It was unheard of. Annual fund management and custodian fees as low as 0.0009% of the investment seemed too good to be true. This is what the recently launched New Pension Scheme (NPS) offers—a paltry cost of Rs 9 for every Rs 1 lakh that is invested. However, enrolment in the NPS has been much less than expected, with only around 2,500 individuals estimated to have signed up by August this year. Why isn't everyone rushing to invest in the next best thing to social security in India?

This is because most investors are savvy and realise that not every low-cost option makes for a good investment. Which is not to say that there is a catch to the lowcost tag. It is, in fact, one of the biggest lures of the NPS. Consider the comparative advantage of the low fees. Against Rs 9 in the NPS, you will shell out about Rs 1,500 a year for every Rs 1 lakh invested in a mutual fund despite the waiver of entry loads and about the same for a standard Ulip (after the first three years of much steeper charges).

Remember, these are recurring costs. So if you invest Rs 1,000 a month each in a mutual fund and the NPS, and assuming that both give the same returns, in 30 years, the NPS will grow to Rs 79 lakh, while the mutual fund corpus will work out to Rs 55 lakh. That's advantage NPS by a huge Rs 24 lakh because of the lower annual fee alone.

This brings us back to the original question: why have so few people signed up? The problems with the product begin with the fact that the Pension Fund Regulatory and Development Authority (PFRDA) bill is yet to be passed by Parliament. What this means is that the regulatory body has no teeth so far. It is also seen by many as a sign of the government's ambivalence about implementing the NPS.

The biggest drawback is that given the manic focus on keeping the fund management charges low, there is little incentive for fund managers and intermediaries to do their job well. In addition to the fund performance, this will also affect its promotion.

Says U.K. Sinha, chairman and MD, UTI Asset Management Company: "Maybe the government imagined that the fund managers won't have any role in actively promoting the scheme. Otherwise they would not have floated the tender and worked in this manner." In its current form, the regulator and the government will have to take the initiative to market the NPS as there are no takers among fund managers and intermediaries at the points of purchase (PoP) to sell it.

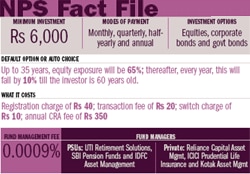

Though the NPS is projected as a cheap product, there is a bias towards investors who contribute higher amounts. The reason is the fixed transaction charge of Rs 520 and the PoP charge of Rs 280. These charges remain the same, irrespective of the invested amount. So, if you contribute Rs 6,000 annually to the NPS, these charges work out to 13.3% of the investment. If you contribute Rs 12,000 a year, the cost is halved to 6.67%, and so on.

It is not costs alone that mitigate the effect of high returns; taxes can be ruthless killers too. It is assumed that the NPS will be taxed according to the EET (exempt, exempt, tax) pattern—the contributions will be tax-exempt within the Rs 1 lakh limit of Section 80C and the accrued income will be exempt when it is earned. The withdrawals will be taxed according to the applicable slab.

Going back to the example of Rs 1,000 invested every month in the NPS, this will shrink the returns to about Rs 52 lakh if the income is taxed in the highest bracket. Compare this with the taxfree income of the Public Provident Fund (PPF) or the Employees' Provident Fund (EPF), and the NPS loses sheen.

Also, the NPS is no longer required to pay the Securities Transaction Tax on its purchase of shares. This will improve returns as 0.25% will be added to the yield on the equity component of the scheme. Similarly, any dividend paid by the fund will not be subject to the dividend distribution tax.

From the investor's viewpoint, the NPS balance sheet has more drawbacks than incentives, though any analysis of the scheme is pure conjecture at this point. For now, the lack of incentives looks like it might take a toll on its performance. If the NPS is made more attractive to fund managers, they are likely to manage the scheme actively, thus ensuring better returns. This will automatically bring in more investors. The demographic trends in India show that senior citizens will triple by 2050. In the absence of any form of social security, they will have to rely on their savings to fund their retirement. An attractive, cheap pension scheme that also offers decent returns is just what is needed. Will the government make it happen?

_Small.jpg)