It’s a question that perplexes even the most astute investor: how does one pick a good stock?

We all know that investing in equities is the best way to create wealth. But picking the right stock is fraught with difficulties. You need to be able to separate genuinely solid companies from those that just make a lot of noise, time the market, and do this before everyone realises that the stock is a winner.

Or take the easy way out. Look at what the experts are buying, mimic their portfolios, and chances are you’ll make a neat packet.

| FAVOURITES, OLD AND NEW | ||||

|---|---|---|---|---|

| Rank in 2007 | Rank in 2006 | Company | Fund holding* (Rs cr) | Fund count** |

| 1 | 2 | Reliance Industries | 8,930.10 | 227 |

| 2 | 15 | Larsen & Toubro | 5,424.24 | 179 |

| 3 | 23 | ICICI Bank | 5,052.89 | 177 |

| 4 | 8 | Bharti Airtel | 4,495.55 | 189 |

| 5 | 10 | Reliance Communications | 4,471.96 | 185 |

| 6 | 4 | State Bank of India | 4,422.14 | 186 |

| 7 | 6 | Bhel | 4,300.23 | 174 |

| 8 | 9 | ONGC | 3,093.25 | 129 |

| 9 | 3 | Grasim Industries | 3,059.19 | 148 |

| 10 | 11 | Siemens | 2,816.68 | 110 |

| * Value of equity held by mutual funds; ** Number of funds holding the stock | ||||

That’s why we decided to make the MONEY TODAY-Value Research ranking of India’s Most Wanted Stocks an annual event. From a universe of over 6,000 stocks, we culled out 45 that are favourites of fund managers.

These rankings can be useful to mutual fund investors as well as direct investors in equity. The former can rest assured that fund managers are doing their best to generate healthy returns. And active equity investors can take a leaf out of the fund managers’ book and create similar portfolios.

We take you through the hottest sectors, as well as the most popular large-, mid- and smallcap stocks. And finally, a word of caution: the most wanted stocks are not always the most rewarding, so don’t rush in with your eyes shut. Remember that it is, after all, your money and your investment.

Movers get shaken

When you look at fund managers' choices to improve your investment returns, you are actually using fund picks as a filter to decide which stocks to examine in detail. After all, you cannot invest in all the stocks a fund puts its money in. The large cap component of mutual fund portfolios is often the least revealing. It changes the least over time and most stocks are common to diversified equity fund portfolios.

| CLICK HERE TO VIEW THE TOP 25 LARGE CAP STOCKS |

But over the past year, there have been some major changes and this year’s rankings threw up a number of surprises. For one, 10 out of the top 25 stocks are new entrants. And then there’s the huge churn in rankings, where we find that no stock has retained its previous ranking. Not even the top five. Reliance Industries (RIL), last year’s second, takes top spot this year. Infosys, last year’s topper, has slipped to 12th place. And last year’s laggard, ICICI Bank, has zoomed to the third place.

Yes, this says a lot about the state of the markets and the economy as a whole, but it has truly farreaching implications for you, the investor. It says very clearly that if you want a piece of the most wanted companies, you cannot afford to follow a buy-and-hold strategy. You will have to be an active investor.

| NEW BEAUTY CONTEST | |||

|---|---|---|---|

| STOCK | FIRST HOLDING | SECOND HOLDING | THIRD HOLDING |

| Reliance Ind | 92 | 17 | 18 |

| Larsen & Toubro | 16 | 23 | 19 |

| ICICI Bank | 13 | 20 | 11 |

| Bharti Airtel | 5 | 4 | 17 |

| Reliance Comm | 6 | 15 | 17 |

| Figures are number of funds having these stocks as their first, second or third highest holdings | |||

Most fund managers invest the bulk of the fund corpus in large caps belonging to the benchmark indices, because they can neither wait years for the stock to begin performing, nor can they take undue risks. This is a safety-first strategy in two ways. The portfolios resemble the indices. So, performance will be reasonably similar to the benchmark.

Even if the portfolio doesn't do well, the manager has little to explain. After all, he has bought large companies that are household names. It’s no wonder, then, that 90% of any diversified equity fund holdings is in large-cap stocks.

