»1. One Pound Sterling. Or just about US $1.41. Which is less than Rs 100.

That's the price at which Tata Steel sold off its Scunthorpe steel plant, its mills in Teesside and Northern France, an engineering workshop in Workington, a design consultancy in York, and a bulk terminal and associated distribution facilities to Greybull Capital. These assets represented its loss-making long products division, employing 4,400 people. It represented roughly one-fourth of the Tata Steel UK business - the erstwhile Corus Plc - which the group had picked up after a bruising bidding war in 2007 for $12 billion (Rs 53,000 crore then).

Apart from the token amount, Greybull Capital - a private investment firm - will also take over 'relevant liabilities', mostly working capital-related. Analysts say there is no transfer of debt, implying that parent Tata Steel's debt continues to be high. Tata Steel will also have to bear pension liabilities of the divsion worth »90 million ($127 million) for 2016-18. Greybull plans a package of »400 million ($564 million) from banks and its shareholders for working capital and future investments.

Meanwhile, over the past eight years, the Tatas have already written off around »2 billion ($2.8 billion at today's exchange rate) goodwill impairment from the books, apart from investing a fresh »1.7 billion ($2.4 billion) to modernise the plants of its British buy. The Tatas tried everything to make their trophy acquisition work - idling blast furnaces, cutting jobs and selling assets (see A Rollercoaster Ride).

In the end, nothing worked, and Chairman Cyrus Mistry finally decided to pull the plug. He didn't have much choice - Tata Steel UK was reportedly losing $1 million (Rs 6.65 crore) a day in 2016, and losses were accumulating faster than the profitable Indian operations could clear them.

The distress sale is a dream turned sour for the group that made India's biggest overseas acquisition - and Britain's biggest inbound FDI - at the peak of the commodities supercycle. The price of hot-rolled coil was $550 per tonne as against $340 today. In 2008, it had even touched $1,000. The Corus acquisition had propelled Tata Steel from the world's 56th largest steel maker to sixth. (At the time of going to press, Tata Group did not provide answers to an emailed questionnaire or access to Tata Steel's CEO and group CFO for this story.)

But erstwhile chairman Ratan Tata's huge bet that good times would continue for some time in the steel industry has haunted the group. Between 2004 and 2008, as the global economy boomed, Indian business houses went on an expansion spree - building capacities at home and acquiring them abroad. The Tata Group embarked on the biggest shopping expedition globally undertaken by any Indian group. It acquired 20 major companies shelling out around $20 billion (Rs 1,33,000 crore today). The Corus purchase was initially supposed to cost the group only $7.6 billion (Rs 33,561 crore then) until Brazilian steel maker Companhia Siderurgica Nacional (CSN) made a counter offer to the Corus board. The bidding war that followed finally saw Tata Steel pick up Corus - but paying a 58 per cent higher price -- from $7.6 billion to $12 billion.

Worse, a commodities crash followed in 2008/09, right after the acquisition. Tata Steel Europe's operations could neither justify nor service the huge acquisition cost. Corus, which reported a topline of $18 billion (Rs 79,488 crore then) and a pre-tax net profit of $1 billion (Rs 4,416 crore then) at the time of the acquisition, reported a net loss of Rs 6,724 crore ($1.08 billion) in fiscal 2015. It delivered a profit only once in the nine years it has been managed by the Tata Group.

Some within the Group had worried that it was paying too high a price. After the euphoria of the bidding war settled, senior executives in Jamshedpur and Bombay House expressed their discomfort with the price and terms behind closed doors.

But the cheerleaders were far more. Then managing director B. Muthuraman countered the naysayers, pointing out that the Arcelor-Mittal deal in which London-based L.N. Mittal acquired the second largest steel maker Arcelor for $33.6 billion (Rs 1,55,702 crore in June 2006) to create a behemoth of 114 million tonnes was a much bigger deal. Muthuraman was convinced that there would be strong demand for steel for many years because of the growth in India and China. The prevailing view among the bulls in the global steel industry was that steel demand would continue rising exponentially because of Chinese demand and that of other BRIC countries, and also the boom in Europe and the US. There was also a theory floated that globally the steel industry would be dominated by a handful of companies with capacities across the world. Arcelor-Mittal, ThyssenKrupp, Posco were the names in the big league - with the Corus purchase, Tata Steel jumped into the exalted league.

