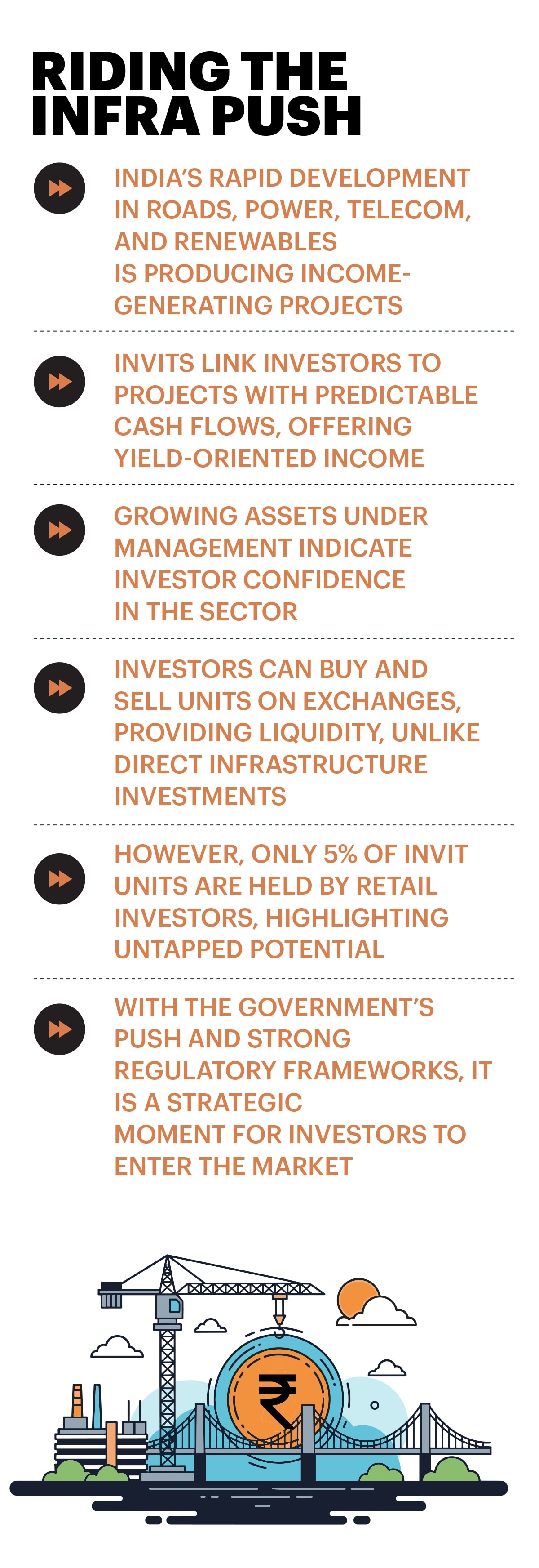

The Centre's infrastructure push since the outbreak of Covid-19 has made both institutional and retail investors look at ways to ride this theme without taking too much risk. One asset class that has come to dominate the discussions is infrastructure investment trusts (InvITs).

InvITs pool investor money to buy infrastructure assets such as highways, power transmission lines and telecom towers that generate steady income through tolls, tariffs or user fees. They distribute most of it to investors at periodic intervals. Since the assets are operational and revenue-generating, the income is relatively stable. Investors can also benefit from capital appreciation.

