In a globalised economic system, no country can escape the general drift of the market. The slump in real estate is not confined to India or the US. Other markets such as Australia, South-east Asia, West Asia and Europe are also affected. The only difference is the degree of the decline. In some markets such as Malaysia and Dubai, while real estate prices have slumped, opportunities have emerged for buyers.

If you have always dreamed of a holiday home overlooking a beach in Mauritius or a farm in Australia or even a villa in Spain, the current scenario may enable you to realise it.

Adding to the attractiveness of some of these locations are the measures these countries are taking to attract foreign investors. While Dubai has allowed freehold property purchase by foreigners, entitling them to full ownership and resale rights, Mauritius allows property owners work permits and Malaysia gives a 10-year visa without working rights. Singapore has a property free zone for foreigners. “The majority of Indian buyers in Dubai are expats who have established themselves in the UAE and are either looking for a home for their families or for long-term investments,” says Peter Riddoch, CEO, DAMAC Properties, a Dubaibased developer.

But though the RBI has allowed Indian residents to buy property abroad, this is not a market for everyone. Only if you are frequently travelling abroad and have sufficient surplus cash should you venture into overseas real estate.

Also, figure out what is the purpose of the investment. Do you intend to use the property or are you going to be an absentee landlord? “Indians are buying property abroad for very specific reasons. For example, there are lots of Indian students in Australia, so Indians would like to invest in property there for their children,” says Poonam Mahtani of Colliers International. You should know the risks and the terms clearly because it is not easy to quickly get out of an overseas market.

First, gather information on the potential destinations and go through the rules on foreign ownership. “Indians intending to invest in property abroad must be aware of certain investment and liability risks they expose themselves to,” says Anuj Puri of Jones Lang Lasalle Meghraj.

While one has to account for the risks that are inherent to realty assets and to the changing interest rates, there is also an additional foreign exchange risk. If the rupee appreciates, your returns are lower. Also, keep in mind that ownership does not necessarily mean visa or work rights.

Buying property overseas is a complicated procedure and requires expert guidance. True, foreign real estate markets are more stable and organised than those in India. But the foreigner tag adds complexity to the deal. Thankfully, in many established markets, foreigners have access to property management services. Once you have decided on a specific location, hire a licensed real estate agent who can guide you through the process. This small expense can help you avoid costly mistakes.

Under the RBI’s remittance scheme, a resident Indian can invest up to $200,000 a year abroad. If this sounds small, several members of a family can pool their limits to create a larger corpus. You need to pay the entire sum upfront because few lenders are willing to give loans to foreigners.

Some banks like HSBC give loans against a property in India, which can be transferred to an account in designated countries for buying a property there. The interest rates on such loans are between 14% and 16%.

The income from the property— whether as rental or as capital gains when it is sold—will be subject to the tax laws of the country where you are investing. But if India has not signed a double tax avoidance treaty with that country, it will also be taxed in India. So be sure of what you are getting into before you jump in.

Narinder Kapur and Ira Mehra own a 5,825 sq ft penthouse in Thomson 800 area of Singapore.

They bought the apartment for S$3 million in 2006. “The decision was a mix of investment and personal living,” says Kapur. “There is a pent up demand for bigger apartments and the location is close to the city but less crowded.”

[1 SGD = Rs 32.38]

15%price appreciation in the past two years

Why Invest: Commercial hub, cosmopolitan culture, significant expat population

What to look for

Restrictions:

• Approval from Land Authority needed for buying land, landed property or flats in buildings of less than 6 storeys

• Foreigners not allowed to purchase Housing Board flats

Taxes / Additional charges:

• Stamp Duty payable on purchase

• Property tax every year on 10% of assessed value

Visit / Stay: Social visit visa valid for 5 weeks, allows multiple entries and 30 days stay per visit

For more information: www.iras.gov.sg, www.sla.gov.sg

K. Gunasegaran bought a house near Kuala Lumpur last year for US$80,000.

“The cost of living here is much cheaper than many countries, and property is not as expensive as in India,” he says. He wanted a house that was close to his workplace and also to schools and colleges. He made sure that he had cash in hand and had no need to get a bank loan. “I only needed to get the central bank’s approval and it took about three to four months,” he says.

[ 1 MYR = Rs 13.46 ]

20%appreciation in price in the past two years

Why invest: Easily accessible, property rates comparable to India

How to invest: Apply under Malaysia ‘My Second Home’ programme

What to look for

Restrictions:

• Minimum value of the property should be MYR 250,000 (Rs 33.65 lakh)

• Foreigners not permitted to sell property within 3 years of purchase

• In case of sale, government permission needed if buyer is not a local resident

Taxes / Additional charges:

• Tax of 30% of the gain charged if property is sold within 5 years of purchase

• Stamp duty payable on every transfer of the property deed

• Legal fees of up to 4% and agent fees of up to 3% of the purchase price

Visit / Stay: Foreigners get social visit pass for 10 years if they apply through Malaysia ‘My Second Home’ programme. This can be extended after 10 years

For more information: M2H - www.mm2h.motour.gov.my: Foreign Investment Committee - www.epu.jpm.my

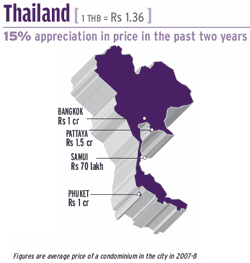

Robby Virk is helping his father to buy a property at Thailand’s Pattaya beach.

