Relentless competition. Transnational attack. Low profits. Fickle consumers. Unproductive labour. Plummeting share value. Is there any silver lining to the storm-clouds gathered over corporate India? What legacy will I be able to leave for my children? Maybe my business will get wiped out. Will there even be a legacy worth leaving? Maybe all family business, as we know it today, will become as extinct as the dodo.

Despondency, instead of exuberation, is clearly the mood at the close of the 20th Century. Personally, I don't understand why we have lost our selfconfidence. Sure, restructuring is not easy. And yes, almost every company in India has been squeezed in one way or the other ever since the New Economic Policy was ushered in. Yet, if the policy brought pain, it also offered great new opportunities. A yet-to-be published survey of 25 leading business houses has revealed that, contrary to common perception, every single one of them has expanded its range of business activities. Sure, there has been some slimming down-many have sold off the odd unit or two-but, generally, the deals have taken place to raise funds for ambitious diversification projects. Which means that these are not distress sales. If that's not a vote of confidence in the future, I don't know what is. Don't forget that the Rs 8,730-crore Reliance Industries (Reliance) managed to sell its 100-year bonds to the Yankees. There is a story-probably apocryphal-that, at the Reliance road-show, when an investor asked Mukesh Ambani about the future management of his group, Mukesh pointed to a toddler playing unconcernedly at a table in the background. It was little Akash, his son-one of the five children in the next generation.

Given that Reliance's 100-year and 50-year bond issues were both huge successes, the Americans appear to have more confidence in our business families than we do ourselves . Everywhere I go, I'm asked the same question: can the family business survive? The tone behind the question is, inevitably, querulous, and the person asking it has already made up his mind.

In considering this issue, a significant trend seems to have been largely ignored. And that is the buoyant state of company registrations. Even though the past few years have been among the senmost difficult ones in recent economic history, more entrepreneurs than ever before are feeling confident enough to embark upon new ventures.

In 1991, the number of new companies registered in the private sector was 20,745, and, collectively, they had an authorised capital of almost Rs 300,000 crore. Five years later, when some of India's oldest and biggest companies are being forced into some serious belt-tightening, hundreds of inconspicuous and uncelebrated businessmen are coming forward with fresh ideas and raw ebullience. In 1996, there were 47,598 new companies-more than double the 1991 figure. The total authorised capital of these new enterprises crossed Rs 800,000 crore.

Moreover, a large and growing number of new family groups have appeared on the corporate landscape in the 1990s. Many of these are jostling with the old guard for a leadership position. Fresh blood such as the Nambiars (BPL), the Guptas (Lloyds Steel), the Jindals (Jindal Strips), the Oswals (OWM and Vardhman), the Singhs (Ranbaxy), the Shahras (Ruchi Soya), the Mehtas (Torrent), the Lohias (Indo Rama), the Dhoots (Videocon), and the Premjis (Wipro) have elbowed out former stalwarts such as the Dalmias, the Modis, and the Walchands. Most of these new groups grew steadily in the 1980s but came into prominence in the 1990s.

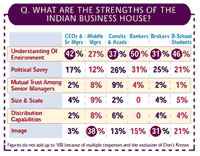

The robustness of the new groups, combined with the unmistakable vitality in at least a dozen of the older established ones, is proof enough that family business in India is not just alive, but kicking. Their main strength lies in understanding the environment that they operate in. This is borne out by a BT-Gallup MBA study which polled a sample of 363 respondents, comprising consultants and academicians (54), CEOs and senior managers (48), middle managers (77), B-School students (110), brokers (48), and executives in banks and financial institutions (FIs, 26), in Ahmedabad, Bangalore, Calcutta, Chennai, Delhi, and Mumbai. According to the study, the two biggest strengths of Indian business families are their understanding of the indian environment, and image. The CEOs and senior managers perceived the first factor as the biggest plus, followed by political savvy. On the other hand, 38 per cent of the middle managers plumped for image followed by an understanding of the environment.

Chest-thumping might be premature, though, and complacency costly. The BT-Gallup MBA poll not only highlights the hot spots, but also indicates the challenges ahead. For, among the five threats to Indian business-splits, succession-planning, takeovers, transnational competition, and lack of focus-transnationals pose the biggest danger followed by splits in the family. Almost half the CEOs and brokers polled believed so. But most businessmen- or at least the astute, savvy ones-have sussed out what needs to be done to stay on top in the next millennium. There is consensus that Indian business needs to reduce costs, improve quality, and, generally, become globally competitive within Indian borders. For patriarchs heading family businesses, this translates into three major dilemmas:

How to find, and hire, the best managers a group can afford.

How to ensure that the next generation is able and capable of taking over the baton.

How to encourage each business unit within the group to become focused, and to maximise its core competencies to best advantage

It is unlikely that even the most hardened oldtimers will quibble with the prescription. Each of the three ideas listed above is not only eminently sensible but simple common sense too. But to implement them will be difficult judging by the results of the poll. And this is where the problem lies.