Yet, like our last year’s ranking of most wanted stocks, this year’s list too has several lessons for stock and mutual fund investors. For instance, the quality of fund management — or a stock pick — depends not just on the quality of holding but also on the timing of acquring that holding. Two mutual funds that hold exactly the same portfolios can yield different returns. It depends on when the fund managers bought each stock and at what price.

Our shows that 227 funds own RIL, compared to 180 last year. Fund ownership of RIL has increased “only” 17 lakh shares to 3.20 crore shares in October 2007. In October 2006, the funds owned 3.02 crore shares. In that year, RIL’s price soared from Rs 1,226 to Rs 2,782. The October 2006 owners have obviously gained. How many of the 47 funds, which bought RIL in the past 12 months, have made profits on the RIL holdings?

This depends on whether they bought at Rs 1,176 (the lowest price during November 2006–October 2007) or at Rs 2,989 (the highest price) or somewhere in-between. You can look at month-to-month portfolio disclosures of specific funds to see if they bought the stock when it offered the best value or at the top of the market.

Another way to judge institutional attitude is to see how many shares are held now against how many were held a year ago. But this can be misleading. The number of shares held can increase due to a rising equity base. For example, ICICI Bank saw shareholding rise from 89.2 crore shares (Sep 2006) to 111.19 crore shares (Sep 2007), increasing its free-float. But factor in the follow-on offer that the bank came up with in June 2007 throwing open opportunity for funds to buy in it. Comparing fund-counts can also prove useful. Rising counts indicate increasing institutional consensus and vice versa.

Apart from the new entrants, old-timers such as RIL, ICICI Bank, Reliance Communications, Bharti Airtel, State Bank of India and Larsen & Toubro are some examples of businesses that have seen expanding exposures. That means institutional consensus has grown in the past year on these stocks. On the downside, Hindustan Unilever (HUL), ITC, ACC, and the erstwhile institutional favourite Infosys have all seen a large drop in fund counts. For the first time in its history, HUL has ceased to be a Top 25 holding— as many as 50 funds have let it go.

Some 48 funds have disinvested ITC, while Infosys has seen 39 funds exiting in the wake of a stronger rupee, which has removed some of the software sector’s sheen. The newcomers on the list include Axis Bank, HDFC, IDFC, Jindal Steel & Power, NTPC, Reliance Energy (REL), Sterlite Industries, Suzlon Energy, Tata Power and Tata Steel. That's a whole clutch of financial and power sector stocks entering the fray. These are obviously concentrated bets on two specific sectors. The stocks that exited the Top 25 were more diverse. These included ACC, Hindustan Petroleum, Punjab National Bank, Mahindra & Mahindra, Zee Telefilms (now Zee Entertainment), Hindustan Unilever, Hindalco, Tata Motors, Satyam Computer Services, and Crompton Greaves.

While you could argue that public sector banks were replaced by more dynamic players, there was clearly a bias against software and automobiles. The IT sector was hit by the strong rupee while automakers were hit by rising costs and slower demand due to high interest rates.

Another point that investors may find interesting is the “beauty contest” format we created when we started tracking large caps. Many funds may hold the same stock but how many keep it as their largest holding or within the top three holdings? That gives an indication of fund managers’ levels of confidence in a stock. The 2007 winner is RIL, which stands first in an amazing 92 portfolios. Larsen and Toubro follows, finding a place in 16 portfolios.

Our take: If you play copycat and pick some of these stocks as the core holding of your portfolio, you cannot go wrong. Your returns may not be as exceptional as the managers who found these stocks early. But, unlike a fund manager, you have no compulsion to generate quarterly returns, so you can buy and hold from within this universe for safe returns.

Last year, we had said that “many of today’s leading stocks were also leaders yesterday and will be tomorrow”. That continues to be true, especially when we talk of large-cap stocks, which form the core of every diversified equity fund portfolio. So should they be of a retail investor. Large funds are benchmarked to the performance of major stock indices like the Sensex or Nifty. The Sensex holds about 41% of total market capitalisation while the Nifty has about 62% of total market capitalisation. The long-term reputation of a fund depends on how consistently it beats the benchmark.

