Arun Alagappan’s passion for agriculture comes through clearly in how he breaks down each issue succinctly. After all, the Executive Chairman of Coromandel International is as close to the farmer as anyone in India Inc can get; offerings include fertilisers, specialty nutrients, crop protection, retail presence and a play in technology.

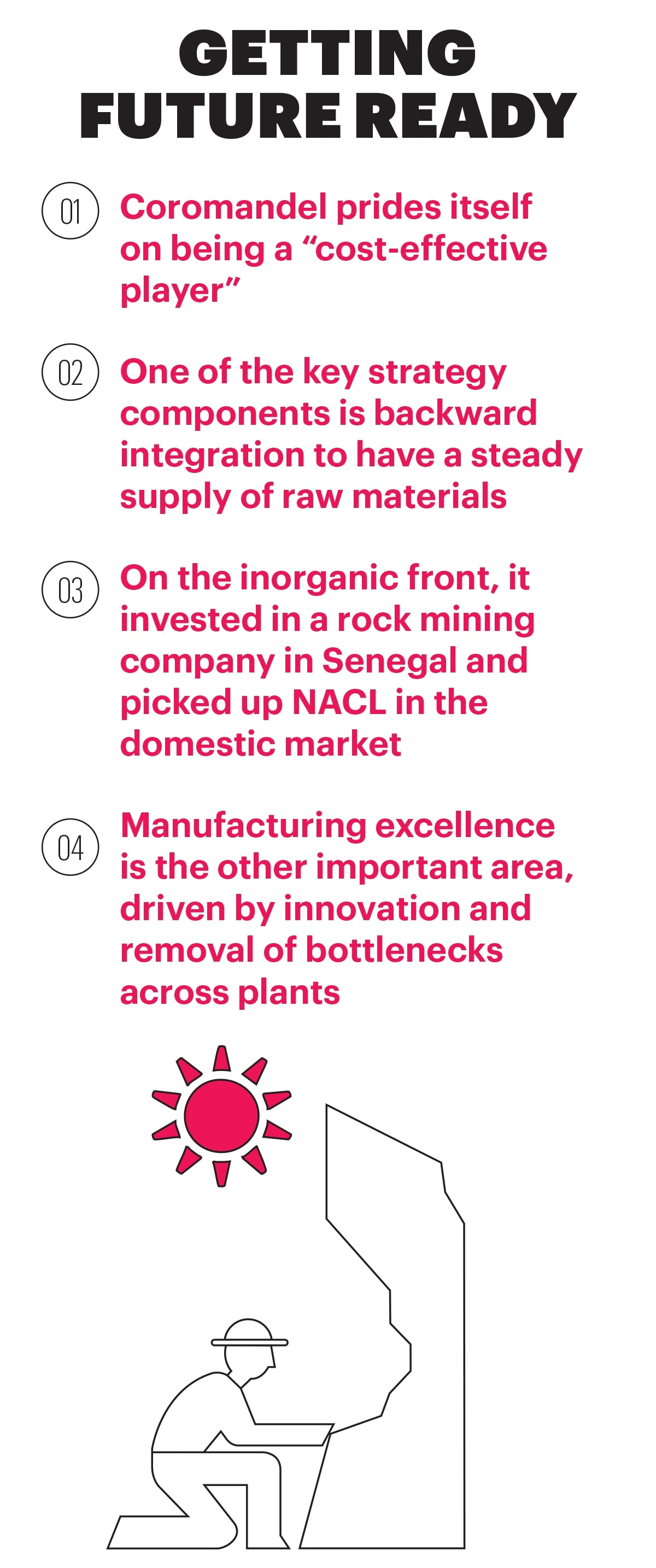

Sitting in his spacious but austere room in Coromandel’s Chennai office, Alagappan underlines his constant endeavour: making Coromandel a “very cost-effective player.” After all, the company plies its trade in a sector that is tightly regulated, has thin margins and requires deep reservoirs of patience; obsession with efficiency is the only way to ensure strong returns.

For Alagappan—who moved into Coromandel in early 2021 after stints at other Murugappa group companies like Cholamandalam Investment, TI Cycles of India and Parryware Roca—the pivot to agriculture meant he had to get back to basics.

The past three years, in particular, have been critical for Coromandel. “What we did right was strengthening the company’s fundamentals rather than chasing only front-end expansion,” he says. In this commodity-influenced business, there was disproportionate focus on two levers: operational innovation and supply chain resilience.

When Alagappan took charge, Coromandel was importing 65% of its sulphuric acid requirement. He, along with his team, decided to explore how the company could add more value and bolster margins by reducing imports.

