Bengaluru-based pixxel Space is a rarity in India’s $13 billion spacetech industry. For one thing, Pixxel has received investor funding in a testament to the potential of the company. It was picked by National Aeronautics and Space Administration (NASA) in 2024 to provide earth observation data on climate change, biodiversity and agriculture to its $476 million Commercial SmallSat Data Acquisition (CSDA) Program.

The company, founded in 2019 by Awais Ahmed and Kshitij Khandelwal, is also one of the few to actually earn revenue from its business. Chief Executive Officer Ahmed, who has a master’s degree in mathematics from BITS Pilani, says Pixxel is still an infant when it comes to commercialising operations.

“The true yardstick of a successful spacetech ecosystem is the revenue it generates and how quickly it can achieve profitability, even while continuing to invest in research & development. By that measure, we are still at a very early stage,” Ahmed, 25, says.

His description of Pixxel, which builds high-resolution, hyperspectral imaging satellites that provide data on the composition and characteristics of planetary objects and surfaces, is apt for India’s entire spacetech start-up ecosystem.

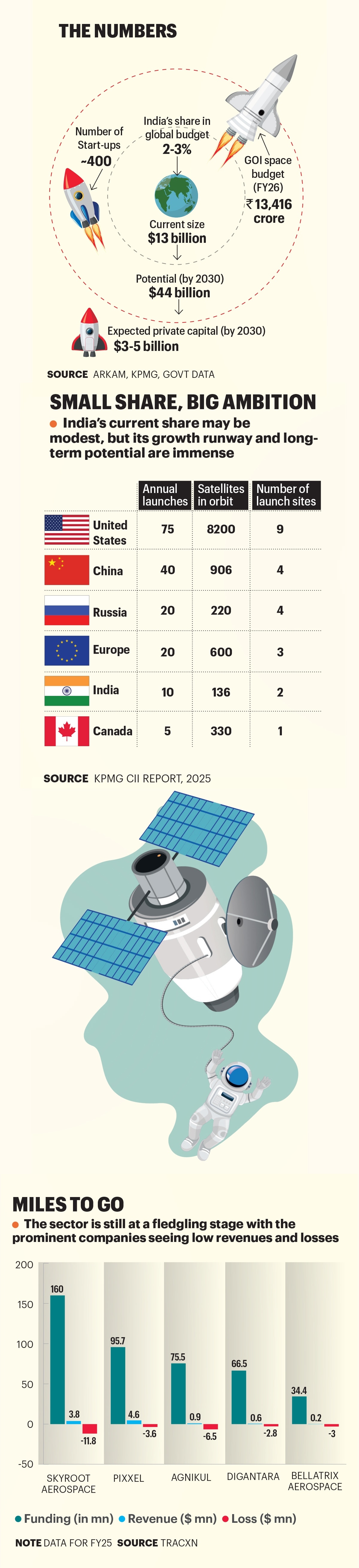

Although it has round 200,000 start-ups, the world’s third largest number, India remains a relatively small entity in the spacetech industry. Most of its start-ups are less than a decade old and are still building core capabilities.

“Across the ecosystem, including us, no company has yet demonstrated large-scale commercial execution,” Ahmed told Business Today from the US.

Vast gap but narrowing fast

The gap between India and global space leaders like the US is vast. Decades of sustained investment and active participation by non-state entities have given mature markets a commanding lead.

The global space economy, estimated at $596 billion in 2024, has been growing 5–8% annually over the past decade, according to a report by the Confederation of Indian Industry and consultant KPMG.

To be sure, India’s growth is nothing to sneeze at. Industry estimates suggest India’s space sector could cross $40 billion by the end of the 2030s, having expanded from $8.4 billion in 2022 to $13 billion now.

That’s promising in a world where conquering space is no longer simply a matter of prestige; space has emerged as a theatre for the projection of geopolitical muscle power.

This has been proven by the use of space technologies like satellite data in the conflict between Iran, and the US and Israel.

From intelligence gathering to non-kinetic warfare, space technology has become a critical, dual-use capability shaping modern conflict—a fact also demonstrated during Operation Sindoor, which India launched against terrorist bases in Pakistan following the Pahalgam attack in 2025.

To be sure, momentum is building rapidly in India’s spacetech industry. The acceleration is being driven by policy liberalisation, increasing non-state participation, and a surge in start-up activity. From fewer than 250 spacetech start-ups a few years ago, India now has around 400 ventures.

For decades, India’s space programme was synonymous with the Indian Space Research Organisation (ISRO).

While ISRO remains the backbone of the ecosystem, government reforms like the Space Policy of 2023, creation of the Indian National Space Promotion and Authorisation Centre to oversee non-government entities and a Rs 1,000 crore space venture fund have opened the doors to a new generation of start-ups across satellite manufacturing, launch and data services.

Investors are beginning to take note. “This is an industry of national importance,” says Arjun Rao, General Partner at the venture capital fund Speciale Invest. “While estimates peg India’s space economy at $40–45 billion in the coming years, that may only scratch the surface of its true potential. Importantly, much of that reflects domestic demand. The bigger opportunity lies in building from India for the world, with start-ups serving global markets.”