PROFESSIONALISATION. The first issue is finding, and hiring, good managers. In order to survive the transnational attack and the gale of new competition both from local and foreign players, it is obvious that family groups must improve their working. This can be best done by introducing good systems, and getting better managers, be it in manufacturing, finance, marketing, or everything in between.

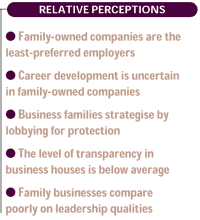

But the poll clearly indicates that managers- good or otherwise-don't want to work for family businesses. Of the 48 CEOs and senior managers polled, a mere 6 per cent said that they would like to manage a family-owned company. On the other hand, a vast 60 per cent said that they'd rather run an ''independent'' Indian company. Of the 110 BSchool students polled, a minuscule 1 per cent said that they would be willing to work in a family firm. The majority, 77 per cent, said they'd prefer to be employed by a transnational.

The heavier pay-packages offered by transnationals might be a factor in these responses-there is no argument that family groups are stingier than transnationals- but it can't be the whole story. When such a huge reluctance to work for family firms manifests itself, there must be other, more subtle causes. From the patriarchs' point of view, the poll is an earshattering shriek which needs to be heard-and heeded. It might be wise to think of ways in which to reposition themselves, create another image, make their organisations more attractive not only to seniorand middle-level managers but also to freshlyminted MBAs. And given that the supply of good managers is rather small compared to the demand, the swifter this issue is addressed the better.

As for the 109 MBA students who said they'd rather not work for family firms, it might be worth noting that of the top 100 companies in the private sector, 67 are family-run, and 24 are transnational affiliates. That translates into some stiff competition for perches in the remaining nine companies. It is worth asking whether there might be more job satisfaction in being selected a member of Reliance's A-Team than not. Perhaps yes. For, the poll reveals the Ambanis to be the most competitive business family in India, followed by the Tatas and the Birlas, who rank second and third, respectively. Confidence in the Ambanis was particularly strong in some categories: 73 per cent of the brokers, 65 per cent of the executives from banks and FIs, and 52 per cent of the CEOs and senior managers put their chips on that business family.

SUCCESSION PLANNING. The second dilemma faced by patriarchs is the thorny preparing-for-succession issue-the third-biggest threat, according to the poll. How does one groom inheritors and arm them for the new marketplace where the rules are constantly changing? Earlier skills are no longer valid. In the past, high octane achievers had to manage the government, form cartels, and make friends with bankers who would lend money unquestioningly.

The licence-permit raj meant that once you had the all-important pieces of paper in place, you could sit back and sell in a market of shortages. Most companies didn't 'market.' They 'allocated.' The events of the 1990s have shattered that cosy world for ever. The jean generation needs different skills. They still need to have the patience to deal with politicians and bureaucrats; but they also have to listen to cranky consumers, uptight quality control managers, and volatile trade union leaders. To top it all, they need to have the charisma to raise money in the capital markets and debating skills to field, or deflect, questions from pesky journalists.

Traditionally, men like Ghanshyam Das Birla learnt their business skills at their father's knee, or sitting with the group's chief accountant. In the 1970s, a few forward-thinking patriarchs began sending their boys to B-Schools in the US. Thus, Aditya Birla and Rahul Bajaj studied at Harvard and the Massachusetts Institute of Technology. This move not only earned the young scions respect from their executives, but it also began a process of muchneeded professionalisation. Today, the strategy is being extended to another level. For instance, Rajiv, Rahul Bajaj's son, worked on the TELCO shopfloor for a year, gathering work experience before joining Bajaj Auto. Kumar Mangalam, the late Aditya Birla's son, boasts of an MBA from the London Business School and is also a qualified chartered accountant.

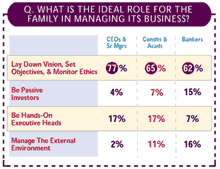

Executive approval of inheritors is vital. In successful companies, the family provides leadership and the professional managers take day-to-day operational decisions. As the poll indicates, 77 per cent of the CEOs and senior managers expect family members to lay down the vision, set objectives, and monitor ethics. So do consultants and academicians (65 per cent) and executives from banks and FIs (62 per cent). This suggests that the family should be something in between passive investors and the hands-on executive heads.

In a sense, this attitude is history repeating itself. In the 1870s, when the industrial revolution first touched India, speculators built cotton textile mills and traders wove gunny bags. The emerging capitalist class didn't know a thing about machinery; they didn't know one end of a screwdriver from another. But they took the attitude that money can buy just about everything. So, Kasturbhai Lalbhai, the founder of the Lalbhai Group, placed an advertisement in the Manchester Guardian asking for skilled managers for a new textile mill in Ahmedabad.

