You bought that stock years ago when demat was unheard of. You kept the share certificate with your other papers and forgot to demat it even when it was made mandatory. Sometime in between you shifted house. Now, the stock is up many times and you want to sell it. You look for the share certificate but are unable to locate it.

Or, take another case. You have held on to your mutual fund investment for years. But over the period, your signature has changed and does not match the records of the fund house. Your redemption request is rejected and you are told to provide proof that you are the same person who made the original investment. You feel helpless.

Among all your investments, the one you need to be most careful about is real estate. You just cannot afford to get stuck. The reason is simple. It will invariably be your biggest single investment. Moreover, there is no regulator to protect you. "Real estate is the most risky investment you make in your life because it involves the largest single investment. You have to take an informed decision," says Vineet K Singh, business head, 99acres.com, a property portal.

Solution: You can offload illiquid stocks in call auction sessions. Stock exchanges identify illiquid stocks at the start of every quarter and shift them to a call auction mechanism. Then, they organise call auctions in these stocks at various times during the day. Orders received over a period are then collected and opening price and quantity traded derived based on the basis of supply and demand. These trades do not involve any costs.

But what about stocks with zero liquidity? Nikhil Kamath, director, Zerodha, says, "A number of entities buy such shares. But the price discount here can go up to 50%." Zerodha is an online brokerage.

"There is no way an investor can sell (through usual channels) if the liquidity is zero. He will have to use informal avenues," says Sudip Bandyopadhyay, managing director and chief executive officer, Destimoney Securities.

"To avoid such a situation, one should avoid small-cap stocks, which have a high chance of becoming illiquid if the market's mood turns bad," says Hiren Dhakan, associate fund manager, Bonanza Portfolio.

Delisted stocks: Delisting is removal of a stock from trading on an exchange. Companies delist when they want to expand/restructure, are acquired by others, or their promoters want to increase their stakes. In such a case, they pay investors. Or, it can be forced by exchanges for noncompliance of rules.

In voluntary delisting, companies usually offer shareholders more than the market price for tendering their shares. In forced delisting, exchanges appoint an expert to arrive at the shares' fair value.

Gokul Raj P, executive director and head, investments, HBJ Capital Services, says, "Forcefully delisted companies give two-three years to the public to tender their shares. Investors can also sell shares to other parties through private placement."

Solution: K Sandeep Nayak, executive director and chief executive officer, Centrum Broking, says investors have to approach promoters or other shareholders for buyback.

Lost share certificate: You may not be able to sell your shares if you have lost the share certificate. Of course, such a situation cannot arise if you have shares in the demat form.

Solution: The way is long-winding and starts with filing a first information report or FIR. You should have the folio or certificate number for starting the process for getting a fresh certificate.

Scrip suspended from trading: Stock exchanges often suspend trading in certain shares due to non-fulfillment of regulatory requirements. Usually, companies have to disclose their shareholding pattern, financial statements, trading in shares by insiders and follow certain corporate governance practices as part of listing agreement with exchanges. In case of a violation, an exchange may suspend trading in the company's shares until it fulfills the terms of listing for the latest quarter. A total of 417 companies have been suspended from trading on the Bombay Stock Exchange in the past 10 years.

Solution: Suspended shares can be offloaded through off-market transactions. Santanu Syam, executive director, operations, Angel Broking, says, "If the suspended securities are held in demat form, one can do an off-market transfer for a consideration into the buyer's DP account.

If the holding is in physical form, the investor can approach the RTA for transferring ownership to the buyer. The settlement is outside the purview of exchanges."

Of course, one can wait for the suspension to be lifted, but that can take long. Kishor P Ostwal, CMD, CNI Research, says, "Re-listing may take years and that, too, if promoters rectify the filings. Since 1996, barely 200-250 companies out of the 1,500-odd that have been suspended have been re-listed."

Unlisted Shares: You may be holding shares that have never been listed on exchanges. These can be sold through unofficial channels. These shares may be traded through the over-the-counter (OTC) market, and are, therefore, called OTC securities.

Solution: You need to approach broking entities that deal in unlisted scrips.

Shashi Kumar, a New Delhibased businessman, was holding shares of unlisted Ratnakar Bank which he sold to Abhishek Securities at Rs 117 apiece. His purchase price was Rs 103. Firms such as 3A Capital Services, Kajaria Securities and Finance and Oswal Trading also buy/sell unlisted shares. You can check the list of shares on their websites.

