There would be few takers for this one. Most will scoff, few might give it a moment of thought and only a handful will probe further. Justifiably so. For when someone claims that your finances are in distress, he must be kidding. The truth is that they were never healthier. Fatter paychecks give it volume and strong investments provide the required depth. The party is in full swing.

But if so, explain why have your phone bills doubled when call rates have been slashed? Or why there are more restaurant bills than currency notes in your wallet? Or why are the zeroes stacking up faster in your mortgage rather than pay cheque? Because the whole truth is that your finances are ailing. Some force is drawing out the health (read money) of your budgets. And if you do not recognise the symptoms, it is because the nature of the illness is very new.

Initially, many consumers ignored the pinch. Those little warning signals when you defaulted on a credit card payment or when your bank balance hovered dangerously close to the minimum value went unheeded. Over-estimation of purchasing capacity aided by easy credit through cheap loans had everyone going on a spending binge, unmindful of how the small additions in bills were stacking up.

But with inflation in necessities such as groceries at over 10% and interest rates breaching the 14% mark, you can no longer deny the strain on household budgets. And the hard fact is, maintaining your lifestyle will only get costlier as taxes ramp up and your consumption of services and discretionary products increases.

But with inflation in necessities such as groceries at over 10% and interest rates breaching the 14% mark, you can no longer deny the strain on household budgets. And the hard fact is, maintaining your lifestyle will only get costlier as taxes ramp up and your consumption of services and discretionary products increases.

The inherent silence and invisibility of these factors makes them more potent. With inflation rates bandied all over the place, you probably do think of price rise when purchasing fruits to stock up the fridge.

But when you are struggling to squeeze out some thousands of rupees to pay an odd bill, thoughts of budget hassles never enter the mind. Even after identifying the pressure points on your finances, chances are you will never be able to distinguish them in your monthly expenses. Neither will your neighbours, relatives or friends. A worrisome thought indeed.

If you admit to the strain on your finances, it is time to take action. But damage control can begin only when you know exactly what factors are working against your budget.

