It's a high stakes war to dominate India's Rs 2.6 lakh crore telecom sector. A corporate fight as brutal, intense, debilitating and bruising as that seen in the cash-guzzling e-commerce business. Indeed, the giants in both these sectors are involved in a game of one-upmanship for customer acquisition through attractive freebies which are burning a hole in their balance sheets. But that's where the comparison ends, and the contrast begins. On every parameter, the telecom clash dwarfs the e-commerce battle: telecom has seen an investmentof Rs9.27 lakh crore against about Rs 71,000 crore in e-commerce; it employs 4 million against 0.35 million in e-commerce and its debt burden of Rs3.81 lakh crore is next only to the power sector in India.

And, it's a no holds barred contest in telecom for another reason. The winner will actually lord over the most precious commodity of the future: DATA.

Little wonder then that the incumbents Airtel, Vodafone, Idea Cellular and Tata Teleservices, besides Reliance Communications (RCom) and BSNL/MTNL, have taken on the challenge thrown by the Mukesh Ambani-owned Reliance Industries' bold and disruptive Rs 2,00,000 crore telecom play, Reliance Jio. Retreating is not even an option. All the large players have invested between $15-20 billion besides raising a debt pile of between Rs50,000 crore to Rs1 lakh crore.

So, Jio's aggressive tariff cuts are being met with matching offers to retain customers; 4G networks are being expanded at breakneck speed; and the chatter to merge or acquire is louder than it has ever been. Jio's launch on September 5, 2016 was a watershed moment in India's telecom space.

First, by making voice calls free for all subscribers, Jio hit at the very root of the incumbents business - voice still constitutes 70 per cent of their revenues. Second, by offering the service free for seven months, it eroded the subscriber growth of rivals while ramping up its own base by nearly half a million subscribers a day. As a result, while pricing voice is becoming unthinkable, data prices have almost halved.

Nearly all the players have begun to bleed profusely. And they are reacting by coming together to, at least, make it a battle of equals on subscriber base, network expanse and spectrum. It began with Vodafone, number two in terms of subscriber base, agreeing to merge with number three Idea Cellular, to create India's biggest telecom company.

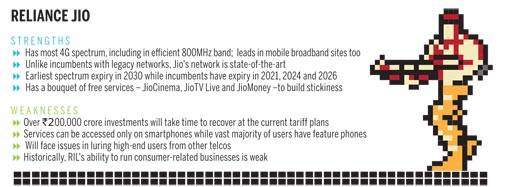

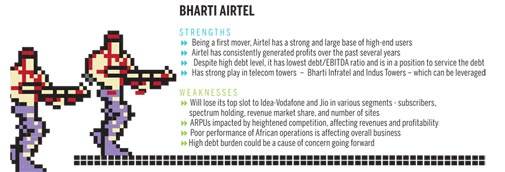

Market leader Airtel had been preparing for such an eventuality for 20 months, acquiring smaller players such as Telenor and 4G spectrum or businesses from companies such as Videocon Telecom, Augere Wireless, Aircel and Tikona. Meanwhile, reports suggest that Tata Tele has been in discussions with RCom for a possible merger. RCom itself has signed up to merge Aircel and acquire MTS in the past 17 months. RCom chairman Anil Ambani has also announced that the telco is in a 'virtual merger' with brother Mukesh's Reliance Jio. RCom has over 95 million subscribers while Jio raced to 100 million customers within 170 days of entering the market.

Just before the launch of Jio, India had 12 telecom service providers. Today, seven months later there are just five - Bharti Airtel, Vodafone-Idea, Reliance Jio, RCom-Aircel combine and state-owned combine of BSNL and MTNL. This is just the beginning.After the current round of M&As, the number will most likely shrink to three (plus BSNL/MTNL). The Vodafone-Idea merger will dethrone market leader Bharti Airtel both in terms of subscribers and revenues.