Walchand Hirachand, the founder of the Premier Group, poached marine engineers from the rival British India Steamship Corp. to build Scindia. J.R.D. Tata imported an American chemist to help him sort out Tata Chemicals' problems. This hands-off attitude changed in the 1960s and the 1970s. Increasingly, top management-the family-were expected to know a lot about their factories. It became a point of honour, for instance, for a Mafatlal to walk around the weaving shed intelligently and knowledgeably, discussing counts with the master. Rahul Bajaj went to the extent of living in the factory complex. But, today, nobody expects a Mukesh Ambani to outdo or outknow his engineers. In an era of super-specialisation, it is more important that the jean generation knows how to assemble the pieces of the corporate jigsaw into the big picture and make it all happen.

To bring together experts and weld them into a motivated team. But even after every lesson has been taught, it's still touch and go. Building empires is not about making money. Some people are empire-builders, others aren't. Entrepreneurship is a gut feeling that can't be handed down. There's no textbook answer about how to teach your kids courage.

Strategic focus. Another aspect of concern is the entire gamut of issues around the need to focus. So, should groups diversify? Or should they slim down? How does one identify one's core competencies? By its very nature, family divorces can provide the solution. However, not everyone thinks so. Most of those polled felt that splits were the second biggest threat to family businesses after competition from transnationals. There seems to be across-the-board unanimity among consultants and bankers, brokers, and B-School students that splits are a greater threat than wars of succession or takeover threats.

However, splits are not only good for business families but also vital for the health of corporate India. Splits goad growth. Data indicates that groups that have split outperform those that have not. RPG Enterprises is an example of this. When the three Goenka brothers separated in 1979, the sales of each truncated group were Rs 70 crore. From this modest beginning, Rama Prasad Goenka constructed a Rs 6,000-crore group; Gouri Prasad Goenka, the youngest brother, assembled the Rs 2,401.44-crore Duncans Group. The middle did not do as well, but the sum of the parts is definitely more than what it might have been had the brothers stayed together. As R.P. Goenka said some time after the divorce: ''When we were together, the desire for business was not greater. But I was more careful. I think there is more adventurism in me now.''

In stark contrast to the successful Goenka model is the example of groups such as the Modis, who have not been able to swiftly cut the Gordian family ties. In the 1980s, the Modis were one of the fastest growing business families in India, with several bluechips in their stable. In the 1990s, there's not a single Modi-run company in the top 100. And, in several cases, either government nominees or their transnational partners have wrestled management control of these companies, reducing the members of the family to the role of virtual investors, albeit large ones.

For patriarchs paranoid about keeping the family together, there is a way out. Focus can be achieved by farming out businesses between progeny. Earlier, to maintain a balance between their sons, fathers would depute one son to look after group finance, another to monitor production, a third to develop sales and marketing, and so on. In the present scenario, this strategy can, perhaps, be redefined so that the group is carved up into focused individual units, each looked after by an inheritor.

The three dilemmas outlined above are, perhaps, the largest ones in the basket of the business family's problems. Will India's big business families do better in the future than they have done in the last 50 years? My hunch-and I earnestly hope that I am wrong-is that we should be happy if there are even half the number of Indian business families in the Top 50 in the next millennium as there were in 1939. The poll results show that I'm not alone. Asked how many of the top 50 business houses will survive over the next 25 years, most guessed that between six and 15 groups would survive.

At the top- and the bottom-end of the range, the poll revealed an unexpected optimism. More people felt that all 50 would survive than those who considered that none would exist in their present form. Among the CEOs and senior managers, 13 per cent felt that all the 50 groups would survive while 31 per cent felt that between six and 15 groups would survive. A overwhelming 42 per cent of the middle managers, meanwhile, believed that between 16 and 30 business families would survive.

The BT Survival Signal of India's top 50 business houses seems to support my hunch. None of India's Business Houses merited a rating of Powerful. Having earned either a Strong or a Medium, 30 groups are expected to survive, but half of today's elite could go down the tube. A rough back-of-the-envelope analysis of all business groups-not just Indian family ones-paints an even grimmer picture.

There is, however, some good news. To understand the future, the pyramid offers a possible analogy. India's biggest business families are being pushed down from the pyramid's apex. But, at the same time, its base is stretching ever wider as the number of family firms is increasing rather than decreasing, in tandem with the country's economy. In the future, the US and Japanese transnationals will, undoubtedly, dominate the tip of the pyramid, but the action at the bottom should be feisty, leading to a lively creation of wealth for the country.

Not surprisingly, even the most pessimistic of respondents (senior managers and CEOs) awarded a heart-warming 4.10 points (Max: 5) for the contribution of the family business to the economic growth of the nation. Another facet of the poll disclosed the overwhelming belief that the Ambanis are India's best-managed business house. Other honourable mentions include the Lalbhais, the Ruias, the Premjis, and the Bajajs. Certainly, the end is far from near. Long live the family firm!