A new financial year has begun, but for India’s retail equity investors, it hardly feels like a fresh start. The portfolios they have carried into FY27 are under pressure, and the factors that created that stress are far from fading.

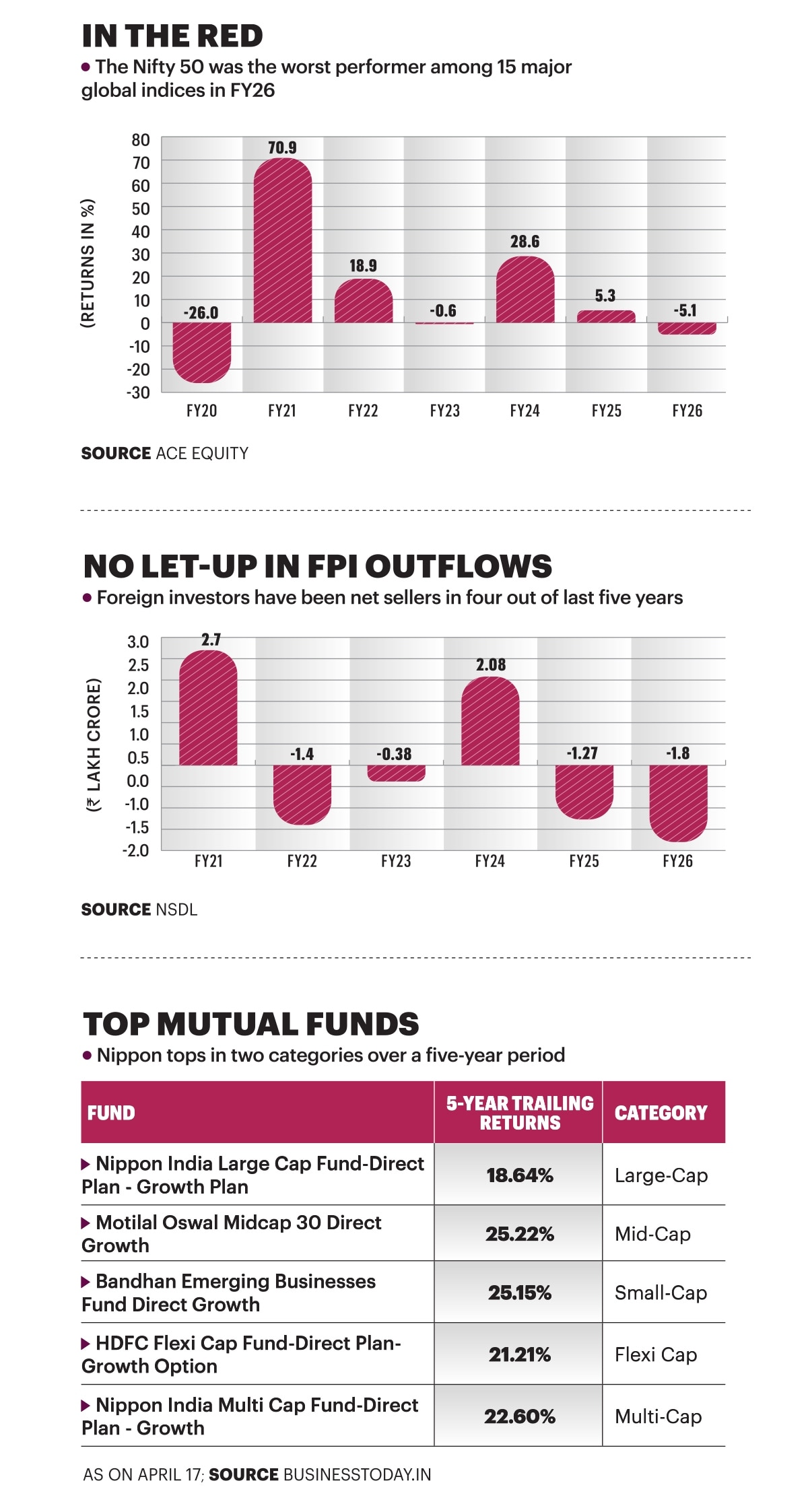

The Nifty 50 fell 5.1% in FY26, its weakest annual performance since FY20. It was the worst performer among 15 major global indices. For retail investors, who aggressively embraced equities during the post-pandemic rally, the disappointment was even more pronounced—the Nifty’s two-year compound annual growth rate was a negligible 0.01%.