The $23-billion Vodafone-Idea merger is the biggest ever in the history of telecom and corporate India. It is bigger than the combined size of Bharti's acquisition of Zain (valued at $10.7 billion) in 2010 and Vodafone's purchase of Hutchison Essar ($10.9 billion) in 2007. Airtel, post the recent acquisition of Telenor India, has 320 million subscribers against 395 million for Vodafone-Idea.

Jio has 120 million subscribers, of which 72 million will start paying from this fiscal. It has set the stage for what could be a bruising battle to be the leader in the world's second largest telecom market by subscribers. "Consolidation helps reduce costs and improve network efficiencies. The aggressive tariffs will continue in this calendar year before there's some stability among operators," says Jaideep Ghosh, Partner at KPMG India.

In all likelihood, the sector will be divided between three large players - Vodafone-Idea combine, Airtel and Jio - once the consolidation phase is over.

Each of these entities will play on their strengths in spectrum holding, profile of customers, strength of balance sheet, network capabilities and value-added offerings.

A THREE-WAY FIGHT

When Jio stormed the market with its free unlimited calls and data, it was clear that only stronger players could survive its onslaught. In fact, Jio's disruptive pricing threatened even the established telcos. The quarter after the commercial launch of Jio's services was terrible for incumbents. Airtel, for instance, has reported 54.9 per cent drop in net profits in the third quarter of 2016/17 over the same period previous year. Idea Cellular registered a loss of Rs 383 crore, its first-ever quarterly loss since its stock market listing. Vodafone too felt the heat and, recently took e5 billion write off on its Indian assets.

Even the massive investments of older operators didn't help much. Vodafone and Idea, which were weaker on a standalone basis, have joined hands to emerge as the leader in what seems like a three-horse race.

The consolidation in the telecom sector was long-pending. For instance, when the Supreme Court cancelled 122 telecom licences in February 2012, there were 15 mobile operators. The presence of a large number of players has resulted in fragmentation of spectrum, severely compromising its efficient usage. Telecom is a business of scale. During his visit to the World Economic Forum Annual Summit 2017 in Davos, Sunil Mittal, Chairman of Bharti Airtel said in an interview that "Jio is a big player that has entered the industry and smaller players are looking to exit over the last few months. The Indian telecom industry could finally come down to four players."

"What are the chances of having a standalone Reliance Communications (RCom)? There are signs that RCom and Jio will work together, if not merge," says Mahesh Uppal, director of consultancy firm ComFirst India. Most experts concur. "There will be three meaningful players in the market. If no one absorbs RCom, then it will be fourth but then RCom doesn't have enough resources to fight a data war," says another analyst. At the last Reliance Communications Annual General Meeting, promoter Anil Ambani admitted that he was joining forces with Reliance Jio. "As far as our 100 million customers are concerned, as far as our 1 million retailers are concerned, as far as our employees are concerned, and as far as our vendors and partners are concerned, there has already been a virtual merger of the two organisations (RCom and Jio)," Anil Ambani said. "Our spectrum is shared, our network is shared, our fibre is shared, our towers are shared, our voice is shared," he said. On a standalone basis, RCom has been posting net losses for the past two financial years (Rs154 crore in 2014/15 and Rs1,624 crore in 2015/16). Going by the trend of past three quarters, the losses in 2016/17 are expected to increase substantially over the previous years.

The situation of Tata Teleservices (TTL), another marginal player, is worse. In the past two financial years - 2014/15 and 2015/16 - it had a cumulative net loss of Rs7,079 crore. There are reports that TTL is talking to RCom-Aircel combine for a possible merger. If that happens, the Jio-led block will become even bigger and overtake Idea-Vodafone in terms of spectrum holding and Airtel in terms of subscriber base. The government-run MTNL and BSNL, which are reportedly exploring a merger, will continue to operate as minor players. "The state-run telco is important from the government's point of view; otherwise private players will have a free run," says B.K. Syngal, Senior Principal, Dua Consulting.