How we did it

To find out which were the stocks most wanted by mutual funds, Value Research examined the portfolios of all open-ended equity funds and equity-oriented balanced funds.

As on 31 October 2007, there were 496 open-ended equity-oriented schemes that collectively invested Rs 1,66,233 crore in over 5,000 listed companies. The portfolios of all the 496 schemes were aggregated and then sorted on the basis of the value of holdings of individual stocks to arrive at the 25 most wanted stocks.

The holdings have been further slotted into mid- and small-cap companies to get a sense of the emerging companies that could become tomorrow’s large caps.

Mutual fund tracker and our partner in the study, Value Research has a dynamic classification, where stocks that account for 70% of the total market capitalisation are categorised as large-cap stocks. The next 20% are classified as mid caps and the remaining 10% are classified as small caps.

The sectoral distribution of mutual fund investments is a good barometer of what’s hot and what’s not. It gives a larger picture of which sectors are most in demand and what fund managers expect in the coming months. We slotted all the stocks across the 496 schemes into 14 sectors on the basis of the businesses they were in to figure which were the most preferred sectors and which ones fell from grace.

Closed-ended funds, exchange-traded funds and unit-linked insurance plans, or Ulips, have been kept out of the rankings.

All mutual fund data is sourced from Value Research; all financial details were sourced from Capitaline.

GLOSSARY

Dividend yield: This is the effective dividend paid out by a company. Companies declare dividends on the face value of the stock. Dividend yield is calculated on the market value of stock.

Return on net worth: This ratio of net profit to net worth measures efficiency of capital use.

EPS: Total earnings divided by number of shares outstanding, showing how much each has earned. EPS calculations have been normalised to make them comparable across companies and sectors

Blue chips in the making?

As a class, mid-cap stocks are most fluid. An under-performing large cap could become a mid cap, while a highgrowth mid cap could easily graduate and become a large cap. That’s what has happened this year, with Crompton Greaves falling from the large cap list to heading the list of Top Mid Caps.

Mid caps truly reflect the growth of the economy. They cannot be your core holding but you can't live without them either. There is one danger in mimicking the mid cap portfolios of funds. Most fund managers buy large caps with a very long-term perspective. They buy mid caps based on more shortterm considerations, hoping to add a little zing to their core portfolios.

Therefore, they are more likely to disinvest rapidly. Balanced against that, there is a very good chance that you might find a multi-bagger that turns into a large cap. This year, six of the Top 10 mid -cap holdings are new entrants.

| CLICK HERE TO VIEW THE TOP 10 MID CAP STOCKS |

Two of the 2007 newcomers are actually “demotions” from the 2006 large cap segment. Crompton Greaves and Zee Entertainment were demoted for different reasons. Zee Telefilms saw a complicated restructuring that created four new companies, of which Zee Entertainment is one. Crompton Greaves was a large cap overtaken by other stocks including new listings that shoved it out of that list.

Among the newcomers, Divis Laboratories is a red-hot stock in a hot sector: contract pharmaceutical research leverages India's workforce of cheap, skilled, scientific talent. Bharat Electronics is a PSU that could gain massively from the opening up of the defence sector and it’s also expected to sell a lot of electronic voting machines over the next two years. Century Textiles is a real estate bet—it has prime real estate holdings in metros such as Mumbai. Punj Lloyd is an engineering and construction firm that is expected to grow consistently through the next five years.

Mid caps can grow quicker than large caps during booms and they can suffer more than large caps during a bust. However, their swings are less extreme than small caps and they can absorb large investment holdings. A fund manager who is looking to beat the benchmark will usually look for big winners within this space and over 25% of fund holdings are in mid caps.

Given the wide coverage of these stocks in the derivatives segment, most mid caps have excellent liquidity. There’s little fear about fund managers being stuck with a large mid-cap position since these stocks often generate huge daily volumes. (They can also be hedged against excessive price volatility, although funds generally don’t do this.) Exposure to this segment also means diversification, not only in the generally accepted sense of holdings across different industrial sectors, but also in terms of size.

The theory behind diversification is that different sectors will perform differently during various phases of the economic cycle. It’s a fact that mid-cap stocks don’t perform the same way as large caps even if they are within the same sector.