Building pedigree

Speciale Invest has backed seven spacetech start-ups, including Agnikul Cosmos, known for building the world’s first fully 3D-printed rocket engine and India’s first private launchpad.

Rao concedes that these are early days for the spacetech industry. “Even for someone like Elon Musk, building and launching a rocket took close to a decade,” Rao says. “You can’t compress that into a few years. These companies need to build space pedigree—one launch, then a few satellites, then scaling up. Only after that does revenue follow.”

This is a crucial distinction. Unlike software or consumer start-ups, spacetech is inherently capital-intensive and time-consuming. Revenue generation often follows multiple successful missions.

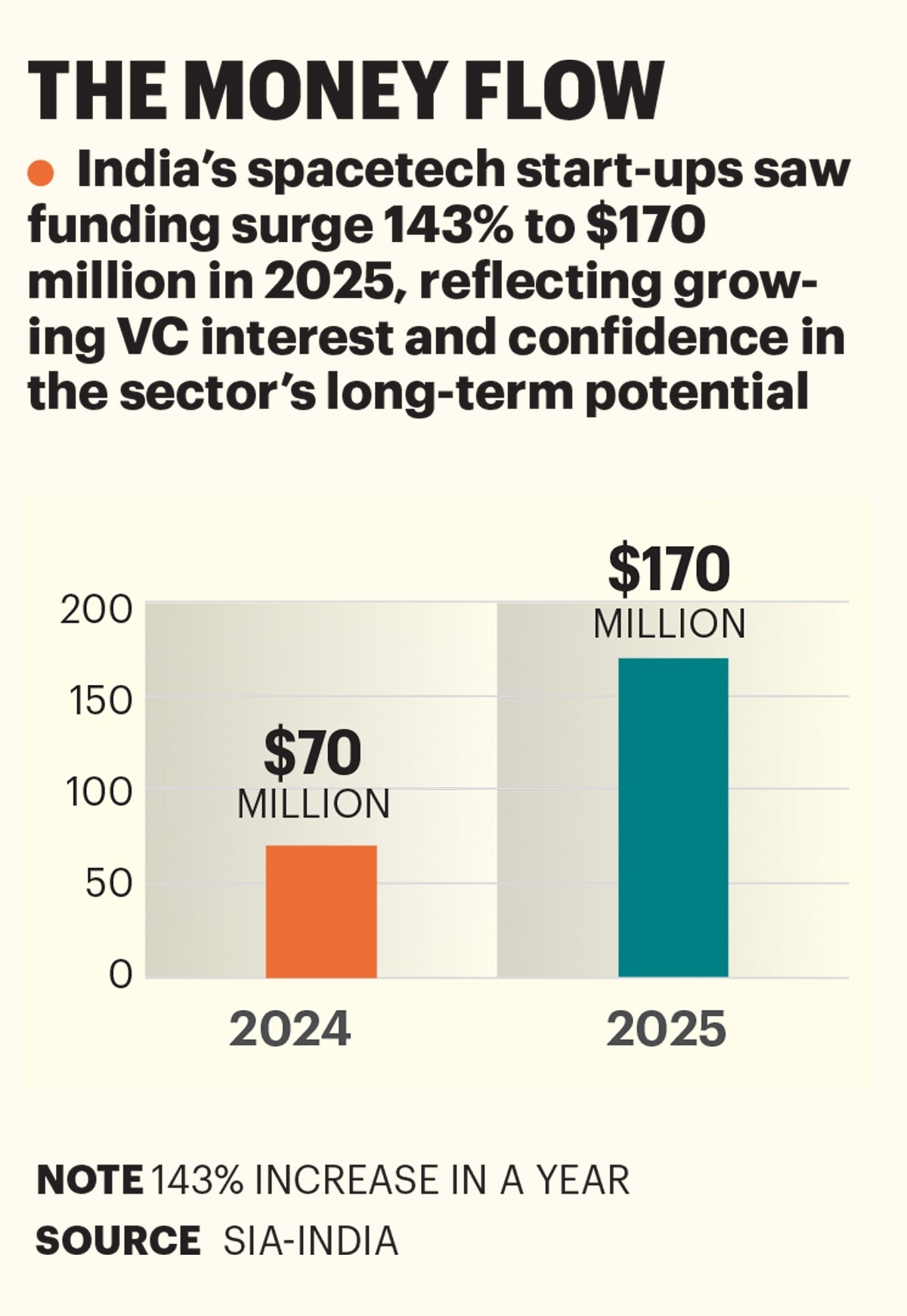

While early-stage funding has improved, growth capital is scarce.

According to Mario Gonsalves, India leader of the public sector practice at consulting firm BCG, spacetech firms have globally raised nearly $28 billion over the past five years. In comparison, Indian start-ups have secured just about $354 million—roughly 1.3% of global capital, despite accounting for 5–6% of start-up activity in the same period.

Data from Tracxn, which follows start-up activity, shows that of 225 spacetech start-ups in 2025, only 78 secured funding. Just nine progressed to a Series B funding round or beyond. Even among funded companies like Skyroot Aerospace (India’s first spacetech unicorn), Pixxel, GalaxEye, and Digantara, access to late-stage capital is a challenge.