INCUMBENTS FIGHT BACK

Airtel's acquisitions and Idea-Vodafone merger are primarily aimed at adding more spectrum to their portfolio. It was more gradual in the case of Airtel. The Vodafone-Idea merger was a reaction to the damage caused by Jio. The merged Idea-Vodafone entity will hold about 1,850 MHz spectrum across different bands, including about 1,645 MHz of liberalised spectrum. In comparison, Airtel's spectrum holding is 1692 MHz and Jio has 1301 MHz.

The pooling of spectrum holdings - as is the case with Vodafone and Idea - leads to higher network capacity, which in turn means that the telcos can use airwaves more efficiently than they were doing independently. For instance, spectrum needed to deliver voice services to the existing Idea and Vodafone customers will reduce to 400 MHz from 600 MHz now. The freed 200MHz can be deployed for data services. "Data is a bandwidth guzzler. Voice is simple. Two plus two is always more than four when it comes to spectrum," says an analyst. Idea-Vodafone will have combined 273,000 sites, of which 189,000 will be broadband sites. "This should allow the combined company to accommodate over 15 times more data volumes than currently, and thus match Jio's data offerings," says a Motilal Oswal report. Airtel has 185,000 2G sites and 171,000 3G or 4G sites whereas Jio has 249,000 4G sites.

THE FIRST MOVER

ADVANTAGE

The biggest strength of Airtel is that it entered the market when mobile calls were expensive. Only those who had higher spending power could afford its services. Airtel still has a substantial chunk of these users in its portfolio. Typically, high-end users are not price-sensitive, and have loyalty towards the brand. Airtel has reduced tariffs for its postpaid customers in response to Jio. Its aim is to match Jio's low price points to keep these high-end subscribers in its fold. Vodafone India too has a significant number of high-end subscribers, thanks to its predecessor Hutch which was a dominant player in metro cities right from the start. Idea, on the other hand, started off with rural and semi-urban towns, and entered metros much later - Mumbai in 2008, Chennai and Kolkata in 2009. Over the years, Idea and Vodafone's customer profiles haven't changed much.

Jio's customer base is largely built on freebies, and there's still not much clarity on the profile of its subscribers. Experts, however, say that Jio's not a preferred brand for high-end users because many of them had a poor first-hand experience of RIL's telecom services in its previous avatar over a decade ago. But for new-generation, data-hungry users, brand names don't matter.

GAME OF SPECTRUM

Both Idea and Vodafone missed the 4G bus. By the time the market was moving towards 4G, it was already too late. Take the case of spectrum auctions in 2010, when Reliance Jio and Airtel aggressively bid for airwaves in 2300 MHz, one of the bands to deploy 4G technology - Idea and Vodafone then did not bid. In the subsequent five auctions, both picked up 4G spectrum but that was still far less than Jio's and Airtel's 4G spectrum. In a January report, brokerage CLSA points out that before their merger, Vodafone's 4G spectrum holding stood at 410 MHz whereas Idea's holding was 440 MHz. In comparison, Airtel had 730 MHz of 4G airwaves. Unlike Vodafone and Idea, Airtel was quick to sense the 4G opportunity and started gobbling up spectrum gradually - through auctions and acquisitions.

Not just the quantum of spectrum, the type of airwaves that Jio and Airtel hold are superior to Vodafone-Idea combine. For instance, Jio has spectrum in the lower-frequency bands such as 800 MHz, 1800 MHz and 2300 MHz while Vodafone and Idea have spectrum in the higher-frequency bands such as 1800 MHz, 2300 MHz and 2500 MHz.

Lower frequency bands are considered superior for the delivery of 4G services because they give better indoor coverage. "Airtel is still the most efficient operator because of its size, scale and the superior network that they have built," says Bhupendra Tiwary, Lead Analyst (telecom & media), ICICIdirect.

As recently as 2015, Vodafone India was seemingly ignorant about the fast-changing telecom landscape. In a response to Business Today's query on its 4G plans, the telco had said that "today a customer is looking at a seamless mobile internet experience especially for videos and is not bothered about the technology (2G, 3G or 4G).