In the past one year, the BSE Mid-Cap Index, which comprises 276 companies, earned 56% against the Sensex returns of 41.9%. Fund holdings in mid cap companies have risen 140% in the past one year to touch Rs 13,887.4 crore. Fund managers have a huge choice in terms of what they choose to buy in the midcap space. This is where their superior stock picking skills can generate the largest returns.

Fortune makers, or breakers

Easy credit and a rising stock market have resulted in an increased appetite for small-cap stocks. The setting up of the BSE Small Cap Index in April 2005 demonstrates the confidence the market has in this segment. But it’s also a known fact that small caps are notoriously volatile. This year’s list proves that; eight out of the Top 10 are new entrants, including the topper, Bharati Shipyard.

| CLICK HERE TO VIEW THE TOP 10 SMALL CAP STOCKS |

If you can live with volatility, you can find some of the market’s highest returns in these stocks. In the past one year, the BSE Small Cap Index returned 68.6% when the Sensex reported 41.9% returns.

During growth phases, small caps can register triple- or even fourdigit compounded annual growth rate (CAGR) for years because of the low initial base. They traditionally outperform in a rising market. Over the past year, there has been a 100% increase in mutual fund holdings in small cap stocks— from Rs 1,709.1 crore last year, to Rs 3,406.7 crore this year. An interesting and instructive point to note for retail investors keen on small caps is that a single large buyer can push prices up by a massive amount.

But thanks to the extreme volatility, only contrarians and fund managers seeking value will consider investing a percentage of their corpus in these high-risk scrips. That is exactly what the strategy of small investors interested in these stocks should be.

Spotting the gems is an art and, in recent times, there’s been a rapid emergence of funds with a focus on these stocks. It’s a fantastic asset class in terms of potential returns, but if you want safety, avoid small caps altogether.

The churn in this category is always high and 2007 was no exception. The list of Top Small Caps has seen more changes than the list of top mid-cap and largecap stocks. Just two of last year’s Top 10, pharma stalwarts Dishman Pharma and Ipca Laboratories, stay on. Dishman, which had the highest market cap last year, is the darling of fund houses with 42 funds owning significant holdings against 21 last year.

Among the newcomers is Apollo Tyres, which has been hit by a dispute in the promoter-family and hence “demoted”. Bharati Shipyard is a new business with excellent growth prospects although it services a cyclical industry. Emco, manufacturer of electrical equipment, could benefit from power sector reforms.

Turnkey electrical engineering outfit Jyoti Structures is a good bet, though it is probably best remembered as a Harshad Mehta favourite. Simplex Infrastructure is a construction company that could grow its turnover by 50% over the next several years. Although NDTV has not seen profits yet, the price of the media scrip has gone up. All these sound good in theory. In practice, you need a gambler’s instinct to enter this segment.

The collective market capitalisation of the 5,500 smallest companies registered on Indian stock exchanges accounts for just 10% of the total market capitalisation. Institutional investors track very few of these stocks and price movements are not highly correlated to movements in the larger indices. The stocks can turn illiquid in a bear market.

Further, small equity bases cannot absorb large investments, they are more vulnerable to cyclical swings, corporate governance is often poor, and it is difficult to gather information about small companies on a regular basis. But there’s some comfort in knowing that there is some institutional consensus and coverage of at least the companies mentioned in our Top 10 list.

Where it all starts

Most wanted sectors often produce the most rewarding stocks—and vice versa. The recent experience with technology stocks bears this out.

