For generations, small savings schemes have been the bedrock of Indian household finance—a quiet, dependable habit passed down over time. Millions of families have tucked away savings in post office savings accounts or the Public Provident Fund (PPF) or invested in the National Savings Certificates or Kisan Vikas Patra. The objective was simple—to save whatever they could and hope to build a steady corpus that could be used for milestone events like higher education or wedding expenses of their children, building a house or for life post-retirement or even life-threatening illnesses.

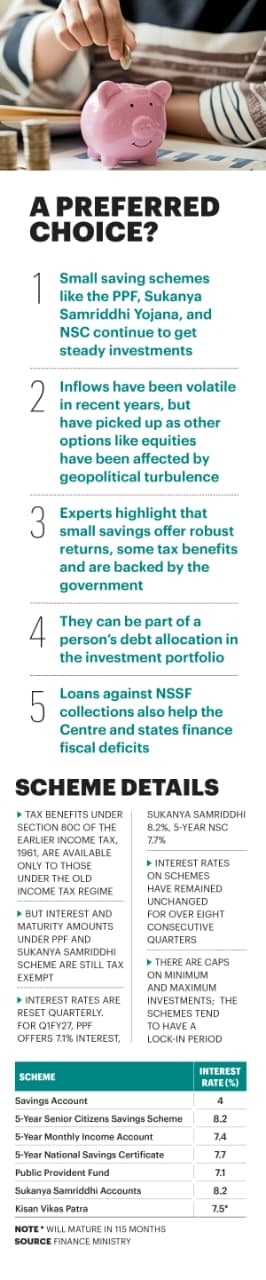

With robust returns and tax benefits available under the erstwhile Section 80C of the Income Tax Act, 1961 (now Clause 123 of the Income Tax Act, 2025), small savings schemes initially helped “promote the habit of thrift and savings among citizens” of a newly independent India. Over the years, these schemes gained popularity and newer generations continued to invest in them.

Some of these schemes started decades ago and some are over a century old and trace their origins to the pre-Independence era. The Government Savings Bank Act was passed in 1873, and the Post Office Savings Bank of India came into existence way back in 1882. Post Independence, small savings gained more momentum, and the National Savings Organisation was set up in 1948.

Since then, many new schemes have been launched, creating a whole bouquet of products aimed at different borrowers. In recent years, the Sukanya Samriddhi Yojana was launched in January 2015 under the government’s Beti Bachao, Beti Padhao campaign. The Mahila Samman Savings Certificate Scheme was launched on March 31, 2023, to promote financial independence of women as a special two-year scheme till March 2025.