The bulls turned out to be horribly wrong, picking up expensive capacity just when the global demand for steel had peaked. Practically all big global steel majors are still living with the consequences of their deals. The crash of steel demand and prices since 2008-end has halved the revenues of the world's largest steel maker ArcelorMittal to $63.58 billion (Rs 4,20,900 crore), with a loss of $7.94 billion (Rs 52,404 crore) in 2015. The world's second largest, Nippon Steel & Sumitomo Metal Corp's profit fell 11.7 per cent despite the flat revenues in the last financial year. This isn't exactly how it was envisaged, though.

The Tata Push

This time of the year nearly a decade ago, the board of Tata Sons relaxed the retirement age of directors by five years, enabling Ratan Tata to helm the group for another five years. Tata had embarked on a global expansion spree, with the objective of bringing in 50 per cent of the Groups revenues and profits from outside India. Europe's largest steel maker Corus Plc was an obvious choice.

Tata's personal bonding with the Corus board members, especially with chairman Jim Leng and managing director Philippe Varin, helped in striking the deal (Tata Steel had engaged with Corus since 1992 at its Ijmuiden operations in coke making and blast furnace facilities improvement). Ratan Tata intended to derisk the Indian business between high-growth emerging markets and price-stable developed markets. He wanted to transfer technology from Europe to India to develop new products and capture growth in Asia, in addition to many other synergies leading to an annual saving of $450 million.

Just when the stage was set for the perfect marriage, in walked the villain: Brazilian Companhia Siderurgica Nacional (CSN). It bowled over the Corus board with a counter offer. Tata's lieutenants - Muthuraman, Tata Sons' acquisition expert Arunkumar Gandhi and UK-based Managing Director of Tata Limited Syed Anwar Hasan - countered the Brazilian offer. At last, on January 31, 2007, in a seven-and-a-half-hour long electronic auction conducted by the UK Takeover Panel, Tatas defeated the Brazilians. It was a moment of fulfilment for Tata to acquire a company four times its own size. Addressing the media in Mumbai the next day, Ratan Tata paraded the CEOs from the century-old conglomerate.

Over the years, it turned out to be a white elephant. According to ballpark estimates, the company suffered Rs 18,800 crore impairment charges, Rs 14,700 crore in accumulated losses at Tata Steel UK from 2010-11; and around Rs 5,000 crore in failed capital infusion (in UK) to turn around the company. These add up to Rs 38,500 crore. Besides, the Indian parent, Tata Steel, paid around Rs 28,800 crore as net finance charges all these years since acquisition. One major part in it would be the interest paid for the $8-billion loan it took to fund Corus. Tatas infused $4.1 billion as equity for the purchase, raising fund through rights issue and foreign equity offering, money that could have been used as capex in expanding Tata Steel's own facilities in India manifold. Tatas still need to pay back the principal. It restructured and refinanced the loans on the way to extend the repayments. The profit of Tata Steel's India operation was almost flat at above Rs 6,000 crore in the past five years, despite the crash of the steel industry. The joker in the pack is the enormous pension liabilities. Read about that later in the story.

Tata Steel has a consolidated gross debt of Rs 85,168 crore as on December 2015. In the previous financial year, the company repaid $1 billion (Rs 6,230 crore). The company said after the third quarter result that it refinanced offshore debt of $1.5 billion (Rs 9,930 crore), further lengthening the maturity and reducing costs.

Ailing Giant Mills

Port Talbot is not just a panoramic coastal town in Wales; it is also one of the most polluted places in the region. Largely because of its only industry - a steel mill spread over 2,000 acres. The integrated plant has 4,104 workers, providing jobs to 10 per cent of the local population. Another such facility in Scunthorpe has 3,381 workers. Rotherham, which employs 1,276, is the third steelmaking site of Tata Steel UK. It has another 10 rolling mills and coating lines spread over the UK. Overall 15,000 workers are directly employed with Tatas and 25,000 indirectly.

Strip products are manufactured at Port Talbot and long products at Scunthorpe. But after the downward spiral, the company wants to focus on strip products. Tata has been trying to sell the long products business, which makes railway tracks and steel used in construction, amid a supply glut and tumbling prices. "There is no prescription towards divestment, and we will make the most appropriate strategic calls in each business on a case by case basis. We reiterate our focus is sustainable, profitable growth," says a Tata Steel spokesperson.

