On October 9, the Bombay Stock Exchange

(BSE) Sensex rose 265 points and ended the day at 20,249. It was one of the several instances this year when it crossed the 20,000 mark. As we write this, the index is again within the shooting distance of its all-time closing high of 21,005. Will it cross the milestone?

As market experts play the guessing game, investors are looking for answer to a question that is as old

as stock markets themselves - is this a good time to buy equities, especially when economic data show a wobbly economy that cannot possibly support a sustained market rally?

However,

having equities in the portfolio is a must if one wants to earn returns that are above the inflation rate. So, before we bring to you sectors and companies that stock analysts say offer a margin of safety in this market, let's listen to the views of experts.

"We remain concerned about the markets reflecting the weak macroeconomic situation and peg the

March 2014 Sensex target at 17,000, implying a 15% downside." -Basab Mitra, chief executive officer, Capital Markets & Wealth Management, Religare

"The positive impact of rupee depreciation on various sectors, government initiatives to push up growth, US economic revival and reasonable valuations will not allow the markets to fall substantially." - Sunil Jain, head, equity research, retail, Nirmal Bang Securities

"We believe that fears related to tapering of the US Quantitative Easing, or QE, programme have been overdone. Emerging market equities and currencies bounced back after these fears receded. With macroeconomic data on the mend, we expect Indian equity markets to move with a positive bias in the short to medium term." - Varun Goel, head, portfolio management services, Karvy Stock Broking

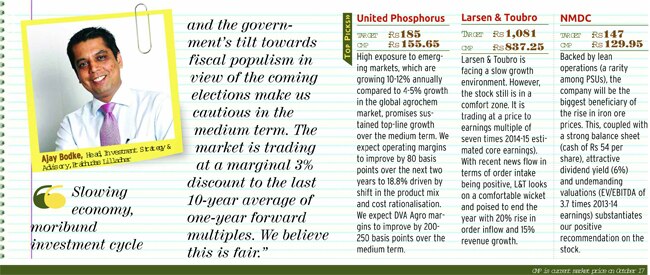

"Slowing economy, moribund investment cycle and the government's tilt towards fiscal populism in view of the coming elections make us cautious in the medium term." - Ajay Bodke, head, investment strategy and advisory, Prabhudas Lilladher

"We are of the opinion that the (Q2) number flow from hereon will be encouraging and should ensure a slow P/BV rerating of the indices." - Sandeep Shenoy, executive director, institutional research and sales, Anand Rathi Financial Services

The above comments show that experts are not in agreement about where India's stock markets are headed. In fact, the markets have been directionless and moving in a range for quite a while, with bursts of extreme volatility in between. For example, on August 16, the Sensex crashed 769 points, the steepest fall in four years, on fears the US Fed may announce tapering of the QE programme that it has been using to inject liquidity. A month later, on September 19, it rose 684 points when the Fed surprised by leaving the programme unchanged.

The market is keeping everyone guessing. Uncertainties on both domestic and global fronts are also creating unease. For instance, domestic indicators are not positive, with industrial production rising just 0.6% in August and wholesale inflation at 6.46%, much above the Reserve Bank of India's, or RBI's, target. The latter has led to fears that the RBI may raise interest rates, hitting bottom lines of companies.

"Divergent growth and inflation trends have been precluding the RBI from taking a directional stand on interest rates over the past six-nine months. Just recently, the new RBI governor took a firm stance by increasing the policy rate to anchor inflationary expectations. This will be negative for growth and corporate earnings and, therefore, for equity markets," says Rajiv Mehta, assistant vice president, research, India Infoline.

There is also a likelihood of the central government not taking big decisions in view of the elections in five states, followed by general elections in the second quarter of 2014.

The market will keenly watch fiscal deficit and current account deficit (CAD), though steps to curb gold imports and higher export growth will lower the CAD. The CAD for quarter ended June was 4.9% of gross domestic product compared to 4% in the same period of the previous financial year

The market will also keep a keen watch on global factors. The principal among them is QE tapering. "The tapering, on hold for the time being, is likely to haunt the markets in December. US recovery is gaining strength and could prompt the Fed to start marginal tapering after its next policy meeting. This can lead to uncertainty around portfolio inflows for emerging markets like India and destabilise the currency," says Mehta of India Infoline.