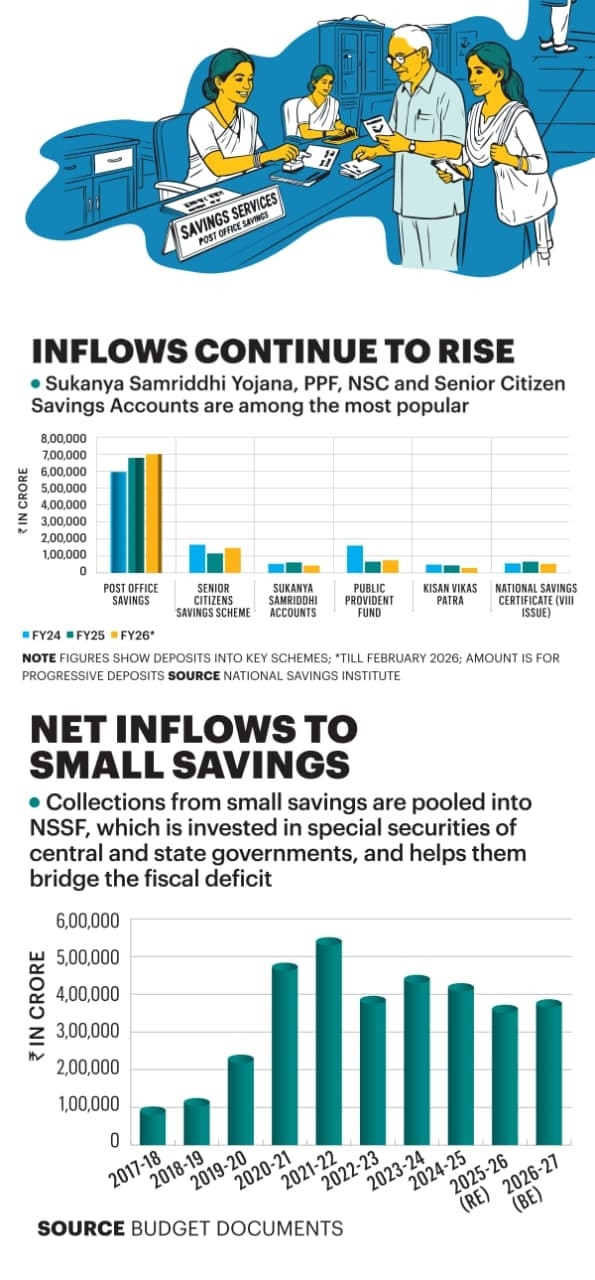

But in recent years, a combination of factors has somewhat reduced their attractiveness for small investors. However. with volatility in equity markets and commodities, experts say that small saving schemes continue to hold ground. This is evident in the net inflows to small savings, which are then pooled into the National Small Savings Fund (See graphic: Net inflows to small savings). The net collections from the NSSF are invested in Central and State Government Special Securities as well as in various public agencies to help the Centre and states bridge their fiscal deficit.

A Robust Instrument

Economists highlight the role of small savings in promoting domestic household savings that have played a significant role as the primary source of capital formation in the country needed for investments across the economy. The decline in household savings has been a matter of debate in recent years and within that of small savings, a further concern. Household savings are estimated at Rs 69 lakh crore in FY25, amounting to 62.1% of GDP. In absolute terms, household savings were seen at a lower level of Rs 52.25 lakh crore in FY23 but amounted to a larger share of the GDP at 67.2%.

D.K. Srivastava, Chief Policy Advisor, EY India sums up this trend and points out that the share of small savings in gross domestic savings has been declining in recent years—from 3.9% of total gross domestic savings in FY23 and 4.4% in FY24 to 3.1% in FY25. “As an instrument of savings, small savings have become less attractive for households,” he says, adding that the share of small savings in financing the fiscal deficit has also gone down in recent years and the government is relying more on market borrowings.

The General Secretary of the Hind Mazdoor Sabha, a major national trade union federation, Harbhajan Singh Sidhu, points out that the EPFO continues to provide a robust interest rate of 8.25%. Sidhu, who is also a member of the Central Board of Trustees of the EPFO underscores, “If interest rates don’t remain attractive for borrowers, like what has happened with fixed deposits, it will ultimately impact domestic savings, which are necessary for the economy”.

Small savings slowly started to lose favour as the preferred investment choice as equity markets gathered momentum and products like mutual funds and systematic investment plans as well as newer investment options like gold, crypto, and real estate offered much higher returns. Along with that, the switch to the new income tax regime that offered no exemptions but lower tax slabs, also somewhat reduced the attractiveness of these schemes.

Returns on these schemes have been unchanged for over eight consecutive quarters. The Shyamala Gopinath Committee, constituted to study small savings schemes, had suggested a market-linked formula for interest rates for small savings which should be 25 to 100 basis points higher than the average yield on government securities of the same maturity for the previous quarter.

However, to protect small investors from very low returns, the government often also chooses to keep the interest rates artificially high.

Government sources have often pointed out that the post tax returns on these schemes continues to be much higher compared to several other schemes, which is an advantage for small savers. For the exchequer, small savings can be a costly outgo as it means a higher cost for interest rates and then borrowing from the NSSF at a higher rate.

Finance Minister Nirmala Sitharaman recently addressed the issue, calling it a “double whammy”, as it is costing the government on both sides. Noting that nowadays retail investors are saving through different platforms, she further said that it is a big ‘dharma sankat’ (moral dilemma) for the finance ministry every quarter. “Whether you will bring this down and cause hurt to senior citizens, who are probably living on that little interest rate that they earn out of it, but it is. We are ensuring that they don’t earn less, but equally if I just looked at the kitty of NSSF, it is from that same kitty I am borrowing,” she said.