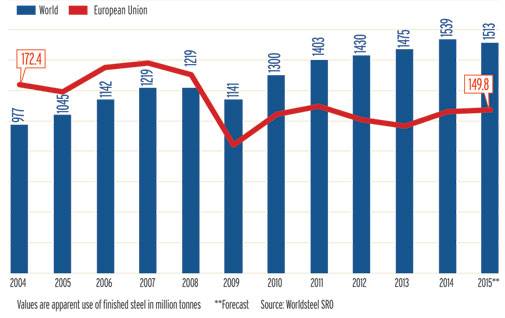

The supply glut and low prices triggered by Chinese dumping of steel strained the financials of Tata Steel UK. Last fiscal its revenue fell 14 per cent to Rs 38,841 crore. Average revenue per tonne decreased by 6 per cent because of downward selling pressure and a 1 per cent decrease in steel deliveries. Steel production fell to 8.2 mt compared to 8.5 mt in the previous year.

After the fall of Lehman Brothers in the US, Europe witnessed multiple financial crises and fall in demand. In parallel, China flooded the markets with cheap steel, thanks to its low wages and electricity charges. European steelmakers have additional charges like environmental management costs. For Tata Steel UK, the high debt burden and interest payments were putting pressure on the bottom line. Delayed modernisation of steel mills and strong Sterling Pound also hit the company.

Analysts say Tata Steel has about $4 billion (Rs 26,600 crore) of debt on its UK subsidiary's balance sheet. JP Morgan thinks the Greybull deal could reduce Tata Steels loss-making exposure. According to the firm, Tata Steels reported EBITDA should improve by $150-250 million (Rs 998-1,662 crore) as these assets were loss-making, and now sustainable reported earnings should be higher.

The Sale Price Conundrum

If one-fourth of its operations could fetch barely »1, what must Tata Steel expect from the sale of the remaining assets of Tata Steel UK? Alessandro Abate, a London-based analyst at Berenberg Bank, says that on the back of similar cases, the non-performing assets are usually sold at symbolic value. "It will be difficult to find a buyer for steel assets in the current market environment," Seth Rosenfeld, a London-based European steel analyst at Jefferies International, told media.

Javid also held talks with Sanjeev Gupta, the promoter of Liberty House who has expressed interested in buying Tata Steel UK, about a potential rescue deal for Tata's UK sites. Gupta's plan of revival involves replacing blast furnaces at Port Talbot with electric arc furnaces that process scrap steel. But it will take years and massive costs. Tata insiders don't believe the plan is workable. The government and unions have indicated they would like to preserve the blast furnaces at Port Talbot, which make raw steel.

On the sidelines of announcing the H1 financials in November, the former CEO of Tata Steel Europe, Karl-Ulrich Khler, who quit in February after serving five years at the top, told BT that the UK government ignored the company's requests to protect it against Chinese dumping. Khler recently attended a protest where steelworkers from across Europe marched to EU's Brussels headquarters, demanding higher import duties against steel dumping. The Tata Group, which is the largest investor in the UK, expected greater intervention from the UK government. Indian Hotels is one of the earliest Indian investors in the UK, acquiring interests in the St. James' Court Hotel in 1980s. Tata Tea spent $450 million (Rs 1,958 crore then) for Tetley in 2000. Tata Chemicals acquired soda ash maker Brunner Mond for Rs 508 crore (in 2006) and British Salt for Rs 650 crore (2011). In 2008, Tata Motors acquired the British marquee car brands Jaguar and Land Rover for $2.3 billion (Rs 9,190 crore in March 2008). TCS has a UK workforce of more than 11,000 employees in 30 locations. It delivers digital projects to more than 150 companies, including BT, Diageo, National Grid, NEST, Marks & Spencer and Virgin Atlantic.

"Chinese exports are being sold below the cost price. While France, Germany and Sweden took steps to protect their steel sector from Chinese attack without imposing tariffs, the UK government was laidback," says an analyst with Barclays. Power tariff in Germany and Spain is two-thirds of the UK. In France and Finland, it is almost half, according to Eurostat. The UK's wholesale gas price is more than three times that of the US Henry Hub.

Analysts believe that Chancellor of Exchequer George Osborne was keen not to offend Beijing by imposing anti-dumping duties in the long-term interest of attracting Chinese investment in Britain. Cheap Chinese steel imports into Britain forced Tata Steel to halve prices on some of its products to remain competitive.