The company looked at each process and zeroed in on mining. It could either own a mine or enter into long-term contracts with those who did, says Alagappan. Towards the end of 2022, Coromandel picked up a 45% stake in Baobab Mining and Chemicals Corporation, a Senegal-based rock phosphate mining company and last July upped that to 71.5%. This has given the company “mining-linked capability.”

Another key decision related to securing critical raw material. “It moved from just being an advantage to a hygiene factor. We invested time and leadership bandwidth to derisk sourcing, deepen vendor partnerships and build flexibility across our inbound supply chain to make sure we could serve the farm sector without disruption,” says Alagappan.

Coromandel also increased captive capacity for key inputs. “We reduced import dependence for key raw materials from around 65% to 40%. This has improved resilience, reduced volatility and given us better continuity of supply,” says Alagappan.

The company also decided to make manufacturing excellence a priority. It drove disciplined process innovation and removed bottlenecks across plants. “That led to meaningful output improvement with minimal incremental capex. For instance, we have been able to lift production volumes by around 20% in some facilities primarily through process and operating discipline,” Alagappan says.

Apart from de-risking its supply chain, Coromandel increased the breadth of offerings and strengthened the integrated agri-solutions platform. “We are strong in manufacturing and market access. That includes making nutrients at a large scale, leadership in complex fertilisers and having a pan-India distribution engine, with a deep last-mile presence through our rural retail network,” says Alagappan.

The other factor that differentiates Coromandel is a portfolio-led model. This allows it to have a play across nutrients, crop protection, bio-products and tech-led solutions. “It lets us solve a broader crop outcome problem rather than selling inputs in silos.” Finally, he lays emphasis on the scale accruing from real assets and capability depth.

“India has high agro-chemical diversity and sensitive farmer economics. In such a scenario, the ability to adapt formulations, improve efficacy and bring differentiated products quickly is a strategic advantage,” he says.

Each effort is an attempt to challenge the status quo and do different things. “We did not understand rock mining but got into it. We added capacities in sulfuric acid and phosphoric acid, which helped in creating the entire value chain and addressed the raw material need,” says Alagappan.

Together, those efforts have shifted the approach at the company. Take the case of the plant in Kakinada, Andhra Pradesh, which has transformed from one that was largely into mixing to becoming integrated. “With sulfuric and phosphoric acid, we are making complex fertilisers. Next year, it will become the single largest site for making phosphatic fertilisers in India,” says Alagappan.

On the retail side, its brand Gromor is opening a store a day and expanding reach. “As a company, we are highly entrenched in Andhra Pradesh and Telangana and touching the border markets of Karnataka and Maharashtra,” he says.

Plus, last March, Coromandel acquired a 53% stake in NACL, a crop protection company with a strong branded formulation business, for Rs 820 crore. “We have got 14 new formulations plus fungicides. These are difficult businesses to build,” says Alagappan.

Those tracking the company seem to like the shift in the way the company operates. A Motilal Oswal report released in February after third quarter earnings said it is well-positioned to sustain the growth momentum in FY27 on the back of “favourable market dynamics, increasing shift towards NPK (nitrogen, phosphorus and potassium) fertilisers for balanced nutrition and strong growth in crop protection led by synergy benefits of the NACL consolidation.”

The medium-term outlook remains strong on account of five factors—expanding into new geographies, developing new molecules across fertilisers and crop protection segments, backward integration for the fertiliser business, purchase of NACL and scale-up of Senegal-based Baobab Mining and Chemicals Corporation.

Crisil Ratings says the NACL purchase was funded via internal cash accrual and Coromandel’s net liquidity after the acquisition stood around Rs 450 crore as on August 31, 2025. “Given strong expected accrual and no significant debt-funded acquisitions, Coromandel’s financial risk profile is expected to remain strong. This acquisition augments the crop protection business, strengthening its presence in the domestic formulations business, expanding existing product portfolio and helping in securing contract manufacturing relationships with NACL’s established customers,” it said.

Alagappan stresses that Coromandel thinks like a tech company. “With predictive AI models, we are trying to see what kind of pests are present in an area,” he says. That is a reflection of the changing nature of the Indian economy. “Today’s farmer is younger and tech-savvy. I have seen some of them leaving IT and coming to farming.” That makes it vital for Coromandel to adapt to those for whom WhatsApp comes easily and technology is readily accessible. “These are not things that are nice to have. Rather, they are must-haves. Farmers are very advanced and do their research. Plus, they all use ChatGPT,” he adds with a smile.

For Alagappan, technology ties in neatly with his emphasis on making the firm stronger and more efficient.

@krishnagopalan