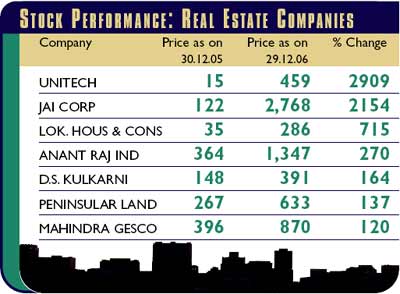

Real estate stocks have been on a tear in the stock markets. In a market that shoots first and asks questions later, the mere mention of some property in a remote place sends the stock soaring. No wonder that the real estate stocks have been chased to the moon last year, making it the best performing sector on the bourses in 2006.

The Sensex in contrast has risen a “measly” 47% this year and the best performing sectoral index is the Capital Goods Index, which has risen 56%. If there was an official real estate index, it would have surely taken the honours of the top performing sector. Unfortunately many of the stocks are too newlylisted for this sort of institutional coverage.

The big question now is how long will the party last?

One thing that is pretty sure is that the high returns that we have seen in the last year are unlikely to be repeated this year, especially for the same set of stocks that have led the rally last year for the sector.

The mad rush for property stocks reminds me of the tech bubble of the 1998-2000 period. Just before the technology bubble finally burst, investors were trying to find information technology (IT) triggers even in old economy companies like Telco and Tisco, where it was speculated that the IT departments of these companies could be merged with then-listed Tata entity Tata Infotech.

The market seems to have come full circle.

Now Infosys is being touted as the best property play! If you take that logic, Tata Steel is an even better play, as it owns the entire town of Jamshedpur. SAIL will take the cake as it presides over six townships across the country. Investors need to be on their guard and not get carried away by such empty arguments.

The rise in property prices can be largely attributed to the everincreasing rise in IT and ITeS infrastructure. A leading foreign real estate advisory firm pegged the contribution of the IT sector to around 85% of the new projects. The much-hyped special economic zones (SEZs) may contribute in the future but currently they are not the driving force.

The demand from ITeS, is still strong as the competition from neighbouring China and eastern Europe is still a couple of years away. But in future, competitive pressure, wage inflation, skill crunch and appreciating rupee may force ITeS to have a re-look at lease rentals or at amortised expenses per future dollar. At that point of time, the real estate sector could feel the heat.

When the first trans-Atlantic flights began in the 1940s it was thought that airline stocks would be evergreen bets. While the numbers of passengers has increased several times over, airlines have seldom made money. Back home in 2000, IT stocks were seen to be evergreen favourites. Six years into the new millennium, today Wipro pays more tax than the net profit it earned in that heyday, but the stock is down 50% from those lofty levels.

The moral of the story is that while the businesses may do well, it is not necessary that the concerned stocks will also do well. Competition ensures that margins become realistic. So the party cannot last forever.

Most of the rapid appreciation we have seen has happened in companies that acquired land banks years ago. So this is a one-time appreciation, which has happened. Further appreciation will be gradual. If a company now acquires new land, it will be at market prices. So where is the question of rapid appreciation?

The biggest flaw in the projection in the real estate companies is the assumption that land prices will appreciate 5% every year. Land prices, even if they have risen through the roof in the recent past, are likely to see alternate cycles of boom and bust.

The SEZ story seems to be headed for a not so pleasant ending. Going by the recent experience, most existing companies are planning to shift to tax havens, where laws of the land don’t apply. This does not gel with the loud thinking of the prime minister that India needs to lessen exemptions on the taxation front. This I feel, would sound the death knell for these early SEZ dreams.

I expect land acquisitions by corporates to become more costly after the Singur incident in West Bengal. The central government may be forced to find an amicable alternative. And that amicable solution will have to be built on the platform of equity; where farmers get a continued share of the appreciation in the land they sell.

One live example of the corporate- farmer partnership is Magarpatta. It is an IT city near Pune, where farmers pooled their land to create a company, borrowed funds from banks to build the most modern integrated IT township in western India. Farmers got shares in the proportion of the land pooled by them. And they will continue to get handsome dividends and phenomenal growth in their wealth as Magarpatta continues its journey to become the IT destination in western India.

One thing that is clearly lacking in the sector is information. There seems to be a large gap between information which is shared with large investors and the common investor, whose only share of information is the price action, call it technical, if you want.

Appreciation however, could happen in such companies, where the land value was not discounted earlier. But here investors will need to establish two things. The first is a realistic estimate of free land that is neither being presently used nor would it be required in the foreseeable future. The second is the willingness of the management to sell or develop such land.

Investors should look at companies that are doing well in their business where surplus land is just a bonus. That way there will be no downside if land prices dip. But for the existing property houses, the best may already have been seen.

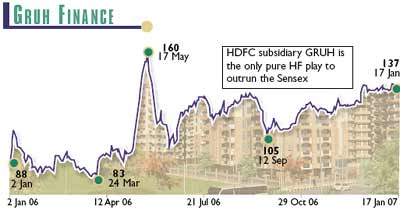

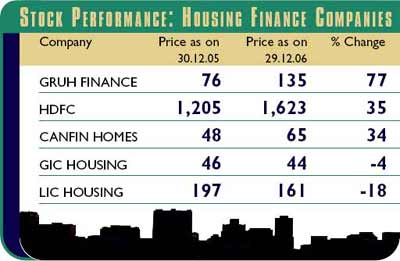

As compared to the real estate companies, housing companies have had a quiet year. Only one company, GRUH Finance has beaten the Sensex. The rest have underperformed the broader market.

Housing companies, however, are not that risky as compared to the real estate ones. The business here is of spreads. As they do not earn any extraordinary profits, these margins are likely to be maintained in tough times and therefore the investor is not going to lose his shirt. He won’t don a three piece suit either.

As around 70% of the disbursals are on a floating interest rates, they get to pass on the cost of increased funds to the consumer. But any further rise on interest rates will hurt as the loss on fixed interest loans will mount.

The best time to enter housing stocks may be when the interest rates start going down hill. As the falling rates will increase the profit on the fixed portfolio.

The higher interest rate regime has also reduced the growth of new housing loans counted in terms of number of accounts. But that has been more than made up by the rising value of the loans. So the housing companies have not felt the heat as much.

The pure-play housing companies do not really capture the growth we have seen in the housing loans. The leader of the pack, on an incremental business is ICICI, which is listed as a bank. Another big gun is SBI, which is also not a pure housing company.

To sum it up, the old property horses look tired. At the most, they could run till the DLF IPO hits the market. And the housing stocks will be good buys when the interest rate cycles turns down.

After the DLF IPO, K.P. Singh may become the fifth-richest man in the world. That will also mean that there is unlikely to be anything left for you on the table.