Hence, investing in 3G in the medium term is a viable proposition." That approach turned out to be a disaster. Vodafone underestimated the demand of data-hungry consumers who were asking for higher data speeds than 3G. "Their reluctance to invest in 4G until recently has left them with no option but to either merge or perish," says an analyst.

BURDEN OF DEBT

Debt is a big area of concern for almost all operators at the moment. A large part of the investments are funded through debt that stands at Rs 3.81 lakh crore, making it one of the most indebted sectors. The rise of debt is primarily driven by five successive spectrum auctions between 2012 and 2016. These auctions saw aggressive bidding by operators leading to three-fold jump in debt from Rs1.23 lakh crore in 2009/10. The high debt level is not an issue as long as businesses generate enough profits to take care of debt repayments and interest costs. But that's not the case right now.

The gross debt of Idea-Vodafone combine is higher than its closest rival Airtel. It's also more leveraged than Airtel. For instance, Idea-Vodafone has debt-to-EBITDA (earnings before interest, tax, depreciation and amortization) ratio of 4.4 as against Airtel's 2.8 post the Bharti Infratel deal. Analysts at Motilal Oswal expect Idea-Vodafone's debt-to-EBITDA ratio to rise further to 5.6 in 2017/18 before starting to drop. Debt-to-EBITDA ratio indicates a company's ability to pay off its debt. A high ratio shows that a company is deep in debt. Vodafone-Idea has indicated that once the benefits of the synergies are achieved, its net debt-to-EBITDA will touch 3.

But there's a fair bit of scepticism about the synergy benefits being talked about by both telcos. Analysts say that targeted synergies and actual synergies have a gap. Brokerage Bernstein, in a March report, says that "mergers are complicated in the best of times. Synergies are only delivered if staff are let go; network overlaps eliminated; brands integrated and marketing budgets reduced. All of these are disruptive at the best of times, and in almost all cases result in share loss. We expect they will lose 5 per cent revenue market share in 2017/18 (as Jio starts charging) and a further 2 per cent during the network integration period. This implies their combined subscriber share will fall from the current 40 per cent to 34.6 per cent by March 2018."

Vodafone India, in a post-merger investors call, has said that the debt held by the new entity is primarily spectrum debt, owed to the government over a long period, typically at least ten years.

In the face of heightened competition, telcos have to constantly invest in network expansion and value-added services which could further raise debt levels. Airtel is spending about Rs20,000 crore every year under its Project Leap programme to upgrade and expand infrastructure. Jio will be spending Rs 12,500 crore on network expansion. According to some estimates, Idea-Vodafone would spend Rs 12,000 crore for capital expenditure.

Together, these telcos will be spending about Rs45,000 crore annually till 2018. Where will the money come from? Telcos are exploring selling stake in non-core assets, mainly towers. For instance, Airtel, which held 72 per cent stake in towers company Bharti Infratel, has recently sold 10.3 per cent of it to a consortium of funds for Rs 6,194 crore. As of last December, Airtel had a net debt of Rs 97,395 crore.

There is an opportunity for Vodafone-India combine to monetise its tower assets. Vodafone India has around 10,500 standalone towers, and Idea has around 9,000 towers. Besides, Idea owns 11.2 per cent stake in Indus Towers. Analysts caution that selling of towers assets is not as easy as it seems.

Take the case of RCom, which had to wait for a couple of years before finding a buyer for its tower assets. Harsh Jagnani, Sector Head (Corporate Ratings) at ICRA, says that top three players have the ability to refinance their debt due to strong parentage and access to global markets. "Nearly 1.65 lakh crore is spectrum-related debt. The spectrum debt is the payments that telcos owe to the government. These payments cannot be deferred. For non-spectrum debt, there are refinance options if there are not sufficient cash flows or other investment requirements," he says.