Some of the big unlisted companies whose shares are being traded in the unofficial market are Bombay Stock Exchange, Cochin International Airport and Essar Steel. But there is a huge difference in their bid and ask prices. For example, at Abhishek Securities, the buy price of Bombay Stock Exchange is Rs 165 while the sell price is Rs 195. Similarly, it is buying Cochin International Airport shares at Rs 105 and selling at Rs 175.

MUTUAL FUNDS

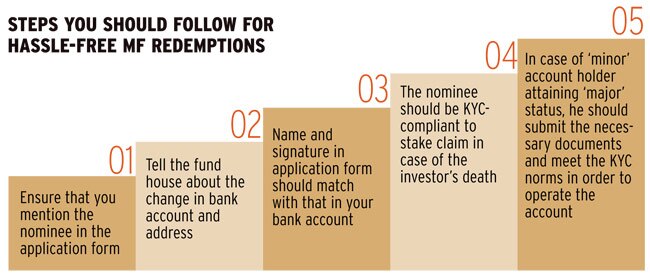

Signature mismatch: In some cases, the signature in the redemption form does not match with that in the application form submitted at the time of investment. In such a case, the mutual fund will reject your withdrawal request.

"This problem does not exist for online investments," says Srikanth Meenakshi, co-founder and chief operating officer, FundsIndia.com.

Name Mismatch: The name in the fund folio can be different from that in the bank account. The reason could be data-entry error by the fund house or a typo by the investor. It could also happen due to change in name after marriage or divorce. In such cases, the mutual fund company will not be able to transfer money to the bank account. It may, instead, issue a cheque to the investor. The process, of course, will take time.

Further, if the cheque is sent to your old address, it may never reach you, leading to further delay.

Solution: It is important to ensure that the name in the mutual fund application form matches with that on the Permanent Account Number (PAN) card and in the bank account. A data-entry error can be corrected by contacting the fund house's customer service department or providing a written request.

In case of change in name, the investor has to attach a request letter, a notarised copy of the relevant notification in a government gazette, attestation from the bank manager confirming the investor's name, branch, account number and signature, plus any other legal document with the new name (the documents may be bank statement and attestation from the school).

In case of error by the investor, he/she has to attach along with the request form a mutual fund account statement, a blank cheque that has the name of investors, a photo identity proof (PAN, passport) with his/her signature and an indemnity bond on a plain paper signed by the account holder/s.

Imagine a situation where your mutual fund folio is linked to an account that you have not used for years. The ATM card, too, has expired, and you do not have a cheque book either. If your money goes into this account, it will remain stuck till you visit the bank and get your address updated. Then you will have to apply for the ATM card and cheque book to withdraw the money.

If you have not updated your address in the mutual fund's records, the cheque, too, will be sent to your old address.

Solution: The best option is to get bank account and address updated with the fund house in time. Otherwise one can submit a request for change in the bank mandate along with the redemption request. Or, one can first apply for change in bank details and submit the redemption request after seven days.

Change of status from minor to major: Though mutual funds do not allow third-party investments, natural and legal guardians can invest in the name of minors. However, when the minor becomes major, the guardian cannot do any transaction on his behalf.

Solution: The minor status has to be changed by submitting know your customer, or KYC, documents.

Nominee not KYC-compliant: It's not mandatory for the nominee to be KYC-compliant at the time of investment. But in the event of the investor's death, he/she has to complete the KYC procedures to claim the money.

Solution: It is advisable for the nominee to be KYC-compliant

No nominee listed: The process of claim settlement is easier if the investor had listed nominee( s). In such a case, all that the nominee has to do is to make a written claim request and submit it with the death certificate.

"Along with this, information required for creating a new folio in the name of the nominee such as bank account and PAN will also be needed. It is possible to have multiple nominees for a folio, and in such cases, each nominee will be allotted the apportioned number of units as per the intent of the original (deceased) investor," says Srikanth Meenakshi of Fundsindia.com.

"If the investment is above a threshold (currently Rs 5 lakh), instead of a personal affidavit, a legal heir certificate will be required," says Srikanth Meenakshi.

INSURANCE

Signature/name mismatch: In case of deathrelated claims, this is not an issue. But if you have to claim maturity benefits, this will delay disbursal. This is because the insurance company will go for additional verification in such a case.

