It's becoming common to blame the economy for most things. Delay in a housing project? Blame the slowdown. Credit card fraud? Peg it on the economy. No insurance? Of course, it's the economy. Job loss? The culprit is the slowdown. Can't afford a new computer? It's because of the downturn. Forgot the homework? Recession.

Actually it's more than a joke—the economic slowdown has hit every facet of our lives, including our investments and other financial products. The recent cut in credit limits for credit cardholders is a case in the point. The economy might have necessitated the cut, but it can hardly be blamed for the lack of communication to customers.

There are a number of other problems that seem to have cropped up for no rhyme or reason. Like banks refusing loans after having said yes, or realtors failing to pass on price cuts to earlier buyers. Fortunately, most of the issues that have come up in the past year or so have viable solutions.

We thought the time was right to look at these dilemmas in today's context and give you an idea about the possible ways in which you can resolve them. And because it's important to think long-term, we also consider ways in which you can ensure that such problems do not crop up in the future.

We take you through the problems in seven areas of personal finance and offer solutions. A common thread that runs through these solutions is your need to understand the product. As we have said often enough, an informed investor is an empowered investor.

Delay in delivery of the project | Project modified or shelved midway | Price cuts not passed on to existing buyers | Delay in refunds on cancellation of booking

The Way Out

The good news is that the law is on your side. According to lawyer Mantosh Sarkar, "In case of a delay, the buyer's right has been infringed and he has every right to claim compensation or come out of this agreement irrespective of any adverse clause." If the contract specifies a penalty in case of a delay beyond the stipulated time frame, investors have the option of invoking the signed contracts. The developer has to pay an interest on your deposit as agreed at the time of booking or refund your deposit. So, the first step is to speak to the developer.

If a standard complaint to the developer about a delay or denial of compensation does not work, you can take the matter to court. You can also take builders to court for high-handed and rough behaviour by their employees or for changing the project specifications during construction after taking deposits. "If you have a grievance against a builder, send a notice to him in writing. Do not worry if he refuses to accept your notice. The proof of sending is valid in the consumer court and the notice would be deemed to have been duly served," says Delhi-based consumer lawyer Rahul Bhatia.

You also have the option of approaching a consumer organisation with your problems and it can take up your cause against the builder. "Today, consumers have many avenues to lodge a complaint. We tell them not only where to complain but how to do so as well (what to tell the company or the court). If a consumer is being harassed, we tell him what to tell the person who is harassing him," says Sriram Khanna of Consumer VOICE.

If the problem is common to many buyers, you can use the power of the Internet to lobby for your rights. Even big real-estate developers have been forced to offer discounts and double the penalty offered for delays from Rs 5 to Rs 10 per sq ft because of sustained online campaigns. Approaching the local authorities can sometimes drive a real estate developer to be more proactive.

How To Avoid This In The Future

"While signing the agreement with the builder, ask him to spell out what is included in the force majeure clause, which can result in delays, and also the interest that you get on your deposit for delays," says Bhatia. It is also a good idea to look at the way the cost of property has been broken up because this is likely to have a bearing in case you seek refunds from the developer later; the greater the splits, the longer it will take to compensate.

"An important aspect to keep in mind is that the promise to deliver goods or services should be in writing—it can be a brochure or even a print-out of a Web page from the company's Website. This should be preserved because it will be your only proof to show what the company had promised," says Khanna.

Also, keep track of the progress of the project. "The trick is to be aware and keep visiting the project frequently to check the progress of the construction. If it is behind schedule and you post a comment on the Net, you will have a group by the time the project is officially delayed and this will offer a good bargain opportunity," says a member of an Internet group fighting for its rights against Parsvnath, a prominent developer.

Also, you should check that all the permissions required to start a project have been obtained, and that the developer has adequate finances to complete the project. Till the time a real estate regulator is put in place, buyers will have to rely on informal options like online forums, which are quicker and more viable than approaching a court of law.