THE FINAL BATTLE

On the last day of its Prime membership programme, Jio announced that 72 million have subscribed to its paid programme, and with the first recharge of Rs303 and above, it will be giving three months of free service till July. Thats a monthly ARPU of Rs 100 but Jio has finally begun to charge for services. Experts say that until Jio doesn't attain meaningful paying customers - over 100 million - it will continue to disrupt the market. ICRA's Jagnani says that competition will remain high for the next few quarters.

Jio has invested over Rs 2 lakh crore. If the depreciation period for this investment is 20 years, the yearly cost would be around Rs 10,000 crore. In addition, there will be operating expenses and interest costs. On a conservative level, Jio would need annual revenues of Rs 25,000 crore to just recoup its expenses. Syngal of Dua Consulting says Jio's game plan is to enroll customers for free and start charging at discounted rates. "Once the users get used to it, they will jack up tariffs," he says.

If Jio raises tariffs, others are expected to follow suit. Some analysts say that Jio has indeed priced its Prime membership plan at a premium to the sector's ARPU rates. In 2015/16, the ARPU of the entire sector stood at Rs 127.

Jio has substantial spectrum holding in 850 MHz band and has no legacy network unlike Airtel, Idea Cellular and Vodafone. For instance, Airtel still has about 349 MHz of 2G spectrum and some 185,000 GSM sites, which are deployed to serve its voice customers - they have lower ARPUs but it's almost difficult for Airtel and Idea-Vodafone to shun them and move to an all IP-based network like Jio. There are about 120 million data customers out of 400 million subscribers of the Idea-Vodafone combine. "As early entrants, Idea and Vodafone deployed technologies available at the time. They operate multiple networks - 2G, 3G, 4G. This has increased complexity and costs. Jio, on the other hand, has no legacy network and operates only 4G services," says Uppal.

Most countries have a maximum of two technologies but India is a unique country where all three technologies co-exist, points out Rajan Mathews, Director General, Cellular Operators Association of India (COAI).

ICICI direct's Tiwary says that the new entrant will be targeting ARPU between Rs 250 and Rs 300 with a majority of user base at the Rs 303 plan (with unlimited voice calls and 28 GB data) and some at the Rs 145 plan (with unlimited voice calls and limited data). So far, Jio's services - 4G data and VoLTE calls - can be accessed on just smartphones. India is predominantly a feature phone market with nearly 700 million users as compared to about 300 million smartphone users. That's where Airtel and Vodafone-Idea have an edge over Jio. Also, the growth of the smartphone market is cooling down - last year was particularly weak for it. According to CLSA, smartphone users are likely to touch 331 million in 2016/17, up 19 per cent a year ago while the growth in the previous two financial years was 40 per cent (2015/16) and 57 per cent (2014/15).

Jio is now planning to target the lower-end of the market with its feature phones that are capable of making voice calls over LTE network. "There is a strong possibility that Jio may launch low-end 4G feature phones priced below $20 and bundle them with long-term, inexpensive data plans in an attempt to increase the 4G addressable markets such a move would hurt the competition as, currently, as much as 70 per cent of cash flows for the rest of the telcos accrue from voice business," notes an HSBC report published in January. Email queries sent to Airtel, Vodafone India, Idea Cellular and Reliance Jio didn't elicit a response.

On the value added services front, there's no major difference in the services offered by large telcos. Services like live TV, movies, music, etc. are standard across all operators. Vodafone, for instance, has Vodafone Play where it offers movies, music and TV. Airtel too has Airtel Movies, Wynk Music and Pocket TV.

Analysts say that Jio seems to have taken a lead in offering a wide and rich variety of content. "Jio has rolled out live TV streaming services and Bharti Airtel has so far responded very tactically. We believe it may be necessary for Bharti Airtel to launch similar services. A delayed response could have an adverse impact on market share in the mid or high-end segment," says a HSBC report.

The bugle, then, has just been sounded.

Additional reporting by Nevin John

@manukaushik