The growing participation of domestic investors has amplified the impact. Household ownership of listed equities rose from 13% in 2015 to 20% on December 2025. As FY27 unfolds, the question is—what should investors do next?

Portfolios hit

Even before tensions between US-Israel and Iran unsettled global markets, Indian equities were grappling with stretched valuations, uneven earnings growth, weak domestic demand, and uncertainty around US trade policy. The hike in securities transaction tax (STT) on derivatives also dampened sentiment.

India’s vulnerability to global shocks is amplified by its high dependence—around 85%—on crude oil imports. Brent crude surged to $118.3 per barrel at the end of March amid the war, well above its one-year average of $68.7.

Elevated crude prices are squeezing corporate margins. Sectors dependent on crude-linked inputs such as paints, packaging, and logistics are facing cost pressures amid subdued demand. Aviation, ceramic tiles, oil marketing companies, and gas utilities remain particularly vulnerable.

“Rising oil prices are like ‘rahu kaal’ for our economy,” says Nilesh Shah, MD & CEO, Kotak AMC. “They push up inflation, widen the current account deficit, weaken the rupee, and compress corporate profitability. While our macro fundamentals remain strong, they have certainly deteriorated due to higher oil prices.” The rupee dipped sharply from 85.6 per dollar in April 2025 to 94.65 in March 2026, triggering heavy outflow of foreign funds. Global institutions are turning cautious. Goldman Sachs has cut India’s 2026 GDP growth forecast from 6.5% to 5.9%.

Despite the correction, equity valuations are not compelling. The Nifty 50’s price-to-earnings ratio has eased by about 14% to around 19.9 times, but remains elevated relative to peers. The MSCI Emerging Markets Index is trading at roughly 16.6 times earnings, implying a premium of nearly 20% despite weaker near-term earnings visibility. Mid- and small-cap stocks are trading at steep premiums of 56% and 34%, respectively, to large-caps, highlighting the risk in the broader markets.

A ‘Kangaroo Market’

The West Asia conflict has led to a roller-coaster ride for D-street investors with markets swinging on the ever-changing statements of a few global leaders. “Normally, we see bull or bear markets. This is the first time we are seeing a ‘kangaroo market’; it moves up and down sharply,” says Shah. “Everything is driven by global events, and those events are often dictated by a handful of players,” he says.

Many investors tend to draw comfort from past crises. The sharp recoveries after the 2008 global financial crisis and the Covid-19 pandemic have created an expectation that every downturn will be followed by a quick bounce-back. However, the backdrop this time is different. “It is premature to say the worst is behind us,” says Kranthi Bathini, Director (Research), WealthMills Securities. “Geopolitical developments are evolving rapidly, and uncertainty is high.”

Elevated public debt and persistent inflation constrain fiscal and monetary support. Crude prices are likely to remain high amid geopolitical disruptions. The earnings visibility is poor. As a result, any recovery is likely to be gradual and uneven.

Foreign outflows have been another pressure point. After strong inflows in FY21 and FY24, FPIs have been consistent sellers, with FY26 seeing record outflows of `1.8 trillion. A weaker rupee, geopolitical tensions, their preference for AI-led growth markets and more attractive valuations in other emerging markets have contributed to this trend. “India is seen as expensive, lacks a strong AI play, and investors have found better opportunities elsewhere,” says Shah. “If geopolitical tensions ease, selling may reduce but may not fully reverse.”

Retail action plan

Despite near-term challenges, the long-term outlook for Indian equities is intact. The current phase offers an opportunity to selectively accumulate quality businesses at more reasonable valuations. “FY27 is going to be another challenging year. Investors must keep a long-term horizon and buy quality on dips and have both core portfolio for at least three-five years and satellite portfolio, which focuses on trading strategies, including buy-on-dips and sell-on-rise, to take the benefit of volatility,” says Bathini. “This is the time to focus on bottom-up investing, companies with reasonable valuations and relatively lower disruption from the current crisis,” says Shah.