However, with recent volatility in equity markets over the last one and half years, returns on several products have become shaky. For instance, the short-term returns of mutual funds have become uncertain.

The rates on fixed deposits too have become less attractive amidst rising inflation and tax treatment.

Steady Returns

Srivastava notes that with increasing uncertainty arising from the West Asia conflict and with the flight of net foreign capital flows from India, the government may need to rely more on domestic savings to finance fiscal deficit. “In this scenario, the government can promote small savings as an avenue for medium- to long-term investments. For this to happen, interest rates on small saving instruments need to be revised,” he says.

Experts also highlight the role of small savings in portfolio diversification and point out that steady returns means that they continue to be the preferred investment avenue with several small investors despite the lower tax benefits available in the new income tax regime that nearly 90% of individual taxpayers have migrated to.

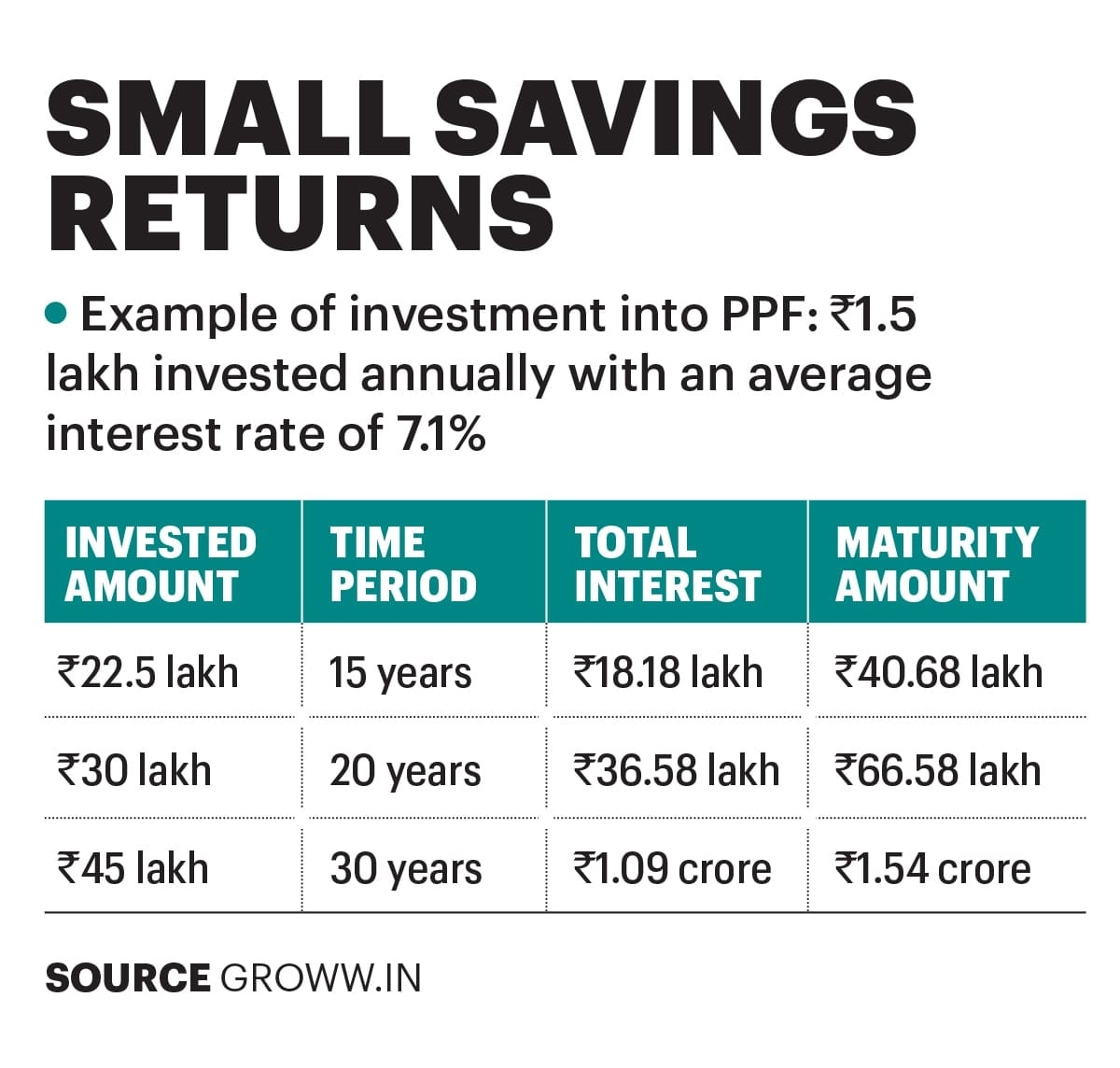

The most popular amongst small saving schemes are the PPF, Sukanya Samriddhi Scheme, National Savings Certificate and the Senior Citizens Savings Scheme.

However, one must remember that investments tend to get locked in for a specific period and those looking to exit must remember that accounts under these schemes can be closed prematurely only under certain conditions. There are also minimum and maximum investment caps under most schemes.

Harshad Chetanwala, Co-Founder of financial planning platform MyWealthGrowth.com says that small saving schemes should not be looked at from the point of view of tax savings as Section 80C is available only for those in the old income tax regime.

“PPF and the Sukanya Samriddhi Scheme still have tax exemption on the interest and the corpus. But from the perspective of diversifying one’s portfolio, small savings are still a good option and can be part of the investor’s debt allocation,” Chetanwala says.

The Senior Citizen Saving Scheme is especially useful to retired investors or those on the verge of retirement but one should remember that the money gets locked into this scheme and hence is not a good option for those looking for easy liquidity, he explains.

PPF also stands as a good option for those who are not a part of any social security scheme like the Government Provident Fund or Employees’ Provident Fund. “These could be self-employed professionals or business owners,” says Chetanwala.