Mahesh Patil, co-chief investment officer, Birla Sun Life AMC, says QE tapering may lead to more foreign institutional investor, or FII, outflows. "The impact will be felt across emerging markets and India will not remain unscathed. However, to a large extent, a lot of money has already moved out due to tapering fears. We could see more outflows when the tapering actually starts. While FIIs could alter allocations based on global risk-on/risk-off events, the structural preference for India will not alter, and we will continue to see net inflows in times to come," he says.

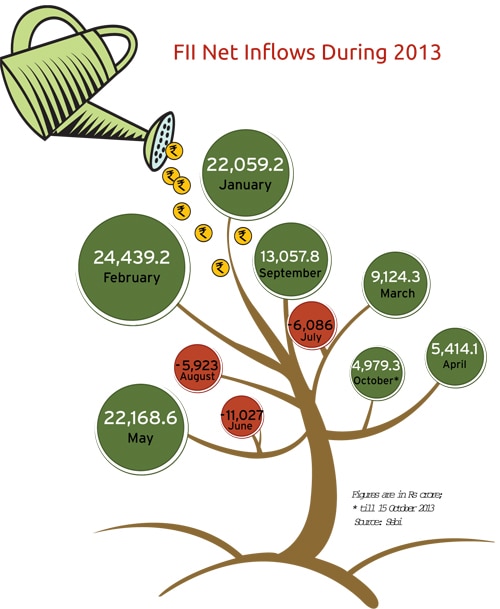

FII inflows this year have been lukewarm compared to 2012. As on October 13, they amounted to Rs 72,617 crore. With less than three months remaining for the year to end, this amount is just 57% of Rs 1,28,360 crore that India got in 2012.

Karvy's Goel says FII inflows are likely to rise only when there are definite indications of growth. "In the short term, tightening of monetary policy is going to slow economic activity. We are expecting growth of around 5% for the financial year with sub-5% growth in the first two quarters. We expect FII investments to resume once there are definitive signs of growth revival," he says.

IN A RANGEThe question every equity investor is asking is: Which way are the markets headed? Is there a likelihood of a clear direction emerging, one way or the other? The general view on this is that the markets will remain rangebound in the short term.

"We expect volatility and lack of direction till the end of the year. We do not envisage the 5,400-6,200 range being broken decisively in the aforementioned time. While domestic macros are expected to remain weak, global factors are dynamic and fragile. In our view, the markets will enter 2014 with much more clarity on both these counts. Also, by then we will have a sense of the emerging political trends," says India Infoline's Mehta.

Jain of Nirmal Bang Securities agrees. "We feel that the markets are likely to remain in this range for at least the next three months." Giving reasons for this, he says that on the one hand, rising rates, slowing growth, political uncertainty and global factors will not allow the markets to rise, while on the other hand, the positive impact of rupee fall on sectors, government steps to revive growth, US rebound and reasonable valuations will not allow the markets to go down substantially.

Karvy's Goel, however, has a different take. "We believe that fears related to tapering of the QE have been overdone. Emerging market equities and currencies have bounced back after these fears receded. With macroeconomic data on the mend, we expect Indian equity markets to trade with a positive bias in the short to medium term," he says.

A possible trigger for direction could be the second-quarter results of companies. Healthy growth in net profits is likely to break the monotony and push the markets to fresh highs. "The sideways trend will continue for some more time and probably receive a trigger after the second-quarter numbers are out. We are of the opinion that the number flow from hereon will be encouraging and should ensure a slow P/BV re-rating of the indices and building up of steam in the coming quarters," says Shenoy of Anand Rathi.

For quarter ended September, Infosys grew top line by 25.78% to Rs 11,482 as against Rs 9,129 crore in the corresponding quarter a year ago. However, net profit fell 0.68% to Rs 2,326 crore, as against Rs 2,342 crore in the same period a year ago.

FAIR VALUEThe broader market, in terms of valuation, is in the fair zone, say experts. "The Nifty is trading at 14 times one-year-forward earnings of Rs 420 (for September 2014). Last 10 years' average for oneyear forward multiple for the Nifty is 14.5. So, the market is trading at a marginal 3% discount to the last 10-year average of one-year forward multiples. We believe this is fairly valued," says Ajay Bodke, head, investment strategy and advisory, Prabhudas Lilladher.

