | {mosimage} | {mosimage} |

| More than two and a half years ago, Business Today warned in its cover story India Slowing, that the Indian economy was showing worrying signs (Feb 20, 2011.) Further cover stories tracking the decline include Watch Your Step (July 8, 2012) and Stepping Over the Edge (Oct 14, 2012). See businesstoday.in/archives-sep1513 for previous stories |

Additional reporting by Anilesh Mahajan, Taslima Khan and Suprotip Ghosh.

Research inputs by Jyotindra Dubey