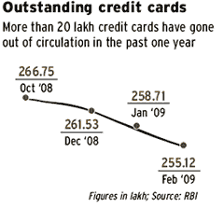

Cash withdrawal limit reduced or revoked | Credit limit reduced substantially | Card blocked for no transactions | Add-on cards closed without intimation

The Way Out

Your immediate response should be to approach the card issuer or bank. Insiders say that a threat to cancel the card (because the lower limits have an adverse effect on your credit history) is generally effective, as the bank is reluctant to lose a customer. If the reduction in cash or credit limits is because of delayed or irregular payments, ask for the billing schedule to be changed to meet your convenience. Of course, promise to meet all your future payment schedules. If the bank has cancelled or blocked the credit card due to non-use, provide an explanation if needed. If you are not happy with the response, file a complaint with the banking ombudsman.

How To Avoid This In The Future

In most cases where the limit is cut, it is because of a low average balance in the associated bank account, or because the payments have been irregular or late. Maintain a minimum balance in your account (ideally, more than what the bank stipulates) and schedule your payments. Pay on time, and in full every time. Avoid rolling over payments; ideally, get rid of all extra cards. Experts suggest that you limit yourself to three cards. If your card has been blocked, check if you have defaulted on your card payment, even if it was three months ago, as CIBIL updates its defaulters' list every quarter. So your name can appear on the list for up to 60 days after you've paid.

Loan cancelled even after approval | Increase in collateral for unsecured loans | Change in loan tenure without notice | Liquidation of mortgaged security | Rate cuts not applicable to existing borrowers

The Way Out

As numerous borrowers attest, threatening to move to a competing bank has the desired result. However, make sure you can carry this through in case the bank still does not give you better terms. Grievances over delays in sanction, disbursement or nonobservance of prescribed time schedule for disposal of applications, etc, can be taken to the banking ombudsman. If you want more general benefits (for instance, making new interest rates applicable to existing borrowers), try collective action through forums like Internet groups. No bank can afford negative publicity and will offer some concessions to avoid such a situation.

How To Avoid This In The Future

"People fail to do their homework before making a financial commitment. The cost of every service or product varies from one institution to another and comparing these before making a commitment will go a long way in preventing you from feeling cheated," says Sriram Khanna, project coordinator, National Consumer Helpline. Also, as a rule of thumb, never trust a sales agent. He might make tall promises, which the bank might not honour. Finally, check your credit history. A long-forgotten default might stand in the way of a home loan.

Inability to get NOC from distributor or AMC | Know your customer norms not simplified | Variable load structures mooted

The Way Out

You need a no-objection certificate from the distributor if you want direct control over your investment (and save on trailing commission). "Although you can consolidate your folios of units bought from two or more distributors, you need an NOC from the original broker if you want to stop the commissions that he earns on your initial investment," says Suresh Sadagopan, a Mumbai-based financial planner.

Distributors generally delay, but cannot deny this certificate. Your best option is to threaten to redeem your holdings. For other complaints not related to the distributor, approach the mutual fund's grievance redressal cell. The name of the contact person whom you can approach in case of complaints is mentioned in the offer document of the mutual fund scheme. Similarly, the names of the directors and trustees who monitor the activities of the mutual fund are mentioned in the offer document. If your complaints remain unresolved, your next option is to seek redressal from Sebi. Send a written complaint to the regulator; on receipt of the complaint, Sebi will take up the matter with the concerned mutual fund.

How To Avoid This In The Future

You can avoid several potential fee-related problems simply by avoiding intermediaries. Opt for direct investment rather than haggling over the variable load structure (when it is introduced).

Most problems for mutual fund investors arise because they fail to go through the offer document before investing. Most investors seem to have blind faith in the broker or agent's recommendation. Some go back and look at the document only when the fund's returns start falling, realising too late in the day that the mandate of the fund is different from their requirement. So make sure you read the offer document carefully before investing.

Also, if your broker (or financial adviser) recommends a specific fund, ask him to list all commissions, incentives or cash payments he stands to gain from this. You have a right to know when he is not acting in your best interests.

