Scale has always fascinated Future Group Chairman Kishore Biyani. The bigger, the better. In 2017, when he unveiled his ambitious Retail 3.0 strategy, he articulated his dream of creating a $1 trillion business by 2047. At that time, the world's biggest retailer Walmart generated $485 billion in revenue, a little less than half of Biyani's ambition. But Biyani was banking on a modest year-on-year growth of 20 per cent per annum for his then Rs 20,000 crore empire.

His recipe for greater scale: service every possible consumer. First with 70,000-1,00,000 sq.ft. big-box retail stores, Big Bazaar. Second, in local areas through 2,000 sq.ft. small-format neighbourhood stores, EasyDay (he targeted 10,000 tech-enabled EasyDay stores by 2020). And third, create an online marketplace where these stores could access Future Group's entire retail inventory. Alongside, he wanted a consumer play as well. His excitement about the group's fledgling FMCG business, Future Consumer, was particularly infectious. He dreamt of scaling up the Rs 2,000 crore business to Rs 20,000 crore by 2021.

Three years down the road, those dreams lie shattered. With profits dipping 11.24 per cent to Rs 619 crore in the first nine months of FY20 (it is yet to declare full-year results), the group's woes came out into the open in the last quarter of FY20. Slowdown and an uncertain future amid lockdowns have crippled his ability to service loans, drowning him in Rs 13,000 crore of debt. Biyani is staring at sure-shot bankruptcy.

There is a temporary reprieve, thanks to the loan moratorium and one-year suspension of the Insolvency and Bankruptcy Code(IBC). Had it not been for the coronavirus lockdown, Biyani's companies would have been facing insolvency. He had a March deadline for repayment of dues. But the Reserve Bank of India's loan moratorium has provided a breather. In mid-May, the Centre also exempted all Covid-related debt from the definition of default under the IBC and suspended fresh initiation of insolvency for up to a year. In this one-year period, the lenders will not be able to recommend Future Group companies for insolvency, even if they default on loan repayments. Instead, the loans will have to be restructured, by taking out the unsustainable portion.

But the business is already unsustainable and Biyani is on the negotiating table to exit - in full or in part. While Reliance Retail remains the frontrunner, two Amazon-backed consortia of Premji Invest or Samara Capital may also emerge as dark horses. Sources say a deal is likely as early as end of July. One of the plans discussed by negotiators of Reliance Retail and Future Group is a complete share swap. It is not clear how the swap will be designed as Reliance Retail is not listed while Biyani has six listed entities. The deal will lead to Biyani's exit from the retail business.

This is not the first time Biyani is struggling with debt. Nearly a decade ago, in FY12, he was in an identical Rs 12,000 crore debt soup. But he extricated himself by selling his most valuable asset, Pantaloons Retail, to Aditya Birla group for Rs 1,600 crore. He also sold Future Capital to Warburg Pincus for Rs 4,250 crore and his stake in apparel brands BIBA and AND. But this time, the chances of a comeback are dim. "The big difference this time is that we are in a recession globally. He was able to make a comeback in 2012 as market dynamics were strong. This time, he will be lucky if he gets money to just square off the debt," says the CEO of a leading FMCG company.

In Dire Straits

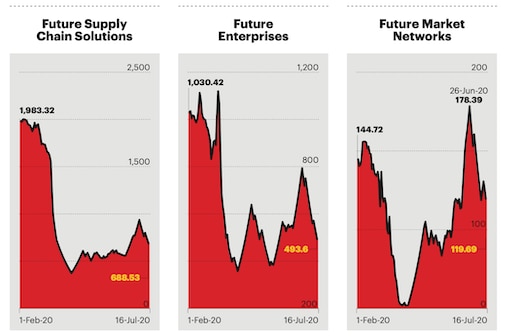

Things weren't so bad till February. Market buzz about his inability to service debt began in mid-February, sending shares of group companies crashing, triggering rating downgrades, even as lenders sought more shares as collateral against loans to Biyani. Between mid-February and first week of April, shares of Future Retail fell by 83 per cent, Future Lifestyle by 75 per cent and Future Enterprise by 65 per cent. The market cap of all group companies crashed around 75 per cent from Rs 33,365 crore on February 1 to Rs 8,354 crore on April 1. This forced Biyani to pledge 80-100 per cent of his stakes in group companies. UBS and IDBI Trusteeship tried to invoke the pledge but Biyani got interim relief from the Bombay High Court. The Supreme Court dismissed the Special Leave Petition filed by UBS AG, London Branch, challenging the high court ruling.

