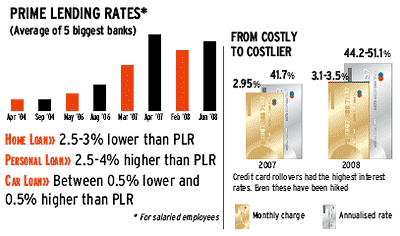

The EMI for your home loan isn’t the only thing that has put on weight this summer. With most banks hiking their prime lending rates by 50-75 basis points, all loans have become more expensive. Mercifully, most other forms of loans are not on a floating rate. So, the EMI of a car or personal loan taken last year won’t change, come hell or high water. Only new customers will have to shell out more. But some education loans are on floating rates and can be affected.

What should you do when interest rates shoot up? One way to weather the storm is to consolidate your debt under a relatively cheaper borrowing option such as a loan against property. Loans taken against a collateral (property, gold, securities) are generally cheaper than unsecured loans such as personal or education loans. Use this option to retire high-cost debt.

If you have more than one outstanding loan, attack the one with the highest rate and the longest tenure. Just as long-term investing can produce wonderful results for the investor, long-term debt can be ruinous for the borrower. Also, weigh your options before you foreclose the loan. There is a pre-payment penalty on some loans.

In these times of high interest rates, rolling over the credit card balance or using plastic power to withdraw cash should be avoided. Credit card rollovers are the most expensive loans. On an annualised basis, it works out to about 50%. Use this facility only when all other options have been explored.

Interest rates: 16-24% (depending on the borrower's profile)

Tenure: 12-60 months

Pre-payment penalty: 3-5%Some banks allow pre-payment of a portion of the outstanding amount (usually 25%) without any pre-payment penalty after 6-12 months from the date of disbursal

Interest rates: 12-14% (Many banks offer a concession of 0.5-1% on the interest rate for female students)

Tenure: Repayment starts one year after course completion or 6 months after obtaining employment (whichever is earlier)

Pre-payment penalty: No penalty for pre-payment. Many banks offer a 1% concession if interest is serviced during the loan holiday period

Interest rates: 16-24% (depending on the borrower's profile)

Tenure: 12-60 months

Pre-payment penalty: 2-3% of the outstanding amount

Interest rates: 13-15% (depending on the borrower's profile)

Tenure: 1-20 years

Pre-payment penalty: 2-4% of the outstanding amount