Because of concerns spanning the sector, technology stocks have fallen out of favour with fund managers this year. The sector has slipped two places on our latest list of Most Wanted Sectors, and the top spot has been claimed by energy.

| Rank in 2007 | Rank in 2006 | Sector | % of fund investment* |

|---|---|---|---|

| 1 | 3 | Energy | 13.65 |

| 2 | 6 | Financial services | 13.51 |

| 3 | 1 | Technology | 12.43 |

| 4 | 2 | Basic/Engineering | 12.20 |

| 5 | 4 | Diversified | 9.29 |

| 6 | 10 | Metals & metal products | 7.97 |

| 7 | 7 | Construction | 6.87 |

| 8 | 9 | Services | 6.21 |

| 9 | 5 | Automobile | 4.43 |

| 10 | 8 | Consumer non-durables | 3.70 |

| 11 | 11 | Health care | 3.59 |

| 12 | 12 | Chemicals | 3.04 |

| 13 | 13 | Others | 2.14 |

| 14 | 14 | Textiles | 0.72 |

| 15 | 15 | Consumer durables | 0.25 |

| * % of total equity fund corpus (Rs 1,67,667 cr) invested in each sector | |||

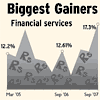

The automobile, chemicals and textile sectors seem to be going out of favour, with absolute allocations dipping. Conversely, allocations to the financial services, metals and metal products sectors have gone up. What does all this movement mean? During a macro-economic boom, growth is evenly spread and the majority of industry sectors move up. But the growth is always uneven and certain sectors always outrun others. In addition, a few “counter-cyclical” sectors have a difficult time when the rest of the economy is booming.

In our study of 14 sectors, the assets under management of the funds we surveyed went up by 50% from the quarter ending September 2006 to that of September 2007. There’s also been some amount of churn, with certain sectors losing their sheen and others gaining favour. A lot of this could be due to the many infrastructure projects that have been commissioned and the many initial public offerings (IPOs)—especially in the financial services sector—which offered opportunities for funds to take sector positions.

The automobile sector had fewer takers, largely due to slow demand combined with higher raw material prices. At the same time, the financial services sector has been boosted in light of strong credit growth. Also, banks have launched a series of follow-on public offers (FPOs) to raise their equity bases to meet Basel II norms. The broking industry has come up with IPOs and the new listings have registered strong growth.

Over the past three years, growth has been spread more or less evenly across 14 broad sector categories. That has been reflected in the aggregate sector allocations of diversified equity funds. However, the broad focus appears to be narrowing. The top five sectors attracted 61% of assets under management (AUM) in October 2007 compared with 52% in 2006. The bottom five sectors attracted only 9.7% of AUM in 2007 compared with 12.8% in 2006.

|

| THE BIGGEST GAINERS |

Fund managers thrive on the concept of sector rotation, which starts with the idea that there are certain sectors that outperform market averages at any point. While it may be impossible to time the ups and downs of sectors, you can jump-start returns by investing in the most favourable sectors and transferring out as they lose steam. For a fund, it is vital to be invested in the right sector at the right time.

Funds are also distributed unevenly because sector sizes are different. For instance, the textile sector is dwarfed by energy or technology. However, there is a distinct concentration in the top onethird sectors. Fewer funds are playing contrarian. Most fund managers focus on company-specific analysis in making their picks. But if company-specific picks are concentrated in a few sectors, the implication is narrower growth.

In the last year, total assets under management in diversified equity funds rose by around 54% to cross Rs 1,67,000 crore. The extra AUM has generally led to absolute allocations rising but despite this, three sectors—automobiles, consumer non-durables (including FMCGs such as Hindustan Unilever and ITC) and textiles—saw disinvestment.

|

| THE LOSERS |

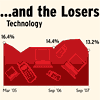

The top five sector allocations as of October 2007 were energy, financial services, technology, engineering and diversified. A year ago, the top five comprised technology, engineering, energy, diversified and automobiles.

Technology lost its premier place largely due to the rising rupee and partly due to uncertainty over spectrum allocation in telecom services. However, it’s worth noting that for fund managers, scaling up allocation to financial services on the back of a booming economy is more fruitful than technology. This does not mean technology is out of favour. The sector has seen a drop of a little over 1%, but in absolute terms it has seen an inflow of an extra 40% or Rs 6,116 crore.

The energy sector has seen a jump in investments after the Reliance restructuring. The power sector, which is a subset of energy, has also done well. Basic engineering and construction (E&C) has continued to gain due to the focus on building infrastructure.

Whether roads, airports or ports, or power stations, E&C comes into the picture and the order book will remain full through the foreseeable future. The other big gainer has been metals. The opening up of mining to private players along with changes in the captive mining policy are seen as favourable for manufacturers, who will be able to control their raw material and fuel chains. Commodity prices have remained strong, so realisations are likely to be good.

