It’s easy to fall into the lull of complacency. It’s easier to think that you have taken care of all contingencies and disruptions while figuring out your earnings, savings and spending. But in times of uncertainty, as is the case now, it becomes impossible to predict immediate trends.

So, each one of us can discount many downsides, get wrongly swayed by the crowds, make logical but wrong calculations, and incorrectly think that only others will flounder. Money Today presents a list of ten most likely—and deadly—sins, and also the solutions to help grapple with them.

|

Of course you want decent returns on your investment. A diversified equity mutual fund is a good bet; we have said it often enough on these pages. But consider this. If you had invested Rs 10,000 in such a fund in August last year, it would have lost 6.42% in 12 months.

That would leave you with Rs 9,358, which you might choose to withdraw now. But what would you do with it? Buy an appliance that cost Rs 8,500 last year? Thanks to the 12% inflation, the same appliance will cost about Rs 9,500 today.

Not a very pleasant thought, is it? Abhay Joshi agrees. A technical consultant, Joshi prided himself on his financial acuity, until he realised that inflation had deviously eaten away much of his household budget. In the past three months, his routine expenses have shot up by almost 40%, and he has had to go slow on repaying a personal loan. “Though I spend carefully, my monthly surplus is continuing to shrink. So I can’t prepay my loan,” he says.

He is unable to buy the electronic goods that he wants to because he’s finding it impossible to stretch his household budget to meet even the regular expenses. |

Solutions • Estimate inflation according to your consumption pattern. • Overestimate inflation and underestimate investment returns. This automatically creates a safety net for your financial plan. • Review inflation estimates when prices rise sharply, so you know if you have enough to meet short-term goals. |

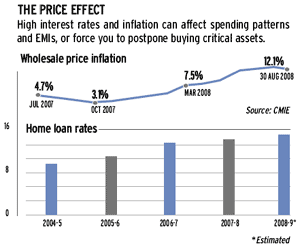

Joshi is not alone. All acrossp the country, people are fighting a losing battle against sky-rocketing prices. And it doesn’t look like things will get better in a hurry. The Wholesale Price Index (WPI) of the week ending 30 August was 12.1%. It has been in the double digit zone for 14 weeks. Home loan rates have increased by 1.5% in the past eight months leading to an extension of mortgage tenures or rise in EMIs. Add a bearish market to the mix and we have the perfect recipe for falling standards of living.

Everyone is quick to blame the various government policies, economists and the like for this situation. But that’s not going to pay your bills.

Financial trainer P.V. Subramanyam, says, “People should understand that headline inflation is not the inflation that affects them. Personal inflation depends on your personal consumption basket.” For the urban consumer who practically lives on branded goods, this figure is way above the one that is publicised.

Most investors, for whatever reason, prefer to think of inflation as something that might affect the value of their longterm investments. Sadly, price rises don’t follow this line of logic. As we have seen in the past few months, prices have beaten even the most dire predictions. This has an immediate impact on saving for shortterm goals (see “Moving out of reach”).

The other common mistake investors make is to leave very little wriggle room when it comes to budgeting monthly cash flows. This means that generally there’s no cushion that can pad the shock of spiralling prices.

So yes, you need a cushion. But many investors decide that money in the bank serves the purpose. Subramanyam strongly disagrees: “Letting substantial sums idle in a bank account that gives barely 3.5% gross interest is criminal.”

MOVING OUT OF REACH How inflation hurts your short-term goals | |||||

| After 2 years | |||||

| Goal | Inflated Value (Rs) | Sip* Required (Rs) | |||

| Current Cost (Rs) | 5% Inflation | 9% Inflation | 5% Inflation | 9% Inflation | |

| Car | 3 lakh | 3,30,750 | 3,56,430 | 12,262 | 13,214 |

| Admission Fee | 6 lakh | 6,61,500 | 7,12,860 | 24,524 | 26,428 |

| * A systematic investment plan that earns 12% pa | |||||

|

A life insurance purchase is difficult and I have made my share of mistakes when I initially bought life insurance. My first mistake was to be intimidated by the complicated financial numbers that were shared with me. I did not ask adequate questions, or invested enough time to understand the policy’s features. As a result, a few years ago, when I needed some money, I was dismayed to learn that the policy had high withdrawal charges and I would not even get my capital back if I withdrew money any time over the next 10 years.

The second mistake was to attempt to combine multiple objectives of protection, investment and savings into one plan. What I ended up buying was a plan that provided neither the best protection nor the best investment or savings. My objectives would have been better served had I purchased a protection-oriented plan and also invested in a post-office scheme.

My third mistake was to not enquire about the riders and supplemental benefits available with the product. Several of these products such as critical illness riders would have been good purchases to make.

But I learnt a lot from these mistakes. We spend our hard-earned money and we must know what we are buying. So ask as many questions as required. It’s particularly important to get a policy illustration in writing from the company and to understand all the terms in that illustration. Have simple and clear financial objectives. Protection and security come first. Investment and savings needs should be secondary. Ask about riders and product combinations available with the insurer.