The steel supply glut casts a shadow over steelmakers across the world. ArcelorMittal, the world's largest steel company, stumbled to a loss of $7.94 billion in the previous financial year. Its sales of $63.6 billion represents a 19.8 per cent decrease, primarily due to lower steel selling prices, which were down 19.7 per cent. Steel is cheaper than at any time in the past decade. The rise of incentivised Chinese steelmakers Hebei Steel Group, Baosteel Group, Shagang Group, Ansteel Group, Wuhan Steel Group and Shougang Group toppled the high cost producers in other geographies. Posco, South Korea's largest steelmaker, swung to a net loss of $79.4 million in 2015 amid weak demand and losses from its equity in affiliates. This despite the fact that it uses advanced technology and produces a large proportion of high-end steel. Analysts predict there are chances of many companies being forced out of business. In Japan, the world's second-biggest producer of steel, the large companies such as Nippon Steel & Sumitomo Metal and JFE Holdings have seen their profit margins shrink because of imports. The effect has less impact due to weaker Yen and cost cutting. The companies that are most exposed to the Chinese threat are big spot market players like ArcelorMittal and SSAB of Sweden. Lakshmi Mittal, Chairman and CEO, ArcelorMittal

Lakshmi Mittal, Chairman and CEO, ArcelorMittal

The strength of the scheme rests in sound investment of its funds. Without investment income, there would be no funds available to pay pensions. If there is a shortfall in the investment return, it is the responsibility of Tata Steel UK Holdings to bridge the deficit as it controls the trust through the appointments.

By last March, Tata already pared the deficit in the steel pension scheme from »2 billion ($2.97 billion then) to »485 million ($720 million) and has agreed with the trustees to eliminate the shortfall entirely by 2026, according to reports. On account of low interest rates in the UK, the scheme's liabilities increased significantly since the last actuarial valuation in 2011, leading to increased funding deficit.

But a change in ownership could require a major contribution to satisfy the UK pension regulators that savers would be safeguarded. According to pension experts in London, Tatas could sell its pension liabilities to a specialist insurer for »2 billion ($2.82 billion now) or agree to keep funding the scheme till its members expired.

A report in a UK newspaper says Tatas are understood to be in negotiations with the government and pensions regulator over putting the scheme into the Pension Protection Fund (PPF), which would mean workers suffering cuts to retirement savings of as much as 20 per cent. Company sources confirm that it does not plan to continue supporting the pension fund once it has quit the UK business, according to the report.

The Threat to the Parent

The Rs 1,39,503-crore ($20.9-billion) Tata Steel is the flagship of the $108-billion (Rs 7,18,200 crore) Tata Group. Set up in 1907, Tata Steel prides itself in being one of the worlds lowest cost steel producers. According to Muthuraman, the Indian business produced steel at $160 (Rs 7,100) and Corus at $540 (Rs 23,900) a tonne in 2006. The acquisition was a misadventure that had now begun threatening the existence of the parent itself.

Tata Steel's negotiations with Corus were based on these numbers. The global economy was resilient in 2005 despite the significant increase in oil prices driven by strong demand and uncertainty of supply. China and the US continued to lead the expansion in the global economy. In Corus' core EU markets, the growth was subdued.

Was the deal too expensive? Abate of Berenberg says: "The acquisition took place in a very bullish period with little visibility on what could have happened in Q3'2008 when the global financial crises exploded, dramatically hitting the global economy."

It was celebration time after the result of 2007/08, when first full year numbers of Corus were added to Tata Steel. The consolidated profit was up three times to Rs 12,350 crore and revenue shot up 415 per cent to Rs 1,31,534 crore. The board recommended 160 per cent dividend. In the year, higher demand led to better price realisation, though steel producers were hit hard by spike in coal and iron ore prices. The cheer for the business in UK ended there. Except a marginal profit registered in 2010/11, the business made alarming losses in all the years until now.

Where does that take Tata Steel from here? The group refused to provide access to company and group CEOs for any visibility on that front. Meanwhile, in 2014, Tata Group announced a $35-billion capital investment programme over three years, which included the Kalinganagar steel plant, investments in creating capacities in the defence production, investments in an omni-channel marketplace, a digital health and wellness platform, and a Big Data analytics initiative, besides unveiling of over two dozen new vehicles by Jaguar-Land Rover and Tata Motors.

With the Tatas now determined to find a lasting solution to Corus, it can only play a painful waiting game while negotiations take their course. But whether it sells or shuts Tata Steel UK, it will have to deal with the ignominy of slipping back to the rank of around 20 among the world's largest steel makers. Only, it will take heart from a healthier and profitable balance sheet.