The 150-year-old Allahabad Bank has weathered the Swadeshi movement, survived the global monetary crisis of 1913, witnessed two World Wars, seen the nationalisation of banks and fought intense competition from the private sector. But it probably never had to face a situation it is confronted with now.

Twenty-five other PSU banks face a similar situation. These banks - including household names such as the State Bank of India (SBI), Punjab National Bank, Bank of India and Canara Bank - need to raise an estimated Rs 4.60 lakh crore capital within the next four years.

PSU banks account for two-thirds of India's banking system. The capital shortage looming before them threatens the nation's ambition of achieving over 10 per cent GDP growth and having a bustling manufacturing sector through the Narendra Modi governments Make-in-India initiative. It also practically bids adieu to the dream of emerging as a global investment destination, simply because banks that cannot raise enough capital to meet the new CAR norms risk being told by the RBI to stop giving out fresh loans.

"It's like driving a car on a near empty tank," jokes a private banker. Rakesh Sethi, CMD of Allahabad Bank isn't amused by talks of a capital shortage for the bank. "Our capital adequacy at 9.99 per cent is well above the regulatory requirements," says Sethi. Allahabad Bank may meet banking regulator RBI's current floor of 9 per cent, its capital adequacy is nowhere near what is required in the immediate future. Basel III, the third in a series of accords arrived at between the world's economies in 2010 following the global financial crisis in 2008, requires banks around the world to maintain a minimum CAR of 11.50 per cent by March 31, 2019.

Allahabad Bank can't be blamed entirely for its poor CAR. Besides rising NPAs, one main reason for the falling CAR is inadequate capital infusion by the bank's 59 per cent owner - the President of India, who owns the equity on behalf of the government. Successive finance ministers have been stingy about providing capital to state-owned banks. As a result, over the past five years the CAR of almost all the PSU banks have shown a downward trend.

Even though Basel III is a voluntary standard, it urges a country's regulator to bar a bank from carrying on its core business of lending if it doesn't meet the CAR norms by the deadline. It is another matter that the deadline for complying with the norms has been extended twice from March 31, 2015 to March 31, 2018 initially and now further to March 31, 2019. Nothing stops countries from around the world to ask for another extension. But to avoid the ignominy of having a CAR below the new norms in case no further extension is granted, all the PSUs need to start acting immediately. A September 2014 Fitch report says India's banking system needs to raise $200 billion to continue growing at the current rate and still meet the Basel III norms. "The core capital position of the Indian banking system is weaker than that of many Asian banking systems that are also migrating towards the Basel III capital norms," says the report.

An Uphill Task

For PSU banks, it is a question of survival. Its owner - the government - is in no position to provide the capital since it's already struggling to bridge the widening fiscal deficit.

Of the Rs4.60 lakh crore that the PSU banks need to raise, Rs 2.39 lakh crore is the equity capital in the form of Tier-I capital that must either be provided by the government or be raised from the equity market.

Now, given the government's finances, it doesn't have the resources to pump in Rs 2.39 lakh crore (close to 25 per cent of the tax revenue) into the banks over the next four years. Historically, it has allocated less than Rs 20,000 crore a year. In 2013/14 budget, out of Rs 14,000 crore, the biggest bank SBI cornered around Rs 2,000 crore while a small bank like Punjab & Sind bank received around Rs 100 crore.

Barring a handful, most PSU banks are gasping for breath as their capital is fast eroding due to deteriorating asset quality. Faced with a crisis, a couple of months ago the government gave the go ahead to these banks to reduce its stake to a minimum of 52 per cent in phases. In some banks - such as Central Bank of India, United Bank of India, Bank of Maharashtra and IDBI Bank - the government holds up to 80 per cent equity. In others, including SBI, Oriental Bank of Commerce and Bank of Baroda, its stake is around 60 per cent.

The Centre estimated that the banks could mobilise up to Rs 1.60 lakh crore from the capital market over the next four years. It has proposed that the remaining Rs 79,000 crore would come from the Union Budget. Since it would earn an estimated Rs 34,500 crore through dividends from the banks, the net burden over four years would be no more than Rs 44,395 crore, or Rs 11,000 crore a year.

Reality Check

That sounds good and eminently achievable. But look at the reality. Even with the stock markets at a record high and Sensex crossing the 29,000 mark, the current value of the PSU banks' dispensable stock above 52 per cent is barely Rs 1 lakh crore.

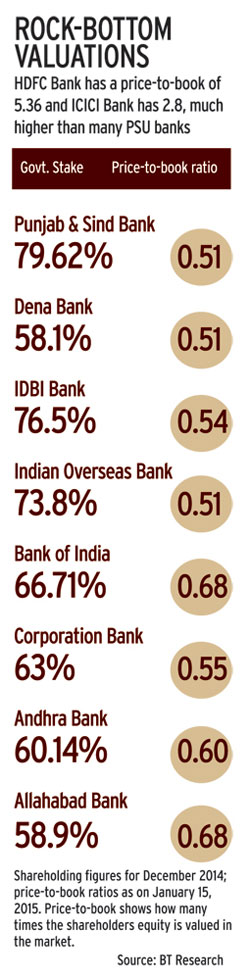

The problem is that investors do not like PSU banks because their NPAs are higher than private sector banks while their profitability is generally much lower. And that is why hitting the capital markets to raise capital is an uphill task. Take, for instance, Allahabad Bank itself where the government holding is 58.9 per cent. The bank has little headroom to raise capital by paring government stake as only about Rs1,000 crore can be mobilised through this route.