Virk’s main reason for choosing Thailand was that prices were 20% lower than some European locations like Portugal and Spain. “It also has a better climate, warmer people and is an excellent tourist destination,” he explains. His father plans to spend holidays in Thailand; it will be the family’s third home as they already own properties in India and Canada.

[1 THB = Rs 1.36]

15%appreciation in price in the past two years

Why Invest: Buoyant tourism, low cost of living, options of seaside properties

What to look for

Restrictions:

• Foreigners can’t own land

• Minimum monthly income of 65,000 baht needed if applying for retirement visa

• Not more than 49% of condominiums in a project can be owned by foreigners

Taxes / Additional charges:

• 1-3% tax if property sold within 5 years

• Stamp duty of 0.5% and 2% transfer fee

• Agents’ fees come to around 3%

Visit / Stay: Visa-on-arrival facility for Indians, retirement visas for foreigners over 50 years old

Contacts: Board of Investment (www.boi.go.th)

Nirmal Baid, a US-based software developer bought a property in Calgary for $300,000.

“I liked Calgary for its sylvan surroundings. I plan to use the place for holidays and also let my friends stay there when they are traveling through Calgary,” he says. Baid thinks the community and neighbourhood are important factor to consider when buying in Canada. “There are pockets where Indians are dominant and that can be encouraging for those who wish to be close to their roots.” He bought the property in early 2007 when prices in Canada had weakened.

[1 CAD = Rs 44.57]

12% appreciation in price in the past two years

Why Invest: Significant expat population, proximity to the US market, prices lower and more stable than in the US

What to look for

Restrictions: Foreigners can stay for no more than six months in a year

Taxes / Additional charges:

• Land transfer tax of 0.5% to 2% depending on the state

• legal fee between 0.5 to 1% paid by the buyer

• Annual property tax of 0.5-2.5% on market value

• 25% non-resident tax to be paid on rental income

Visit / Stay: Foreigners need tourist visa, which can be extended after 6 months

Contacts: Real estate agents like www.remax.ca/ or Canada Real Estate Association for brokers - www.crea.ca

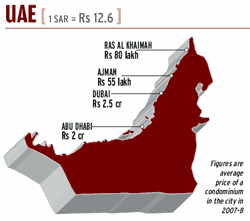

[1 SAR = Rs 12.6]

25% price appreciation in the past two years

Why Invest: No income tax, attractive shopping and business destination, high living standard

What to look for

Restrictions: Foreigners can buy only in designated ‘freehold’ areas

Taxes / Additional charges: 1 .5% land registry fee, payable on completion

Citizenship / Visit / Stay: Visas valid for 60 days and, for a fee, may be renewed once for an additional 30 days

For more information: Agents like www.bhomes.com; Developers like Al Nakheel, Emaar and DAMAC

[ 1 GBP = Rs 84.81 ]

3-5%appreciation in price in the past two years

Why Invest: Significant Indian population, no restrictions in buying property, important business centre, snob value

What to look for

Restrictions: No restrictions on foreigners buying property

Taxes / Additional charges:

• Capital gains tax of 18% on the gain is liable upon sale

• If the property is let as an investment income tax will be due

• Stamp duty, land tax, land registry fee to be paid at the time of purchase

Visit / Stay: Worker’s visa or a tourist visa needed

Contacts: Estate agents like Savills (www.savills.co.uk)

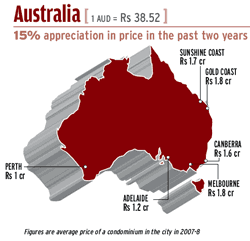

[1 AUD = Rs 38.52]

15%appreciation in price in the past two years

Why Invest: Foreigners account for 4,000 out of around 5,00,000 residential sales in Australia each year

How to invest: Buy ‘off-plan’ property for which developer has prior government permission to sell to foreigners. The property can be booked by paying just 10% of the cost and the rest of the money can be paid when construction is complete and the property registered

What to look for

Restrictions:

• Foreigners can invest only in newly built property

• Foreign owners can only sell to local residents

• Construction on vacant plots should start within 12 months

Taxes / Additional charges:

• Around 5% of the purchase price needed to cover fees

• Body corporate fee needs to be paid regularly

Citizenship / Visit / Stay:

• Residence, temporary residence, migration or visitor visas for foreigners

• Investor Retirement Visa allows people over the age of 55 to stay for up to 4 years by investing over $500,000

Contacts: Foreign Investment Review Borad (www.firb.gov.au) Brokerage houses like www.propertyshowrooms.com

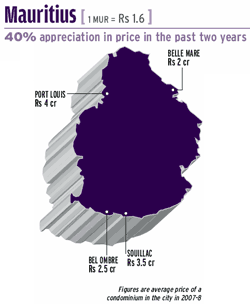

[1 MUR = Rs 1.6]

40% appreciation in price in the past two years

Why Invest: Scenic locations, accessibility, no capital gains tax

How to invest: Under government’s Integrated Resort Scheme luxury villas along the coast sold to foreigners

What to look for

Restrictions:

• Integrated Resort Scheme requires a minimum investment of $500,000

• Land size in a villa cannot exceed 1.25 arpents (0.5276 hectares)

Taxes / Additional charges:

• Rental income earned by nonresidents taxed at 15%

• Property tax levied at MUR30 per sq m for apartments

Visit / Stay: Foreign buyers and family get 'residentship status' till they hold on to the property

For more information: Board of Investment: investmauritius.com General information: www.gov.mu