Promoters on the prowl

At the time when all classes of investors — FIIs, mutual funds, banks, insurance firms and retail investors — want to increase their exposure to equity, only promoters have increased their holdings in 500 (BSE 500) biggest listed entities. A study by Citigroup’s brokerage division found:

• Promoter holding rose to 58% in the BSE 500 companies in the quarter ended Sep 2007 from 54% in the previous quarter

• BSE 500 companies saw a fall in FII holdings to 20.2% in July-September from 22% in the previous quarter

• Domestic mutual funds reduced their holdings to 3.7% in the same period from 4.3%

• Insurance firms and other institutions reduced their stakes to 5% from 5.5 %

• The companies also saw retail investors cutting down their stake to 9.2% from 10%

Promoters are confident of increasing the value of their businesses in future. Since promoters should know the prospects best, as an investor you too can have faith that stocks will generate good returns in future.

Alpha fund's most wanted

• Alpha funds are betting more heavily on Jindal Steel & Power, Jai Prakash Associates and Reliance Energy than the rest of equity funds.

• In the list of top 25 holdings, 20 stocks are common between Alpha funds and the rest.

| COMPANY | ALPHA FUND* RANKING | ALL FUND RANKING |

|---|---|---|

| Reliance Industries | 1 | 1 |

| Larsen & Toubro | 2 | 2 |

| Bharat Heavy Electricals | 3 | 7 |

| Jindal Steel & Power | 4 | 21 |

| Jai Prakash Associates | 5 | 11 |

| Bharti Airtel | 6 | 4 |

| Reliance Energy | 7 | 13 |

| Oil & Natural Gas Corp. | 8 | 8 |

| National Thermal Power Corp. | 9 | 16 |

| Siemens | 10 | 10 |

| * Alpha funds are the top 10% performing funds. All Fund Rankings are same as Most Wanted rankings | ||

FIIs are looking beyond blue chips, so should you

• FIIs are cutting their exposures to blue-chip Indian stocks in Sensex and Nifty and are allocating more funds to mid-cap stocks.

• Between Sep 2006 and Sep 2007, FIIs increased their holdings in 165 (60%) of the 276 firms that constitute the BSE Mid-cap index.

• During the same period, FII holdings have dropped in 22 of the 30 (73%) Sensex stocks and 31 of the 50 (62%) Nifty stocks.

What it means to you: FII participation is going beyond the obvious large-cap stocks into mid- and small-caps signalling more and diverse investment opportunities.

| Index (No. of stocks) | Direction of FII stock movement |

|---|---|

| Sensex (30) | 73% (down) |

| Nifty (50) | 62% (down) |

| BSE Mid-cap (276) | 60% (up) |

Least-owned doesn't mean least rewarding

• Just as not all most wanted stocks are most rewarding, the converse is also not always true

• This list of stocks with smallest share in funds’ corpus has some super performers as well as draggers

• ADF Foods, an exporter of Indian food, has posted close to 150% annual return

• However, Rane (Madras), a global supplier of auto parts and winner of Deming prize, has lost 29% in a year

| Company | Value (Rs cr) | Shares (lakhs) | Fund count | 1-year return (%) |

|---|---|---|---|---|

| ADF Foods | 3.53 | 4.45 | 1 | 146.28 |

| Pritish Nandy Communications | 6 | 7.79 | 2 | 98.77 |

| ACE India | 13 | 229.35 | 2 | -0.15 |

| Kohinoor Foods | 6.18 | 12.15 | 2 | -2.45 |

| MM Forgings | 14.83 | 10.02 | 6 | -8.82 |

| Stone India | 10.1 | 7.74 | 2 | -11.59 |

| Sundaram Brake Linings | 8.39 | 2.09 | 3 | -25.44 |

| Kale Consultants | 3.3 | 4.23 | 2 | -27.69 |

| Solectron Centum Electronics | 9.01 | 6.05 | 5 | -28.3 |

| Rane (Madras) | 8.2 | 10.73 | 3 | -28.87 |

— Research inputs by Sameer Bhardwaj