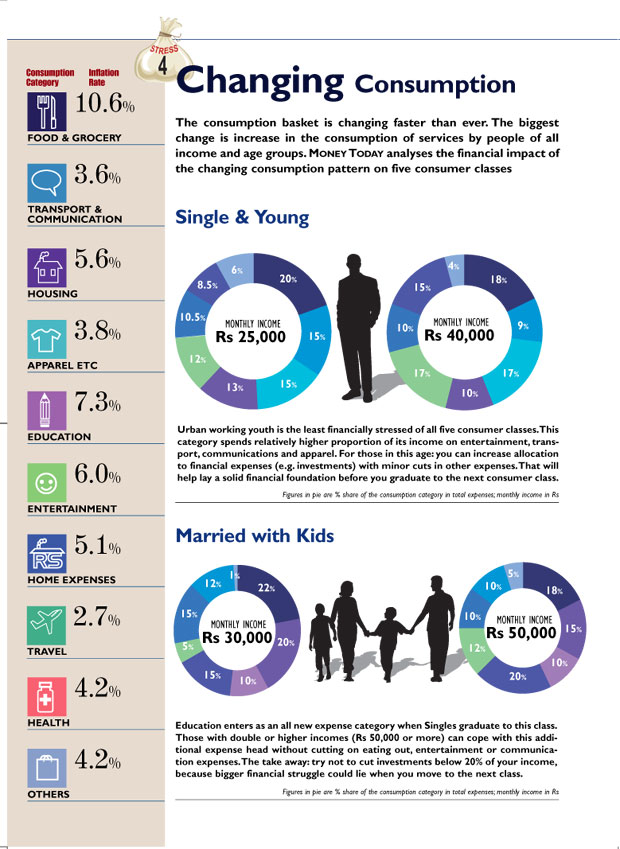

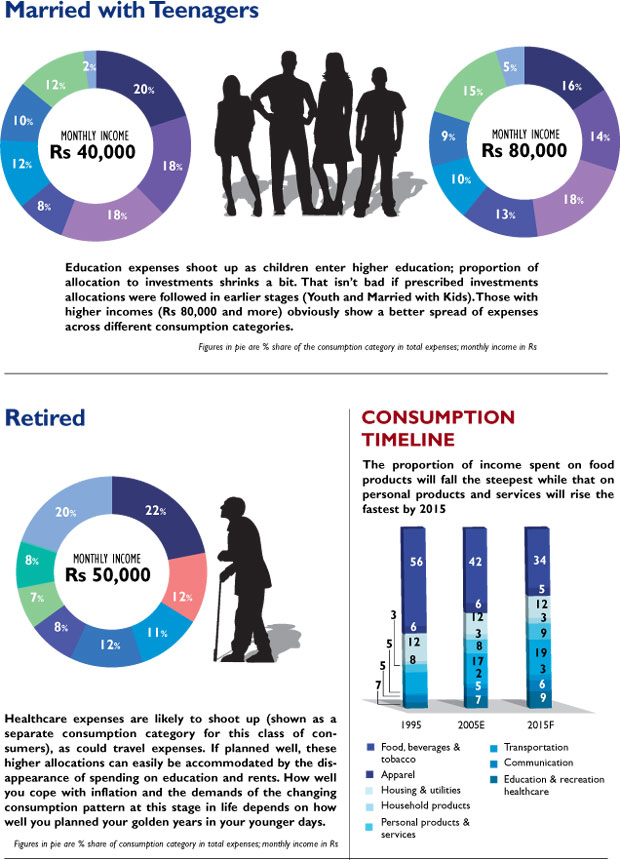

Every family has an exclusive consumption basket and the impact of inflation, interest rates and taxes vary according to the nature and proportion of expenses. Equally different are the nature of problems that can arise from the same stress points and their possible solutions.

The current version of inflation has busted many myths about the dimensions of the middle-class wallet. One being its capacity to absorb the rising prices of essentials such as fruits and vegetables. The budgeting blues of Kolkatabased Abhinandan Das — a student living with his parents — is a case in point.Five steps to intelligent expense planning |

| TRACK Start by putting down on paper your monthly expenditure under different heads. |

| ALLOCATE Next, allocate your expenses under different heads according to spending pattern. |

| MATCH Contain your expenses to match the allocation under the same heads. |

| REVIEW Examine allocation to heads with deficits or surpluses for more than three months. |

| CHANGE Spending and savings pattern may need tweaking if suggested by quarterly reviews. |

Das’ father had opted for voluntary retirement a few years back and the family’s income is fixed. This also means they are struggling to accommodate the recent spurt in prices of food products, household items and medical care. Says a disturbed Das: “Now we think twice before making the smallest of purchases, something we never had to do before.” The goings maybe tougher for his family but those with healthy salary increments are facing the heat too.

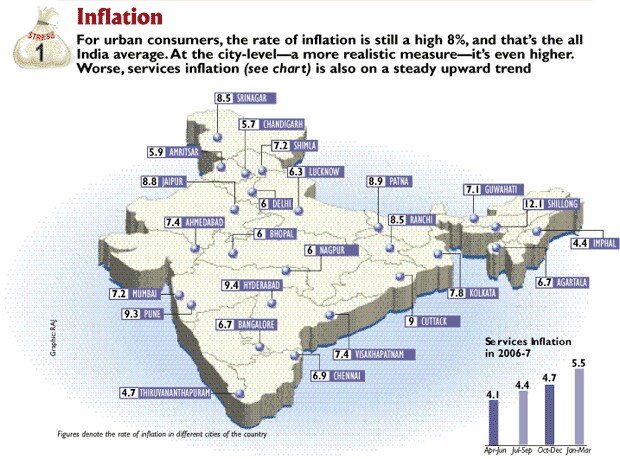

A senior manager with an MNC in Jamshedpur, Sanjay Prasad is doing quite well for himself. Nonetheless, he has drastically cut back expenditure to keep his finances on track. Weekly family outings have reduced to a monthly ritual. “Instead of going back home for lunch, I now carry tiffin to office to control fuel expenses,” he remarks. Indeed, inflation is no longer the malady of metros and Tier I cities alone. Tiny Shillong to chilly Srinagar are in the grip of price rise higher than the all-India average.

But packing the most powerful punch is services. The huge increase in consumption volumes combined with spiralling costs makes them a double whammy for your money. Worse, you probably never include this expense while computing your budget. Delhibased deputy manager, Amit Goyal, is not even aware that a service tax of 12% is the culprit behind his higher services’ bills.