Jain of Nirmal Bang Securities agrees. "The Nifty's valuation on the price to earnings (PE) multiple is 14 times 2013-14 earnings per share or EPS. The average one-year forward multiple of the last seven years is 15.25. For the last one year, the valuation has been 15.25-12.5 times oneyear forward PE multiple. As such, the markets are reasonably priced," he says.

Goel of Karvy sees an upward movement based on current valuations. "The Sensex EPS is expected to be Rs 1,333 and Rs 1,495 for 2013-14 and 2014-15, respectively. Assuming a multiple of 15 times 2014-15 earnings, we get our base case level of 22,425 for the Sensex by the end of 2013-14," he says.

Dipen Shah, head of private client group research, Kotak Securities, says a rise in valuations is dependent upon how growth shapes up. "Looking at the consensus estimates for 2013-14 and 2014-15, benchmarks are quoting at 15 times and 13.6 times, respectively. While these are around the long-term average, the underlying growth rates are low. To that extent, we believe these valuations will sustain and improve only if growth rates rise. However, if there is an adverse local/global event, there can be a downside."

MAKING GAINSWhat should investors do during such times? Experts say opportunities to make money are there in every kind of market. "To beat inflation, one must invest in equities. It is not easy to earn in this market, but if one follows a few simple rules, one can make money in the current market as well. Since the market is in a range, if the investor buys towards the lower range and sells around the upper range, he can generate reasonable returns," says Jain of Nirmal Bang.

Jain advises investors to be selective in their bets. "One needs to select quality stocks and hold them patiently. Also, one needs to have the courage to sell when there is euphoria in the market."

Shah of Kotak Securities advises investors to check the quality of the management before investing. "We adopt a bottoms-up approach. We prefer companies with ethical managements, strong balance sheets and reasonable valuations. Industry leaders even in distressed sectors are also good bets for the long term."

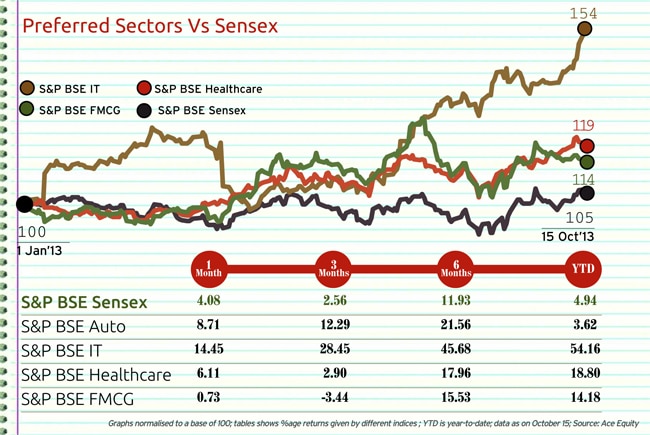

But what are the good bets in the present market? Experts seem unanimous that the best investment bets are in information technology (IT), pharmaceutical and fast-moving consumer goods (FMCG) sectors. "The sectors which offer capital safety will be the ones which can attract investor interest. IT, pharma, FMCG and select automobile stocks score high on this," says Shenoy.

Varun Goel of Karvy adds telecom and private sector bank stocks to the list. "We are positive on pharmaceuticals, IT, FMCG and telecom sectors. We believe these will show good earnings growth. Selectively, even auto companies and private sector banks have begun to turn attractive," he says.

Like Nirmal Bang's Jain, Rajiv Mehta of India Infoline says the key lies in picking the right stocks. "Exposure to defensive sectors such as IT, pharma, telecom and FMCG will help you perform better than the market in the near term. However, stock-picking in these 'safe haven' sectors will be the key, as some companies enjoying rich valuations are witnessing growth and margin headwinds. While we don't see any trigger for bounceback of the cyclicals, they are unlikely to be further hammered either given the historically low valuation of many of them. On the contrary, we feel that the next three months could be an opportune time to accumulate resilient companies in financial and infrastructure sectors."