Margin calls high, margin limits down | Brokers sell shares without prior notice | Shares pledged by promoters not disclosed | Incorrect promoter holdings filed

The Way Out

If the problem is related to the broker, your first step should be to complain to the brokerage, although most complaints go unheeded. Once you have officially registered a complaint, forward it to Sebi's grievance cell. If the problem is with the company, approach its compliance officer who is supposed to look into investor grievances. If the company fails to provide redressal, approach the stock exchange on which it is registered. The registrar of companies can help in case of unlisted companies. In cases of cheating, file a criminal complaint against the brokerage with the Economic Offences Wing of the police. Also consider approaching investor action groups; the Ministry of Corporate Affairs provides a list of such groups on its site.

How To Avoid This In The Future

Trade only through registered and reputed brokerage houses and don't allow anyone to trade on your behalf. Read the terms and conditions carefully before signing on with a broker. Make sure you read all the communication from companies and also track them in the media. Understand the market and the strategy you choose. If you want to make a quick buck by dabbling in the futures & options market, make sure you know how much you can lose and what the risks are when you leverage.

Denial of medical insurance claims | Refusal to restructure policies

The Way Out

If a medical claim has been refused and no convincing reason given by the third-party administrator, write to the insurance company within 15 days of the refusal, with copies of the claim and supporting documents (from the hospital). If you do not get a response from the insurance company within a month, take the case to the insurance ombudsman. The decision of the ombudsman is binding on the insurer; you can take the case to court if you are dissatisfied with the decision. File a case in the consumer court. "In the past five years we have developed the law in the insurance industry the most. Companies have been exploiting consumers on the basis of exclusion clauses that are never explained to the consumer. A string of judgements in favour of consumers has brought out important aspects on the basis of which these companies can't deny a claim based on exclusion clauses," says Justice M.B. Shah, former president, National Consumer Disputes Redressal Commission.

How To Avoid This In The Future

"Ulips combine investments and life insurance in a single product," says Bert Paterson, former managing director, Aviva India Life Insurance Company. This is where they differ from traditional life insurance products (see table). Traditional plans have never offered policyholders the kind of choice and flexibility of investments that Ulips give. Unlike Ulips, which allow you to choose a fund option depending on your risk appetite and return expectation, traditional insurance plans invest mostly in debt. So even if the policyholder has a higher risk appetite, he will be saddled with a low-risk investment that earns low returns.

With Ulips, you can choose the extent of life cover and investment you want. Instead of fixing the extent of cover, it looks at the annual premium that one can pay and works on the minimum sum assured based on this value. A part of the premium is invested in a fund, while the rest serves as the insurance premium. So, Ulips offer investors what no traditional policy does: information about how the policy works.

Receiving notices even when tax is paid | Dealing with complicated forms

The Way Out

More often than not, problems with the Income Tax Department are caused by the department's systems, which are known to be archaic. However, it is up to the taxpayer (assisted by chartered accountants) to take remedial action.

If you get a notice or realise that you are being harassed for no reason, your first step should be to send the department written clarification. Along with this, include copies of income proof such as Form 16 or 16A, TDS certificates issued by the employer (in case of salaried individuals) or by banks or post office (in case of tax deducted on investments).

If the problem is caused because of an assessing officer, you can appeal to the deputy commissioner (appeals) or commissioner (appeals). If that fails, you can take up the matter with the Income Tax Appellate Tribunal. If this too doesn't work, you can go up to a high court, and finally, even to the Supreme Court.

How To Avoid This In The Future

In general, the Income Tax Department sends a notice to the taxpayer when it cannot verify a claim. To avoid this, ensure that you have documentary proof for every step, even though the new forms and systems do not require you to append them with the return. In case of a notice, having the paperwork in order will ensure that you can send the required documents to the department within the stipulated 30-day time limit.

One of the most common problems happens when the tax department does not take into account the tax deducted at source. In fact, for the assessment year 2007-8, the problem was so rampant that the members of the Institute of Chartered Accountants' of India (ICAI) have written to the chief commissioners of income tax in various cities, stating that the mistake could lead to harassment of taxpayers. On its part, the Central Board of Direct Taxes has instructed income-tax officers to process returns where the TDS is up to Rs 5 lakh and the refund is below Rs 25,000 without verifying the details.