Points to remember |

Not all deficits are bad and not all surpluses are good. |

You may stretch your finances to pay a home loan EMI. But it helps create an asset. |

A surplus in child’s education or family entertainment means you are not spending enough on crucial areas. |

Overspending under some heads may be a signal for corrective action. |

Quarterly reviews should differentiate between what is good and bad for household. |

Services inflation is a still lesser known devil. Who pays attention to a tame 5.5% when the wholesale price index (WPI) looks wolfish at the 7.7% mark? But the truth is that WPI is getting domesticated, climbing down by Y% in the past Z months. On the other hand, services inflation, though lower in value, has been consistently rising over the past Y months. And experts predict that the curve will only move upwards.

In addition to value, volume of service consumptions has also grown. In fact, consuming more services is one of the defining parameters of improved standards of living. So as you become more prosperous, cost of maintaining that prosperity rises alongside. Ironically, this is a point of no return. You would hardly wish to compromise on the prospects of moving up in life just because living will become dearer. Moreover, you are helpless in the face of these expenditures. Bhopal’s Madhuri Moghe agrees. A victim of the increasing addiction to mobile telephony, she rues, “Earlier we had only one landline connection. With three mobile phones in the house now, costs were bound to rise. But no matter how much we cut back on talking, there is no escaping the service tax menace.”

And she doesn’t once mention the possibility of doing away with one of the phones. Such is the extent of our dependence or addiction to the service. Reddy’s position is no different. With the arrival of low-budget airlines, he now prefers travelling by air for work or pleasure. As a result, his travel expenditure has increased in the past few years. He refuses to compromise on the convenience of efficient and faster connectivity though it comes with a heavy price tag and threatens to upset the household budget. Delhibased Charu and Mohit Gopal are beset with the queer problem too.

And she doesn’t once mention the possibility of doing away with one of the phones. Such is the extent of our dependence or addiction to the service. Reddy’s position is no different. With the arrival of low-budget airlines, he now prefers travelling by air for work or pleasure. As a result, his travel expenditure has increased in the past few years. He refuses to compromise on the convenience of efficient and faster connectivity though it comes with a heavy price tag and threatens to upset the household budget. Delhibased Charu and Mohit Gopal are beset with the queer problem too.

Living with Mohit’s parents now, the working couple will be moving out on their own soon. Multiple incomes had insulated them from feeling the heat on their budget. But as they tot up future living expenses, it is clear that services and rent will gobble up most of their earnings. “We will try to be careful, but there is little that can be done about it,” says Charu blandly. Not entirely correct, but we will come to that later.

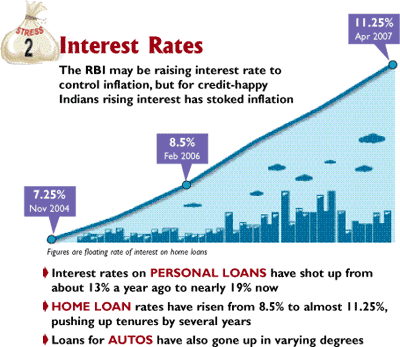

Integral to the change in consumption pattern is the emergence of the credit culture. Not only “what” we buy has changed but “how” we buy it has transformed. Affordability of a product is measured not by MRP but its EMI. Every second household is paying off a house, car or personal loan which accounts for about 25-30% of the total monthly expenses. All was hunky dory as long as interest rates flirted with the lows of 6-7%. But two years ago, rates started climbing up, giving loan takers the jitters. By the time they neared the double digit mark, many had already pressed the panic button. But all hell broke loose in family budgets when home loan rates kissed 13%, twice of where they stood even a year ago.

A couple of notches down today to 11.5-12%, the situation is hardly any better. Whether your budget can take the pressure or not, you have to pay up. If scraping together the inflated EMI seems impossible, the only other option is to extend the loan tenure by however long it takes to repay the outstanding amount. Given that budgets are already too stretched, pre-payment of loans is an option for very few.

To the contrary, some, like Ujjain’s Madhukar Kaushik, have been forced to take a new loan to fund the old one. Kaushik, a bank executive himself, had taken a home loan in 2000 at 8.5% for 15 years. Then came a second home loan, a personal loan and loans from some employee societies. His finances crumpled under the weight of high interest rates and in 2006, Kaushik was forced to take another personal loan in an attempt to tide over the rough times.