With almost all his equity pledged with lenders, Biyani is desperate to find buyers for his business.

While repeated emails to the company didn't elicit a response, a banker close to the company says when the stock market debacle happened in February, the company had just put together a detailed cost-cutting plan to tide over the crisis. "Kishore had predicted that 2020 would be a tough year globally. He was expecting a recession and was aware that the debt challenge would soon haunt him. Therefore, he decided to shut down any business that was burning cash," says the banker. The company shut 150 non-performing stores, started negotiating for lower rentals and began to slash people costs.

The lockdown hit cash flows badly. With liabilities mounting, Biyani had no option but to exit the business completely. He is in talks with Samara Capital and Premji Invest (which has a 6 per cent stake in Future Retail) to sell his most prized possession, the Rs 20,185 crore Future Retail (which houses Big Bazaar, FBB and small-store formats (EasyDay, Nilgiris and Heritage).

However, the only way Biyani can get rid of the debt is by selling the entire business. The banker says Biyani is hopeful that Reliance Industries will come to his rescue and give him a good value by end-July. If Reliance does this, it will buy Future Group along with its debt, which means Biyani will have to exit. He may also have to sign a non-compete pact disallowing him from starting a new retail venture. "He is prepared for a complete exit. In fact, he has no choice, he desperately needs cash. Only a larger group-level deal will give him the liquidity he needs," says the banker.

A senior retail industry expert, who has known Biyani since the late eighties, says if he has a choice, he will never sell to Mukesh Ambani. "When Reliance decided to enter retail in 2007, Biyani and Ambani had met, and the former had invited Ambani to join his business. He opened up every detail of his business but Reliance entered the retail sector on its own. Biyani shared his business model in good faith."

As Biyani dreamt of building scale, his competitor, Radhakishan Damani, the founder of DMart, preferred doing what he did best - focusing on growing his core grocery retail business. With revenues of Rs 15,000 crore, DMart was the most profitable retail company in India in 2017. "We shouldn't be compared with DMart. They are a low-cost operator, limited SKUs, they do it very well. We are very complex. That's our specialty, as you can't be the same," Biyani had told BT. On the other hand, the big daddy, Reliance Retail, was racing towards the Rs 1,00,000 crore revenue target. Reliance Retail had the backing of cash-rich RIL.

Biyani's FMCG (private labels) brands straddled food, personal care and home care. The idea was to find gaps and offer aspirational products that competition didn't have. He dreamt of challenging global FMCG biggies such as Unilever, P&G and Nestle on his home turf by offering own brands at compelling prices and reducing inventory of other FMCG brands. He thought he would get the required scale if he could have a small format store within a radius of every two kilometres selling essentially his own brands. That's why he went shopping for small-format stores across the country. He bought EasyDay from Bharti in 2015. Later, he acquired Nilgiris and Heritage in the South and partnered with US-based 7-Eleven, owner of a chain of convenience stores that was looking to enter (the launch is stalled) India. He also planned to sell his brands to kirana stores through cash and carry business Aaadhaar Retail.

But Biyani and Future Group were stretched for cash all along (Pantaloons, sold in 2011, was his best performing asset). Nevertheless, he was confident of pulling off his growth story. "We have the cash flow to make growth happen," he had said in an interview with BT in 2017. Three years hence, things have turned out differently.

What Went Wrong?