Tax Treatment

To be clear, taxpayers under the old income tax regime continue to have benefits of tax exemption of Rs 1.5 lakh for specified investments, including those to small savings. But this is no longer available under the new income tax regime. However, the interest and maturity amount under PPF and Sukanya Samriddhi Scheme are tax exempt. Other schemes tend to be taxable at the relevant slab rates.

Shaily Gupta, Partner of law firm Khaitan & Co explains the nuances and says that while the tax saving benefit of Section 80C is no longer available to those under the new income tax regime, PPF is still a preferred investment option as it inculcates a habit of saving and gives a good return. Further, the interest and the amount on maturity is fully tax exempt.

Sukanya Samriddhi Yojana is the second most preferred option and is a very tax efficient scheme for a girl child, she says, adding that it also offers tax exemption for interest and the maturity amount.

“The National Savings Certificate also remains very popular with some segments of taxpayers, but it is not as commonly preferred as the PPF, as the overall annual deduction limit of Rs 1.5 lakh under Section 80C is often fully utilised through PPF contributions alone,” she further explains.

While the interest earned on NSC is taxable on an accrual basis, it is deemed to be reinvested and accordingly qualifies for deduction under Section 80C (under the old regime) for the first four years.

“The interest accrued in the fifth year of the scheme is not reinvested but paid out to the investor and hence does not qualify for deduction under Section 80C and is taxable at the applicable slab rate,” Gupta says. The Senior Citizen Savings Scheme also remains popular with retired investors who are looking for a regular income as it provides quarterly interest, but the interest amount is taxable, she adds.

Most importantly, small saving schemes continue to promote the original objective that they were formulated for—to inculcate the habit of saving. In fact, bankers and investment advisers note that even Gen Z continues to invest in schemes like the PPF in which their parents may have opened accounts for them.

While small savings may not be the focus, it is unlikely that they will lose their place in the retail investor’s portfolio. This is especially true in the current era of global volatility where safe haven investment opportunities are often few and far between. And maybe, in this instance, old is gold!

@surabhi_prasad