"The stake sale exercise would be value destroying for PSU banks," says a private banker. Jayant Sinha, Minister of State for Finance, agrees. "It is our responsibility to ensure that if we are going to dilute our stake, which is the stake of the people, we will do it at an appropriate valuation," he said at a bankers' meet in Pune. Incidentally, it was Sinha's father and former finance minister Yashwant Sinha who once suggested cutting the government stake in PSU banks to 33 per cent. But the younger Sinha, who knows a thing or two about valuations as a former partner of investment firm Omidyaar Network, is treading cautiously.

"The capital position of many PSU banks could be described as weak ," says Saswata Guha, Director (Financial Services) at Fitch Ratings. The RBI's recent financial stability report also noted that the capital adequacy of PSU banks could fall to its lowest, 9.2 per cent, by next year under a severe stress scenario.

If the PSU banks do take the plunge to raise equity, the big question is whether there is investor appetite for their shares even at fire sale prices. In January last year, SBI's equity sale of Rs 8,000 crore could only go through after another state-owned entity Life Insurance Corporation (LIC) pitched in. In fact, LIC has been happily subscribing to the unsold portion of the PSU banks' equity offering. It makes sense because the equity remains within the government ecosystem. But SBI has a better CAR than many of its brethren.

Allahabad Bank has been waiting for better days despite getting a QIP of Rs 320 crore approved by its board. Why wait when you need capital? "Issuing shares at less than book value hurts the existing shareholders," explains Sethi. Allahabad Bank has a price-to-book ratio of 0.68. With the RBI recently allowing a new instrument of Tier-I bonds, the bank is now exploring the possibility of raising between Rs 500 and Rs 1,500 crore through Tier-I and Tier-II bonds, says Sethi. Similarly, Oriental Bank of Commerce cleared a Rs 1,000 crore QIP in January. There is a likelihood of LIC chipping in if there is a tepid response to their offering by institutional investors. But LIC's stake in PSU banks is already on the rise.

Prithvi Haldea of Prime Database, a database on the primary market, says PSU banks could tap depositors or global markets for raising capital.

RBI Deputy Governor R. Gandhi, however, feels reducing stake won't be sufficient since Basel-III projections are based on minimum capital requirements. While speaking in Kolkata on 'Indian PSU Banking - The Road Ahead', Gandhi said PSU banks will have to chalk out a capital raising plan over the next five years. "The banks should actively consider several options including non-voting rights shares, differential voting rights shares, golden voting rights, etc," says Gandhi, who is responsible for regulations and risk management.

Pressing the Panic Button

Gandhi has set the tone for some tough decisions, most of which are in the government's domain. SBI Chairperson Arundhati Bhattacharya echoed similar views when she said the PSU banks should look at issuing non-voting shares.

Praveen Gupta, Deputy MD of SBI, feels it makes a lot of sense for PSU banks to meet part of their capital requirement by raising these bonds. "It not only opens a new class of investors but is also much cheaper when compared against the expected return on pure equity," says Gupta, who is also the CFO of the bank. The government expects a 15 to 16 per cent return on equity from PSU banks. The interest rate offered in Tier-I bonds is a healthy 9.5 to 11 per cent. In August last year, Bank of India raised Rs2,500 crore through these bonds at a rate of 11 per cent. In December, Andhra Bank mobilised Rs500 crore at a much lower rate of 9.55 per cent. Similarly, more than half a dozen banks are already in the market - from south India-based Corporation Bank to Delhi-based Oriental Bank of Commerce - to raise capital through Tier-I bonds.

Meanwhile, banks are also considering selling non -core assets. "The government has advised the bank to dispose of investment in noncore assets to increase internal accruals in order to reduce total capital requirement. The bank is exploring the possibility of such divestment," says Rajeev Rishi , CMD of Central Bank of India. IDBI Bank has decided to sell its stake in NSE as well as Care Ratings. The stake sale in Care Ratings could generate Rs 750 crore. "Banks could also revalue their fixed assets and real estate. This will strengthen Tier-II capital," says an expert. Among the long-term solutions on the table are proposals to create a holding company structure or merge multiple PSU banks to create four or five large banks of SBI's size and balance sheet.

The Genesis

A bulk of the blame for PSU banks' capital crisis must go to the government. It has starved these banks of capital. While the government's own finances didn't permit capital infusion, even the banks failed to generate internal capital because of deteriorating asset quality. Their capital shortfall is now accentuated by the Basel-III guidelines, which require them to raise their capital adequacy every year to absorb any loss from credit, market or operational risks.

The failure of banks globally post the 2008 crash of Lehman Brothers exposed the shortcomings of the Basel-II capital requirement. Under Basel-II, the trading business (equity, bonds, derivatives) required lesser capital than the core banking business of lending to corporates and retail. The banks took advantage of this capital loophole and built large trading books. Similarly, there were other areas, like leverage, where Basel-II had insufficient capital requirements.