Biyani's ambitious Retail 3.0 strategy never really took off. While Future Group's revenue is around Rs 35,000 crore, Future Consumer is just a Rs 4,040 crore business (as against the Rs 20,000 crore goal). It suffered a loss of Rs 215 crore in FY20. The group has 990 EasyDay stores; it shut down 150 in Q3FY20. Same store sales growth (SSSG) of Future Retail formats was just 2.1 per cent in Q3FY20. With coronavirus, it's obvious that SSSG will be negative in Q4FY20.

The unanimous verdict of industry stalwarts is that Biyani 'overleveraged' himself. "He is an outstanding entrepreneur, has broken new ground, and many of his experiments broadened the horizons for Indian retail. However, some of them were not very successful," says former Dabur COO Kannan Sitaram (at present, Venture Partner, Fireside Ventures).

A close family friend, Lalit Agarwal, CMD, V-Mart, says he has known Biyani from the days he set up his first Pantaloons store in Kolkata. "He always had a broad view of business and dreamt of capturing a large market. He has been a hands-on entrepreneur but doing many things at the same time became a problem for him. He got into higher capital intensive projects which gave him lesser return on capital."

Biyani himself admitted that in his earlier avatar, he was chasing every possible avenue of growth and so ended up with huge debt. Right from restaurants, beauty salons and gyms to consumer finance, he dabbled in everything, even film production. "Earlier, I was focused on growth and doing new things all the time. Now, I am doing 10 days of rigorous review of businesses in a month. Allocation of capital and resources has become the priority. We will not sign for any new store if we don't see profitability there. It was not the case earlier. Now, return on capital employed is important," he had told BT in the earlier interview.

So, where did he go wrong? Despite focusing only on retail post the 2011/12 debt crisis, industry feels he became over-ambitious in core retailing too. While Big Bazaar and FBB remained his strong points, his bet on the neighbourhood format, for which he acquired EasyDay, Nilgiris and Heritage, backfired. Biyani hoped to attract loyalty towards his smaller format stores by getting consumers hooked on to a loyalty programme. The idea was to get at least 2,000 members per store and charge them an annual membership of Rs 999 which entitled them to 10 per cent discount on every purchase. The model, says a senior analyst, didn't work as Indian consumers were unwilling to pay a fee. "The neighbourhood grocer wasn't asking for a fee and was offering similar services," he says.

"The dynamics of a small store format is quite different and when the company started expanding aggressively, it accumulated huge debt. Consumers didn't find a compelling reason not to shop in a kirana store as opposed to EasyDay," says Abneesh Roy, Executive Vice-President (Research), Edelweiss Securities.

A former Future Group executive, who was closely associated with Biyani's Retail 3.0 vision, says had the market not become sluggish and Covid not happened, Biyani would have managed to pull off the small store format. "We anticipated a shorter gestation for small format stores but it turned out to be a longer gestation business. Had the market been good, it would have done well."

Stock Broker Arun Kejriwal says Biyani's biggest drawback is his inability to manage cash. "Biyani realised he can sell stories to the market. He bought one company, then he bought a second one, and kept buying, raising money and selling dreams to the market. He often duplicates businesses and keeps raising money from the market." Kejriwal refers to Future Supply Chain (which is listed under Future Enterprises and has bulk of the debt, close to Rs 6,500 crore) where, he says, Biyani raised money to offer supply chain and distribution services to other companies. But that was not to be. "The bulk of its business comes from Future Group. They hardly offer their services to others," says Kejriwal. Biyani is desperate to get rid of Future Supply Chain and is known to have asked Ambit Capital to find a buyer.

Retail Debacle

Biyani is often called India's Sam Walton (Founder of Walmart). But for the fact that both championed value retail, there is nothing common between the two. While Walton took 40 years to move from Bentonville to other cities in the US, Biyani has been a firm believer in aggressive growth. "Walton was patient, focused on cutting costs and building logistics and supply chain. For him, retail was not a real estate play. It was a business which needed planning and execution as any business. What Biyani has done defies common sense. He started in Kolkata and went all over India knowing that the country is too complicated for building a good supply chain," says the CEO of a leading consulting company. He finds Radhakishan Damani more like Walton as he has stuck to the basic principles of grocery retailing. DMart (Avenue Supermarts) is today a Rs 24,870 crore company despite the Covid lockdown and the liquidity crisis prior to that. In FY20, it reported 44.15 per cent growth in profits.