Among the spacetech start-ups today, only Skyroot Aerospace, co-founded by Pawan Kumar Chandana and Naga Bharath Daka, has raised close to $100 million. Skyroot specialises in small satellite launch vehicles and in 2022 made history with Mission Prarambh, launching India’s first non-ISRO rocket, Vikram-S.

The top three players—Skyroot Aerospace (~$160 million), Pixxel (~$96 million), and Agnikul (~$75 million)—account for over half of the total private capital raised in the sector, while most others operate with sub-$10 million funding.

The issue isn’t talent or innovation—India has both. The constraint is patient capital willing to back long gestation cycles.

Early-stage by design

Global benchmarks like Musk’s SpaceX and Rocket Lab often dominate comparisons. But industry figures argue that such parallels are premature.

Gonsalves explains that India’s spacetech ecosystem is early-stage by design. Non-government investment began only in 2020, and the absence of late-stage capital continues to cap scale.

The journey from prototype to scale in spacetech—especially for launch companies—is inherently capital-intensive and long-drawn.

As Chandana of Skyroot explains, the process involves sustained investments in R&D, propulsion testing and subsystem validation, with each cycle becoming progressively more complex and expensive.

For a launch start-up, achieving its first successful orbital flight is not a near-term milestone. It typically takes close to a decade of development, multiple test cycles and significant capital outlay. “Investors who understand this timeline from the outset are critical,” Chandana says.

This raises the question: are Indian investors aligned to such long gestation cycles especially in a system often driven by expectations of high returns and clear exit pathways?

Chandana says the level of awareness is growing. “The early backers of Indian spacetech—who invested when there was no national space policy and no defined exit path—were genuine believers in the sector. They understood the timelines involved and set an important precedent,” he says.

Even today, a large share of capital in Indian spacetech comes from global investors like Lightspeed and Accel, with only a handful of domestic venture firms actively participating.

Rahul Chandra, Managing Director of Arkam Ventures, which has backed Skyroot Aerospace, says investor awareness and comfort have improved from three years ago. Crucially, India’s spacetech capabilities are increasingly being seen as globally relevant. This potential to build for international markets—not just domestic demand—is what continues to attract global capital.

Domestic venture capital continues to be skewed toward companies in the software, software-as-a-service (SaaS) and artificial intelligence segments, leaving hardware-heavy businesses relatively underfunded.

A recent report by Arkam Ventures predicts $3–5 billion of private capital inflow by 2030 to the spacetech sector.

Government-backed demand is emerging as a critical enabler. Through programmes like Innovations for Defence Excellence (iDEX) meant to foster defence and aerospace and increased procurement of space-based solutions, early revenue visibility is improving for start-ups.

A parallel push on exports, combined with a more open Foreign Direct Investment regime, is also expected to ease both capital inflows and outflows, strengthening the ecosystem’s financial foundation.

That said, the sector remains in its early stages. The absence of near-mature companies across key segments like satellite imaging, communications, and launch services means the ecosystem is still evolving. The next phase of growth will hinge on a handful of start-ups demonstrating commercial viability at scale.

Exit strategy

Most crucial is the need for spacetech companies to offer an exit strategy to their investors.

Equally crucial is commercial execution—getting to orbit, proving cadence and manufacturing at scale.

Skyroot’s Vikram-S flew as a sub-orbital demonstrator in 2022. Agnikul conducted a sub-orbital demonstration of its Agnibaan SOrTeD in June 2024.

Skyroot is now targeting the launch of Vikram-I, which will become the first orbital private-sector, around May 2026, in an event that will mark an inflexion point for Indian spacetech.

Space applications – earth observation data, supporting services in agriculture, disaster management, rural connectivity, and climate monitoring – make up 75% of the value of spacetech and are dominated by government-run infrastructure.

Government procurement will be very important for start-ups, as this does two things at once: it creates anchor demand in a sector where product development cycles are long and technical validation is enormously important; second, it gives young companies credibility.

“In spacetech, an early contract is not just revenue, but also proof that the product works in a mission-critical environment, which can materially de-risk the business for future customers and investors. But I would not call government procurement the most important revenue stream for the sector as a whole. It is an important early de-risking mechanism, and not the full market. The opportunity itself is broader than government demand,” says Chandra of Arkam Ventures.

Long-term growth will depend on a diversified revenue mix across government, enterprise, global clients and data-led applications.

Suyash Singh, co-founder and CEO of GalaxEye, which is building India’s first multi-sensor imaging satellite, says Indian start-ups are largely on par in terms of capability with their global peers.

“We may be six months to a year behind, but we do have launch vehicles and the ability to build satellites. Where we lag is in capacity—we don’t yet have thousands of satellites in orbit,” he says.

As space becomes central to both economic power and national security, India’s ambitions are no longer optional, they are strategic. The country has built capability, sparked start-up momentum and opened up policy.

The next phase will test execution—scaling capital, creating global businesses, and delivering meaningful exits.

@PalakAgarwal64