The PSU bank chiefs also just cannot escape the blame for the capital mess. Given the small doses of capital infusion by the government and the deteriorating asset quality every year, the banks should have applied the brakes on their growth ambitions. Every rupee of lending consumes capital. For example, if a bank gives a personal loan of Rs 100, the risk weight is 150 per cent of the minimum capital requirement of nine per cent. That's Rs 13.5 on every loan of Rs 100. Similarly, lending to BBB-rated corporate carries a 100 per cent risk weight. Hence, for every corporate loan of Rs 100, the bank has to provide Rs 9 capital. "The banks could have re-balanced their portfolio by focusing largely on assets that require lesser capital," says Rajesh Mokashi, Deputy MD at Care Ratings. Consider mortgages where the risk weight for capital is 50 per cent for loans up to Rs 30 lakh. The high growth between 2009 to 2012 was mainly because of the loans sanctioned in earlier years. Ravi of IDBI defends PSU banks and says there are large term loans where disbursement takes place over a period of time. "The banks cannot turn their back on the commitment on term loans," says Ravi.

M.D. Mallya , former MD of Bank of Baroda explains that a large component of loans went to the poorly performing infrastructure sector in the last three to four years. "Infrastructure is contributing to the deteriorating asset quality. No one would have anticipated that infra could face such difficulty," says Mallya. There are some who attribute the problem to the limited vision of the PSU bank chiefs. The CMDs are keener on demonstrating growth during their tenure (about two to three years) without calibrating it against long term needs based on asset quality and internal generation of capital. This is reflected in the growth in advances of PSU banks in the post 2008 period when everyone else around the world was conserving capital.

Thirdly, the Basel-III roll out has kicked in from April 1, 2013, which is putting enormous pressure on these banks. Basel-III requires banks to keep a minimum Tier-I capital of 7 per cent, out of which common equity has to be 5.5 per cent. "The capital requirement is actually lower during the initial years with higher doses of capital starting from March 2016," says Mokashi of Care Ratings. But given the current state of PSU banks' balance sheet, the RBI is yet to introduce another Basel III guideline to maintain a 0 to 2.5 per cent buffer that protects banks from risks arising out of excessive credit growth.

A Bleak Future?

The stability of PSU banks is of paramount importance for the government and the economy as a whole. After all, they account for two-third of all deposits and advances in India. But the government has fiscal constraints as it targets containing fiscal deficit at 4.1 per cent in 2014/15. In fact, the government had adhered to the Fiscal Responsibility Act in the five years ending 2007/08. The deficit figure was at 2.54 per cent of GDP in 2007/08. But the global financial meltdown washed away all the gains.

The new government under Prime Minister Narendra Modi appears serious about sorting out the capital crisis. In early January, Modi himself flew in to Pune to discuss the various issues confronting PSU banks. "We will have to wait and watch on what sort of capital the government would provide. I don't think that the government would be able to provide unlimited capital," says the CEO of a PSU bank who attended the event. Many bankers after this meeting are convinced that one solution could be consolidation of PSU banks.

"Capitalisation would no longer be an issue if the government reduces its stake to 33 per cent," says Romesh Sobti, MD & CEO of private sector IndusInd Bank. "The problem could be of absorption in the primary market. If the PSU banks improve governance and management quality, the money will certainly flow in from foreign institutional and other investors. But these radical reforms are not going to happen in the next one or two years," says Sobti.

{mosimage}Bankers are pinning their hope on economic revival. It will sustain stock market rally and will help banks raise money at better valuations. It will also have an impact on the portfolio of corporate loans. The credit rating of many companies will improve and hence risk weight assets will go down, thereby freeing more capital. Shinjini Kumar, Financial Services Head, PwC, says the future capital situation depends on how economic growth pans out. "If things improve, it is better for banks and if things deteriorate , there will be a challenge," says Kumar.

The RBI's financial stability report has suggested that the ultimate enhancement in valuations could only come from corresponding improvements in asset quality, governance structures and operational efficiencies. But that's a tall order. Meanwhile, the analyst community is already painting a bleak future. The return on equity (ROE), a measure of returns to shareholders, shows a steep decline for PSU banks. At 9.71 per cent, it was woefully short of 17.06 per cent delivered by private banks. Many PSU banks such as Indian Overseas Bank, UCO Bank, Central Bank and Punjab and Sind Bank have an ROE of less than 7 per cent. This makes them far less attractive for investment. "We have been very cautious on PSU banks, except SBI and Bank of Baroda," says Saday Sinha, analyst at Kotak Securities. "The only bank which has a comfortable CAR is the Indian Bank." There is little hope of improvement of ROE as capital requirements and future capital raising would further impact returns.

And if the new capital doesn't arrive, PSU banks will have no option but to halt lending. Time is of essence. If the government's collective wisdom points to raising capital through stake sale, there is no better time than this. If the solution to the capital crisis lies in consolidation, what are we waiting for?

Research inputs by Niti Kiran and Jyotindra Dubey