By the time this comes out, you will have read all the reactions to Budget 2009-10. Supporters claim that it will spur economic growth; detractors have called it timid, tepid and unimpressive. What’s the truth? Does it really matter to you if fertiliser subsidy is nutrient-based or if the minimum alternative tax has been increased? Ultimately, the government spending does affect all of us.

But there are some proposals that help or hurt individual financial plans, our spending, savings and investment. We take a look at some of these areas and see if they are really going to be in your favour. We consider the impact of the new proposals on personal income tax, fringe benefits tax and the new pension scheme, and also look at how customs duty and excise changes will affect your shopping basket.

Although the annual Budget is supposed to be a road map for government spending over the year—which is why it begins with all the spending on reforms and public allocations—what most of us wait for are the tax proposals. Do we have to pay more as income tax? Are there any new tax breaks? What about salaries?

It seemed like good news when the finance minister announced that the basic exemption limit for individuals had been increased by at least Rs 10,000. Any increase in the exemption limit is good, but this time, it has managed to ruffle many feathers.

Edit writers and opinion creators are already grumbling about tokenism. That’s because, while giving the average taxpayer a tiny break, the Budget has also scrapped the 10% surcharge on tax for those earning over Rs 10 lakh. So, the higher income group gets a substantial benefit, while those earning less have been fobbed off. The rich get another break—the wealth tax exemption has been raised to Rs 30 lakh from Rs 15 lakh.

There have been further accusations of tokenism regarding the increase in deduction under Section 80DD to Rs 1 lakh from Rs 75,000 (for those with a severely disabled dependant). Parents and students will, no doubt, welcome the expansion of the eligibility criteria to include any education after school under Section 80E. However, this section restricts the benefit to interest repayment. It would have made a real difference if the principal had been covered as well.

So, is there any good news? Well, a promise has been made to make filing tax returns easier. The finance minister announced that Saral-2 would be made available soon for public discussion. What does this really mean? The idea is good—to create a simplified tax return form.

But, says professor Kanu Doshi, chartered accountant, managing partner, Kanu Doshi & Associates, and dean, finance, Welingkar Management Institute, Mumbai: “A simplified form can only be a distant dream till the time the law itself is simplified. There cannot be a simple form of return without a simplified tax law. Where the tax law is complex, the form has necessarily to provide for the requirements of such law as, for example, the different heads of income with sub-heads, varying methods of computation with differential tax impact, apart from the many artificial provisions treating what is not income as income and what is admissible as deduction, as disallowance.”

Other experts say that the earlier Saral was shorter—though not necessarily less complex. The ITR forms, which replaced Saral, might be longer, they say, but are simpler. Delhi-based chartered accountant Surya Bhatia says, “It would be good if the new form seeks the same information as the ITRs in a more concise form.” Experts are also wary about the proposal to enforce the UTN (unique transaction number). The UTN will be generated by NSDL each time the tax is deducted from an individual’s income. So, a salaried assessee might end up quoting 12 UTNs in his return. “When TDS deduction can be tracked through PAN, there is no need for another number,” says Vikas Vasal, executive director, tax, KPMG.

The finance minister has also changed the gift tax norms, announcing that from 1 October, the value of gifts given in kind (hitherto untaxed) will be included while computing the gift tax liability.

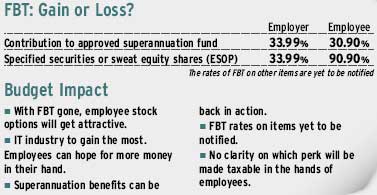

Fringe Benefit Tax

You win some, you lose some. Though the measly increase in the income-tax exemption limit might have left you disappointed, the removal of the fringe benefit tax (FBT) should chase some of the gloom away. What it means, or what we assume it will mean, is that allowances such as conveyance, telephone, fuel, uniform, entertainment, and the like, which had vanished from salary packages, could make a grand comeback.

This is great news, isn’t it? Many experts say that abolishing the FBT is too little, too late. Says Dony Kuriakose, director, Edge Executive Search: “The move will help employers save on taxes after the abolishment of FBT and lead them to offer cash-heavy salary packages.”

What this means is that the FBT can benefit you only if your employer decides to pass it on to you. “The abolition of FBT means savings for organisations and if their HR philosophy is in place, they will be passing it on to the employees,” says Pranav Sayta, partner, Ernst & Young. Effectively, individuals will save where the employers, entirely or partially, pass on the cost to the employee. Conveyance, entertainment and (intra) city travel allowance were being used by employers earlier, when there was no FBT.

Now, we are back to square one. Employers can increase the amount provided under fringe benefits in various forms. Of course, this will be added to one’s salary, taking the taxable salary to a higher level. However, with the surcharge gone and a marginally higher exemption, the effective tax rate will be less than what the employer would have paid while passing on the benefits to the employee. Despite the tax implications of new employee stock option plans (Esops), they could make a comeback as an employee retention strategy.

So, how will the scrapping of FBT help you? It is more than likely that perks can take your salary up by 10-15%, but this largely depends on your employer and your position in the organisation. For instance, an employee earning Rs 50,000 a month and paying Rs 5,000 on fuel can get a reimbursement and save tax of up to Rs 1,500-1,800 a month. Structured smartly, you can claim more reimbursements, which could even mean you can move to a lower tax bracket.