Even as market volatility persists, some sectors have already begun to turn the corner. “Our first preference has been banking and financial services, where valuations are reasonable and impact is limited. The second sector is cement, which should benefit from infrastructure building and GST changes. The third is hotels and hospitals, where domestic demand and resilience support growth,” says Shah. One big theme, he believes, will be electrification with rising power generation, reduced dependence on crude oil, and shift towards electric mobility and cleaner energy.

At the same time, he cautions against sectors vulnerable to crude price shocks, including oil marketing companies and businesses dependent on petrochemicals such as chemicals, plastics, and fertilisers.

Mutual Fund Playbook

For investors, discipline remains the key. Equity allocations should be staggered and remain at neutral levels. Large- and mid-cap funds are expected to outperform small-cap funds over the next 18–24 months. Key themes are banking, healthcare, and consumer discretionary. Diversification is equally important. Investors should also consider exposure to alternative investment funds, structured investment products, and global equities.

As investors fine-tune their mutual fund portfolios for FY27, the focus should not only be on asset allocation but also identifying which sectors and themes are likely to lead or lag in the evolving market environment. “Domestic-oriented sectors appear better placed, particularly discretionary consumption such as passenger vehicles, jewellery retail and hospitals, where underlying demand continues to hold up well. Cement also looks good with improving volumes and pricing support. Renewable energy remains an attractive structural theme,” says Feroze Azeez, Joint CEO, Anand Rathi Wealth.

“Within financials, the tilt is towards PSBs over larger private banks, and towards banks over NBFCs, given the relative comfort on asset quality and growth visibility. In IT, the absence of negative surprises provides comfort, with large-caps appearing more reasonable on valuations. Real estate, FMCG and export-oriented chemicals may face near-term headwinds and underperform,” he says.

Trends Shaping MFs

“Indian investors have become smart and are treating mutual funds as a disciplined savings avenue rather than a tactical investment product. This is clearly visible from the AMFI data, where consistent and rising SIP contributions even during volatile periods indicate a growing preference for long-term wealth creation over short-term market timing,” says Azeez of Anand Rathi Wealth.

As per AMFI data for March, SIP inflows touched record highs at `32,087 crore, marking the seventh consecutive month above the `29,000 crore level, while FY26 contributions stood at a strong `3.5 lakh crore. Equity inflows remained robust at `40,450 crore, the highest since July 2025, suggesting that investors are using market corrections to increase allocations rather than exit.

For long-term investors, a structured asset allocation remains critical. “A balanced portfolio could include an 80:20 mix between equity and debt, with equity exposure diversified across large, mid, and small caps,” says Azeez. Equity diversification becomes key in volatile markets. “Equity investments should follow an ideal market cap mix of 50-55% in large-caps, 20-25% in mid-caps and the rest in small-caps. This will help investors ride all market cycles smoothly.”

Gold & Silver

With gold rising 75% in 2025 and silver over 150%, the outlook for precious metals appears more balanced. “While the long-term trend remains constructive, investors should be prepared for phases of consolidation, intermittent corrections, and higher volatility. The bias remains positive, but returns may be more tactical, requiring disciplined allocation and staggered buying,” says Navneet Damani, Senior Group Vice President-Head Research, MOFSL.

Gold and silver are being driven by a mix of global macro factors. Conflicts such as Israel–Hamas and Russia–Ukraine initially pushed demand, but in the absence of fresh escalation, there was some profit booking. At the same time, inflation concerns remain elevated. “Volatile crude oil prices are a key factor. Central banks have stayed cautious and delayed rate cuts. This has kept US bond yields and the dollar relatively strong, limiting any sharp upside in gold,” says Damani.

Liquidity has tightened globally. Changes in Japan’s policy and impact on yen carry trades have added to this pressure. However, the broader environment still supports gold. “Sticky inflation along with slowing growth raises stagflation risks. That is structurally positive for gold,” says Damani. “On the domestic front, gold is expected to test `1,85,000–1,90,000 on the upside. For silver, targets are placed near `3,30,000 on MCX. Overall, the bias remains constructive, but a staggered approach of investment is advised.”

Every market cycle may not be about chasing returns. There are periods in markets when it is more important to stay invested and survive before you thrive again.

@sakshibatra18