Unlike Walton, whose single-minded focus was his hypermarket model, and to an extent Sam's Club (cash and carry), there is no retail format in the world which Biyani has not tried - supermarkets and hypermarkets, small format stores and premium food retail (Foodhall), apparel retail, malls and home products retail. While Walton believed in organic growth, Biyani has grown through acquisitions, most of which were loss-making. The only acquisitions which Walmart has made and that too in recent times have been a handful of online retail companies which it has merged with Walmart.com to take on the likes of Amazon.

"EasyDay was his market concept to take on DMart. At the same time, he also signed with 7-Eleven. There has been no consistency in strategy. It's his attitude of 'I need to do everything in retail' that has led to his doom," says the CEO of a leading lifestyle retail company.

Biyani's small format store strategy (EasyDay, Nilgiris), say experts, has been the major reason for his current situation. He wanted to offer an improved version of a kirana store with loyalty programmes and discounts. These stores attracted consumers initially but were not sustainable despite discounts. Also, real estate and people costs did not make sense. "Those who owned their kirana stores had low costs and loyal customer base and were not impacted," says Roy of Edelweiss.

Biyani set up at the most four-five stores in a city. "You need at least 30 to make an impact," says a senior analyst with a leading brokerage.

A former DMart senior executive says Biyani's cost of doing business is extremely high. He says the rental model is capital intensive and doesn't make sense for value retail. "I don't understand why he didn't convert his good performing stores into the ownership model. Rentals should not be more than 2-3 per cent of your business after the first couple of years but Biyani's rental costs add up to almost 20 per cent of total costs, which is too high."

Failed FMCG Ambition

While experts say Biyani's aggressive retail expansion led to his downfall, FMCG was his big ambition. He wanted to use the multiple retail formats to sell his own private brands.

Almost 35-40 per cent merchandise at Future Group formats was its own brands which, according to experts, didn't go well with consumers. While Tasty Treat pasta, priced Rs 30 less than a Del Monte, did have takers, when it came to soaps, detergents and biscuits, consumers were put off when they didn't find brands such as Britannia, Parle, Surf or Ariel. "Private labels work in certain categories. Future Group thought private labels will give it higher margins and it will win customer loyalty through lower prices. But one can't push private labels beyond a point," says Roy of Edelweiss.

A former Future Group executive says Nilgiris and Heritage lost their loyal customer base after Future Group took over. "They removed popular Nilgiris in-store brands and replaced them with their own." In the past few years, the company has acquired juice brand Sunkist and also got into a partnership with New Zealand dairy major Fonterra for stocking its products.

Biyani's private brands also suffer from lack of trust. The company tried to woo customers through deep discounting, but that hasn't worked. "A consumer may get swayed by the 'buy one get one free' offer one time, but if the quality isn't good, she will not go back. Most global retail brands have private labels and they are successful because quality is supreme. Biyani has not focused much on quality," says the former DMart executive. Private brands account for less than 10 per cent of DMart's inventory. It has always believed in offering consumers the best brands at lowest possible price-points.

Governance Issues

Biyani's desire to pull many horses at one go has proved to be detrimental to his group. However, anyone who has interacted with him will agree that he is among the best minds in the retailing business in the country. "He is always thinking about what next, what changes can I make, what else can I offer to consumers? He says the consumer isn't just the king but also the queen. He is always thinking about how to engage more deeply with the Indian middle class," says Srini Vudaygiri, CEO, Unibic.