Be it Moghe, Reddy, Kaushik or Prasad, the spectre of high loan rates haunts almost every household. The result is nightmarish for some, while others are trying to scrimp their way through. Comments Dr Neel Kapoor from Bhopal: “Our home loan would have been over in January but has been extended by a year due to increased interest rates.

Obviously, this has upset all calculations and we are forced to cut corners to dole out these thousands for one more year.” For the Kapoors, the sky seems to have fallen through the roof. All stress factors are conniving to rock their finances. Service inflation has hit them through the cost of their daughters’ higher education.

Transport expenses have forced them to shift from petrol to an LPG powered car. Consumption of telephone services has jumped in the past years so that even though rates have fallen, their bills have become fatter. Where do the extra funds come from? “Savings,” answers Kapoor. “Our monthly savings have dipped by more than 60%. In addition, all investment plans have gone haywire. We were planning to invest in another property this year. That has been put on hold since those funds are now paying off the extra EMIs,” she says glumly.

In fact, investments have been brazenly compromised across all households suffering from an acute cash crunch. Moghe voices the same concerns, “We are saving nothing at all. Right now, the priority is to repay our home loan and fund our children’s education,” she says. Unable to save enough from his expenditure, Prasad defaulted on SIP payments for the last two months consecutively. Reddy has all but given up trying to put together the down payment for another housing loan. “Lack of funds has taken its toll on my retirement planning too,” he laments.

In fact, investments have been brazenly compromised across all households suffering from an acute cash crunch. Moghe voices the same concerns, “We are saving nothing at all. Right now, the priority is to repay our home loan and fund our children’s education,” she says. Unable to save enough from his expenditure, Prasad defaulted on SIP payments for the last two months consecutively. Reddy has all but given up trying to put together the down payment for another housing loan. “Lack of funds has taken its toll on my retirement planning too,” he laments.

By now you know what is squeezing your finances dry. Not that it is a happy revelation because there is precious little you can do to control service taxes, interest rates or inflation. So, is shortage of funds a reality of life you must learn to live with? No, definitely not. If they can’t do much about the villains in the script, the actors can be wiser. The trick is adhering to the fundamentals of finance management.

Track your expenses. Not in broad heads alone (though that is important to assess the big picture) but in minute details. How much is spent on snacking in office? How much on junk jewellery? You must have the answers to these questions. Then collate the expenses under various heads. This helps you determine whether your spending pattern is justified. These tips might seem too rudimentary to tackle your budget crisis.

But it would be a blunder to ignore them. Chandigarh-based senior media co-ordinator, Vijay Arora, stuck to these basics through the struggling years of his career and still managed to provide a comfortable lifestyle for his family. “We made elaborate budgets every month, down to the amount to be spent on buying gifts for friends and relatives. And we stuck to it,” he says simply. Of course there were temptations to overspend, but long-term goals helped him douse the desires. For instance, many a times, he felt compelled to buy a car.

“But I bought it only recently when I could fund the purchase without loans and save enough for petrol expenses too,” he explains. Hence, your household budget should provide not only for present but foreseen future expenditures too. And don’t forget to factor in inflation in the price of the product or service you are saving for. Future needs should be computed at future prices. You don’t need to be a financial wizard to be able to figure this out. It’s just simple math. Say, 10 years from now you plan to send your child abroad for higher studies. The current cost of the course is estimated at Rs 10 lakh. Add annual inflation of 5% to the same. Thus your savings must add up to around Rs 11 lakh after two years.

Remember, savings is deferred consumption. And the proportion you want to keep aside for this must be decided carefully. If you are a better investor, first decide what percentage of your income must constitute the investible surplus. Work backwards to arrive at the amount available for monthly expenses. In case you spend wisely, fix the expense limit first. The rest automatically forms the investible surplus of your income. But whatever method you follow, stick to the final division of your earning. Discipline is indispensable to intelligent financial planning. The moment you let go, your finances are vulnerable to all the predatory forces discussed in the story. It is only human to be careless.

But carelessness can be calamitous. Especially in times of plenitude. For urban India, these are times of plenty. It is easy to be reckless, spend more than you can afford and not save at all. But don’t be overwhelmed by your bulging pay packet. Ask yourself whether you are optimising on this opportunity. Are you planning for a secure future? Good times don’t last. Good decisions do. Be wise when you can. And stay wealthy for a lifetime.

— with Sudhir Gore