Little drops of water make a mighty ocean. Yes, it’s a cliché, and like all clichés, it’s true. More so, when it comes to your money. But what the clichés don’t say is that the little drops have to be collected for a long time before they can make an ocean. It’s the same with your investments, especially in Ulips as these are primarily insurance products. It seems obvious, but the problem arises because many investors feel it’s good to exit in three to five years as the investment component functions like a mutual fund.

Unlike equity mutual funds, and to an extent, tax-saving mutual funds, which have a short- to medium-term investing time frame, Ulips have longer lock-ins. Puneet Nanda, executive vice-president and CIO, ICICI Prudential Life, says, “Ulips allow investors to enter the stock markets indirectly and in a disciplined way. They act like SIPs.”

Insurance cover: Over Rs 15 lakh “Traditional insurance plans give very low returns. I had not expected the Ulip fund to grow so well.” Delhi-based Kumar invested in mutual funds but stayed away from insurance because the returns were very low. He took a Ulip to cover his life and provide a sizeable corpus for his three-year-old daughter after a friend told him about the concept. Under the plan, if a claim is made in the next 15 years, the proceeds will go to his daughter when she turns 18. |

“Mutual funds churn portfolios frequently. Ulips are conservative and take much longer calls on the market.” |

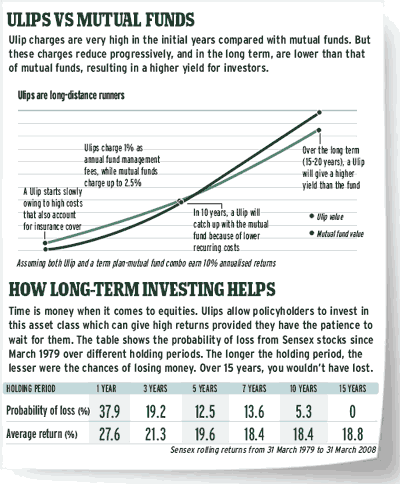

Some of the more aware investors seem to agree. “I have investments in stocks, funds, and now, Ulips. In the long term, the fund manager’s ability is better utilised in Ulips compared with mutual funds,” says Bangalore-based T.P. Ravi Kumar. Critics say that the Ulip charges are exorbitant, making mutual funds the better and cheaper option. You end up paying all sorts of fees—administrative charges, mortality charges and, of course, fund management fees—when you invest in Ulips. But stay invested for 10-20 years and you’ll get back all this and more (see chart).

Ulips charge as much as 25-40% of the premium as administrative costs in the initial years. Some of them even charge 100% in the first year. However, these charges taper down to about 1% by the fourth or fifth year. Most diversified equity mutual funds charge up to 2.5% of the corpus value as fund management fees every year. In the long term, say 15-20 years, this small difference in annual fund management charge can have a significant effect on your returns.

Ulips also gain from the fund management philosophy, which does not believe in frequent redemptions. “We don’t take very aggressive stock or sector calls. In general, we maintain a well-diversified portfolio. It has to do with the long-term nature of funds that we manage,” says Nanda.

The long-term nature of these products is perfect for Delhi-based Mahender Kumar. He wants to ensure that his three-year-old daughter has a decent corpus when she turns 18. “The advantages of a Ulip child plan are the long-term gains from stock markets and the flexibility to ride from one fund type to another to hedge between equity and debt,” he says.

Kumar started with maximum equity exposure two years ago, but moved to debt in late 2007. “I was lucky because the Ulip allowed this. Of course, the value of my equity funds eroded during the same time,” he says. The free switches across fund types and the provision for top-ups add to the benefits of long-term investing through Ulips. Cost-wise, switching from equity to a debt scheme and then back to equity in a mutual fund is expensive compared with Ulips. In the long run, even a 1% annual charge can make a huge difference in returns.

Finally, here’s the clincher. If you still decide that Ulips will do well in the short-medium term and exit early, don’t be shocked when you find that you have to pay for this. Exiting Ulips, especially in the early years, can hurt you financially because most of the charges and fees are paid upfront. But if you stay put, making smart switches within the plan options, you will end up a winner.