Solution: You may have to provide authenticated specimen signature to the insurer. "This is done to ascertain the authenticity of the claim. This is in the interest of the customer and is done as a safeguard against fraudulent claims," says Mayank Bathwal, deputy chief executive officer, Birla Sun Life Insurance.

"Banks can be cooperative. If not, you need to close the account and open a new one," say Shilpi Johri, a Gurgaon-based certified financial planner.

The process for correction of name or signature is similar to that in case of mutual funds.

Change in/absence of KYC: In case of death claim, KYC details of the insured and the nominee will necessarily differ, but this will not in any way delay the claim process. However, the nominee must be KYCcompliant.

While claiming maturity benefit, any anomaly in KYC details of the insured will lead to rejection of the application. The insurer will seek additional verification as proof of the change.

Solution: You should keep your insurer updated about your KYC details. "It is beneficial for the policy holder to keep the insurer informed about changes in KYC details such as address and phone number during the life of the policy. In case that is missing, additional KYC verifications are done prior to disbursement of the benefits," says Vikas Gujral, executive vice president and head, Customer Service & Operations, Max Life Insurance.

Absence of nominee: The life insured may not have a nominee. Or the insured and the nominee may expire at the same time.

Solution: In such cases, the claimant needs to submit a succession certificate issued by a court. The certificate should specifically provide for disbursement of the insurance money.

However, if the insured had a will, the benefits are disbursed to Class-I legal heirs and/or heirs designated by the will. "If there is no nomination, or the nominee dies before the insured, or in case of death of the appointee in case of a minor nominee, the claim is treated as an open title claim. It is settled on receipt of legal evidence of title such as succession certificate," says Frederick D'Souza, senior vice president, underwriting, HDFC Life.

Even in cases where the nominee has been mentioned, Class-I legal heirs can restrain the insurer from payment to the nominee by convincing a court to issue a prohibitory order.

The proposer and the insured are different: When the proposer (owner) and the life insured are different (for example, when the employer insures his employee, husband proposes for the wife or a parent insures the minor child), on death of the proposer, insurers give an option for changing ownership so that the policy can continue.

Solution: Insurers offer riders to enhance the insurance plan at a nominal price. If the proposer had opted for the waiver of premium rider benefit, the insurer will waive the premium and the policy will continue.

Non-payment of premium for full term: This is another common reason for withholding of insurance benefits. "People are often unaware of the policy terms and conditions and stop paying premium after the lock-in period (five years). The policy lapses as a result," says Vivek Karwa, a financial planner.

In such a case, the cover ceases to exist. The policy holder is paid the surrender value only if he/she has paid the premium for at least three years in case of policies with tenure of 10 or more years. Shorter policies acquire surrender value after the premium has been paid for two years.

Solution: A lapsed policy can be revived by paying the pending premium (plus interest). "The policy holder must ensure that the policy is kept in force by paying premiums regularly," says D'Souza of HDFC Life.

"By incorporating such a clause, the developer is trying to control his own price. But it eats into your profits. You should know (before buying) whether the builder asks for transfer charges," says Rohit Sharma, assistant vice president, Research and Real Estate Intelligence Services, Jones Lang La Salle.

No transfer till possession: Builders often restrict transfer of the property till possession. You are locked in till the project is completed. Some even impose charges for the second seller as well if he/she tries to sell out before completion of the project.

Bar on selling below a price: Inclusion of this clause means you cannot sell the property below a particular price

Solution: The most important thing is to read the buyer-builder agreement carefully and be aware of the restrictions. If possible, negotiate with the developer. "These are usually standard clauses and not negotiable. But if you are a high net worth individual who signs big cheques, you can negotiate," says Vineet K Singh, business head, 99acres.com.

Title not clear: If this happens, there is danger of the asset becoming illiquid.

Timing market wrongly: Has the price of the property you bought not risen as much as you had wanted or has, in fact, declined? This could have happened in the recent slump that has hit the real estate sector, leaving many investors in the lurch. "The flipping market is gone for good. Six to 12 months' trading market has gone forever, at least for the next three-five years," says Singh.

Solution: If you are stuck with a property that has not reached the target price, the best option is to hold on till the sentiment improves. "As of now, the market is for holding on to properties, not trading. If you cannot hold on, then it is a distressed asset, and it will be sold like a distressed asset," he says.