So, how will the scrapping of FBT help you? It is more than likely that perks can take your salary up by 10-15%, but this largely depends on your employer and your position in the organisation. For instance, an employee earning Rs 50,000 a month and paying Rs 5,000 on fuel can get a reimbursement and save tax of up to Rs 1,500-1,800 a month. Structured smartly, you can claim more reimbursements, which could even mean you can move to a lower tax bracket.

The move will see some changes and restructuring of salaries, especially at senior positions. “Though employees can ask for a change in the salary structure, a lot will depend on whether the employer wants to change the structure mid-year,” says Sayta.

Of course, there’s a flip side. Few companies, including technology firms that once pushed hard for higher employee benefits through perquisites, are in the mood to dole out benefits. “With the economy not in the best of phases, the bargaining power no longer rests with the employee,” says Sayta.

However, senior positions, as always, allow for more bargaining power. “The move could actually see some development in startups, where Esops will be back in the reckoning, giving the job market some impetus,” says Kuriakose.

For companies, the removal of FBT is not just the scrapping of a procedural irritant. Small and mid-sized FMCG and real estate players, which took the biggest hit when the FBT was introduced, will now be able to reduce the overall cost of their marketing and promotional activities. This could be passed on to consumers as small price cuts. But for employees, the abolition of FBT only means that the incidence of tax has been shifted to them.

New Pension Scheme

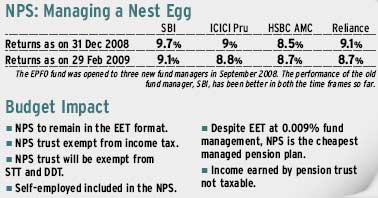

Even the best ideas can fail if they are not backed by action. This seems to be the problem with the New Pension Scheme (NPS). While the finance minister has given some concessions to the pension trust, he has not addressed one glaring anomaly. The objective of accumulating a pension corpus can be achieved through a mutual fund, insurance scheme, and for those who are employed, through the employees pension scheme (EPS). However, the NPS, unlike other pension products, doesn’t follow the EEE model. Instead, it follows the EET model (contributions will be tax-deductible and the accumulated income will be exempt, but any withdrawal will be fully taxable). By not addressing this issue, the finance minister has effectively killed the NPS even before it took off.

There’s some good news, however. The budget did address the issue of allowing deductions on amounts invested in the NPS to a maximum of Rs 1 lakh under Section 80CCD, not over and above the Section 80C limit of Rs 1 lakh. The exemption of income tax for the NPS trust is also a positive, as is the exemption of any dividend paid to this trust from the dividend distribution tax. Similarly, all purchase and sale of equity and derivatives by the NPS trust will be exempt from the securities transaction tax. This makes the accumulation phase of the NPS extremely cost-effective when compared with mutual funds and unit-linked insurance plans.

There’s some good news, however. The budget did address the issue of allowing deductions on amounts invested in the NPS to a maximum of Rs 1 lakh under Section 80CCD, not over and above the Section 80C limit of Rs 1 lakh. The exemption of income tax for the NPS trust is also a positive, as is the exemption of any dividend paid to this trust from the dividend distribution tax. Similarly, all purchase and sale of equity and derivatives by the NPS trust will be exempt from the securities transaction tax. This makes the accumulation phase of the NPS extremely cost-effective when compared with mutual funds and unit-linked insurance plans.

The scheme carries the least cost of management benefit tag when compared to any of the other options available. Says Vinesh Kriplani, partner, global tax advisory services, Ernst & Young: “On a cost basis, this is the best that one can look for in a long-term savings-cum-investment plan.”

The bottom line is that since the scheme is too young to have any other benchmark, it is too early to bet on it purely on the basis of cost. If you are looking at investing in the NPS, ideally, wait and evaluate the way it behaves under fund managers (who will have a low incentive to manage this fund) before joining.

Spending

How much money does this budget give you to spend? Can you increase or improve your consumption basket? The verdict is not yet in, since much depends on whether the companies pass on the benefits to consumers or simply increase their own margins. Some experts are optimistic. “This budget will definitely impact the consumption basket. The surcharge removal, in particular, will leave more disposable cash with people, especially those in higher income brackets,” says Vikas Vasal of KPMG.

Apart from putting a little more cash at your disposal, the budget has also reduced the prices of some goods. In some cases like LCD TVs or branded jewellery, the benefits will be direct, with duty cuts being passed on as lower prices. In other cases, it depends on whether the companies pass on specific benefits. For instance, the abolition of FBT will assist the FMCG sector in reducing the overall cost of marketing and promotional spends, which they may choose to pass on to consumers. At the same time, some other benefits like a lower cost of construction for developers— because of excise duty exemption on prefab structures manufactured at site of construction—may just go on to increase their stretched margins.

So, while your monthly expenses may not go down even marginally, it is still better than the expenses going up, say some experts. “The good news for an average consumer is that even if the budget has not given too many concessions, it has managed to maintain the status quo when it comes to spending. Most changes are basically an extension of the stimulus package that was announced a couple of months ago. Therefore, the impact on spending will, at best, be marginal,” says Rohit Jain, partner (indirect tax), at the law firm, ELP.