A former Future Group employee says Biyani comes up with at least 10 new ideas every day. Often, the dilemma before his team is what to implement and what to ignore. In fact, his vision, more than often, doesn't get translated into action, which leads to governance issues. Industry veterans say Biyani is only a man of ideas and does not follow best business practices.

Transparency is a huge issue, says the CEO of a leading personal care company. "If you are launching a new product with Reliance or DMart, the process is simple. You go to central teams at their headquarters where they list the product. It becomes part of their inventory nationally. In Future, even after getting the product listed centrally, one has to go to each and every store and ensure that it is listed. Most stores also have a huge amount of missing inventory."

"The inventory they show on their books isn't right. I visited a Big Bazaar store in Chennai. The store manager came up to me, told me inventory is missing, and requested me to give a credit note to make up for that," says the CEO of a leading FMCG company.

A common complaint is that the group does not pay vendors on time. One frequently gets to read about leading FMCG companies blacklisting Future stores due to payment delays. A Ranchi-based regional rice and atta manufacturer says he wants to terminate his contract with Big Bazaar as payments take ages. One reason DMart is a favourite among vendors is that it clears dues in days, unlike Future, which takes months.

Biyani is also infamous for delaying payments to landlords even during good times. "He had a good relationship with Phoenix and there was an understanding that Future would get the option of becoming an anchor tenant in any new mall built by Phoenix. Phoenix ended the relationship when it realised that his reputation is going from bad to worse and that having him as an anchor tenant doesn't bring any advantage," says a senior real estate consultant.

Governance issues have tainted the deal with Amazon, too. According to a former senior Amazon executive, it is on the brink of collapse. Amazon picked up a 1.3 per cent stake in Future Retail last year through Future Coupons, in which it bought a 49 per cent stake. "The deal was aimed at building the retail business together. Amazon was to bring in technology and Future supply chain efficiencies and inventory. The stores are to be used as fulfilment centres. The arrangement is facing a host of operational challenges. When the Amazon delivery staff goes to Big Bazaar stores to pick up inventory, they are made to wait at the cash counter as stores prioritise their own customers. The aim was to do over a lakh deliveries a day from Big Bazaar stores but they don't do more than 10,000-15,000," the former executive adds. Though there are reports of Amazon increasing its stake in Future Retail, the US retailer will be happy to exit considering that the investment is not reaping fruits, he adds.

Will Ambani Buy Biyani?

While the market is abuzz with talks of the two signing on the dotted line soon, retail experts believe the deal is too good to be true. The CEO of a leading consulting company says stories around Ambani buying out Biyani must be coming from the latter's company. "Reliance buys things at a scrap rate. They bought Alok Industries at a distress price after it went to the NCLT." Alok Industries, by virtue of being a fully integrated textile company with a dominant presence in cotton and polyester, can be a supplier for Reliances fashion and lifestyle business, he adds. "It has assets in plant and machinery. In retail, there are no assets, and the inventory is perishable. The longer the inventory lies in your stores or warehouses, the more its value diminishes. Real estate is not owned by you, it is leased. If you don't pay rent, the lease is terminated. Your front-end staff does not have unique skills, unlike manufacturing, where you may have highly qualified R&D people. So, when you think about value and valuation, it will be difficult to get Reliance interested, unless it comes at a distress price," he says. "It won't be Biyani who will call the shots but the lenders. If his shares are pledged, lenders will have to see at what price they are being sold. Ambani has no reason to buy Future," says the CEO of a leading FMCG company.

Kejriwal says nobody will buy Biyani's entire business. "It will be piecemeal disposal. Whosoever will buy will have a strong balance sheet. They will say, I will settle your debt and renegotiate terms with lenders and make money on that."

Biyani needs an urgent bailout. One has to wait and watch who will buy him out and how soon, but chances of a comeback appear grim. The only business Biyani is likely to retain is Future Consumer. But then, FMCG is an expensive business and will require huge capital. His friends and associates say Biyani is never without a plan.It remains to be seen if the 'ideas man' has a plan to work around this time.

@ajitashashidhar; nevinjl