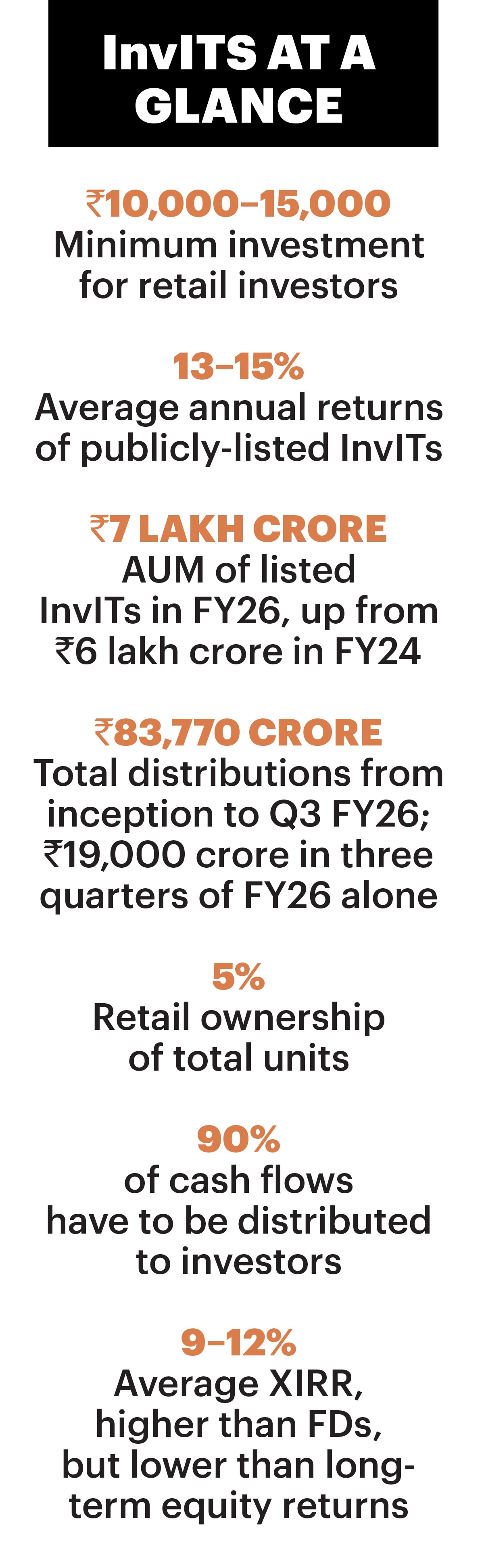

One reason for the rising interest in InvITs is their alignment with the Viksit Bharat 2047 vision. They are benefitting from a favourable macroeconomic environment marked by competitive interest rates and rising demand for stable yield instruments. This is reflected in expansion of assets under management (AUM) from Rs 6 lakh crore in FY24 to Rs 6.25 lakh crore in FY25. It is expected to have grown to Rs 7.25–7.5 lakh crore in FY26. The AUM is projected to grow to Rs 12 lakh crore by FY30.

In a volatile equity environment, heightened by the war in West Asia, investors are considering predictable income-generating assets, says Shrinivas Rao, CEO of real estate solutions firm Vestian. “This combination of structural growth and yield-driven demand is supporting sustained interest in the InvIT segment,” he adds.

Retail Interest

InvITs, launched in India in 2016, with the first listing in 2017, saw limited success initially, discouraging retail participants. Most InvITs were sold as private placements to institutional investors, delivering steady payouts and gradual capital appreciation, which built confidence. At the same time, early listed InvITs such as India Grid Trust and IRB InvIT Fund improved their performance over time as their asset base expanded and cash flows stabilised.

“The first few InvITs did not perform well, with some trading below their issue price, exposing early retail investors to principal loss,” says Kuljit Singh, Investment Banking Partner and Leader—Infrastructure, EY India.

In 2018, however, the product was positioned for retirement planning, as an alternative to fixed deposits. With regular cash distribution, often 10% annualised, potential capital appreciation, and listings that provide transparency, InvITs are becoming popular among retail investors seeking stable returns by participating in India’s growth story.

Yet, though retail engagement with InvITs has grown steadily over the past few years, fueled by the Securities and Exchange Board of India’s (Sebi’s) reduction of the minimum investment to Rs 10,000 for a unit, rise in new listings, and better investor awareness, individual ownership still lags. “Industry data shows that retail investors hold only 5% units, while institutional players, both domestic and global, dominate with a 95% share,” says N.S. Venkatesh, CEO of Bharat InvITs Association.

Now that some investors have made decent returns, industry insiders expect retail participation to increase significantly. InvITs have outperformed traditional asset classes like bank FDs. In a savings account, you get 3-4% interest; in an FD, 6-7%, but then your money is blocked. “Most InvITs are giving 10% on the market price. You can hold the unit for less than a year and still get 10% annualised return. Over the years, there has been capital appreciation, too,” says Singh.

But perhaps the most fair comparison is with another asset class born with InvITs—real estate investment trusts (REITs), which own or operate real estate projects, deriving returns from rent and the appreciation of the asset. In India, REITs have typically offered 6-7.5%, according to Credai National and ANAROCK, close to FDs, but with exposure to commercial real estate.

On the other hand, equities have delivered more in the long term, with compound annual growth rate of 11–13% on the Nifty 50 over the past decade. However, equities have greater volatility and no guaranteed income stream.

Interestingly, at the regulatory level, InvITs are categorised as hybrid instruments. “The parity in treatment of InvITs with REITs as equity instruments in general can allow mutual funds (MFs) and specialised investment funds to include them within their equity allocation limits, indirectly boosting liquidity and improving market participation,” says Badal Yagnik, CEO & Managing Director of commercial real estate firm Colliers India. In fact, investment by MFs is gaining traction, with 25 fund houses investing around Rs 55,000 crore in InvITs and REITs till the end of 2025.

“InvITs play a meaningful role as a stable income-generating component within a diversified portfolio, particularly given their relatively predictable cash flows and growing institutional interest,” says Rao.

Cash Flow Reality

InvITs generate steady cash flow from operational infrastructure assets across energy, transport, warehousing, and digital sectors, delivering consistent returns even during market volatility.

“Across diverse sectors, from energy, warehousing and digital infrastructure to transport, InvITs have demonstrated significant resilience in distribution consistency,” says Venkatesh. They are required to pay out 90% of their net distributable cash flows, ensuring a steady income stream that often outperforms traditional fixed-income assets.

This stability is driven by long-term contracts, regulated revenue frameworks, and essential-service characteristics, which cushion cash flows against economic volatility. While short-term disruptions may arise due to macroeconomic factors, interest rate movements, or sector-specific challenges, overall distribution patterns tend to remain resilient over time.

Data from ICRA Analytics and industry reports shows that InvIT distributions in India rose 55% year-on-year in FY26, even amid fluctuating market conditions, while total payouts continued to grow sequentially.

“Until Q3FY26, InvITs have collectively distributed approximately Rs 87,000 crore, of which about Rs 19,000 crore was paid during the first three quarters of FY26,” says Venkatesh. He adds that investors earned an average internal rate of return of 9–12%.

Post-Tax Returns

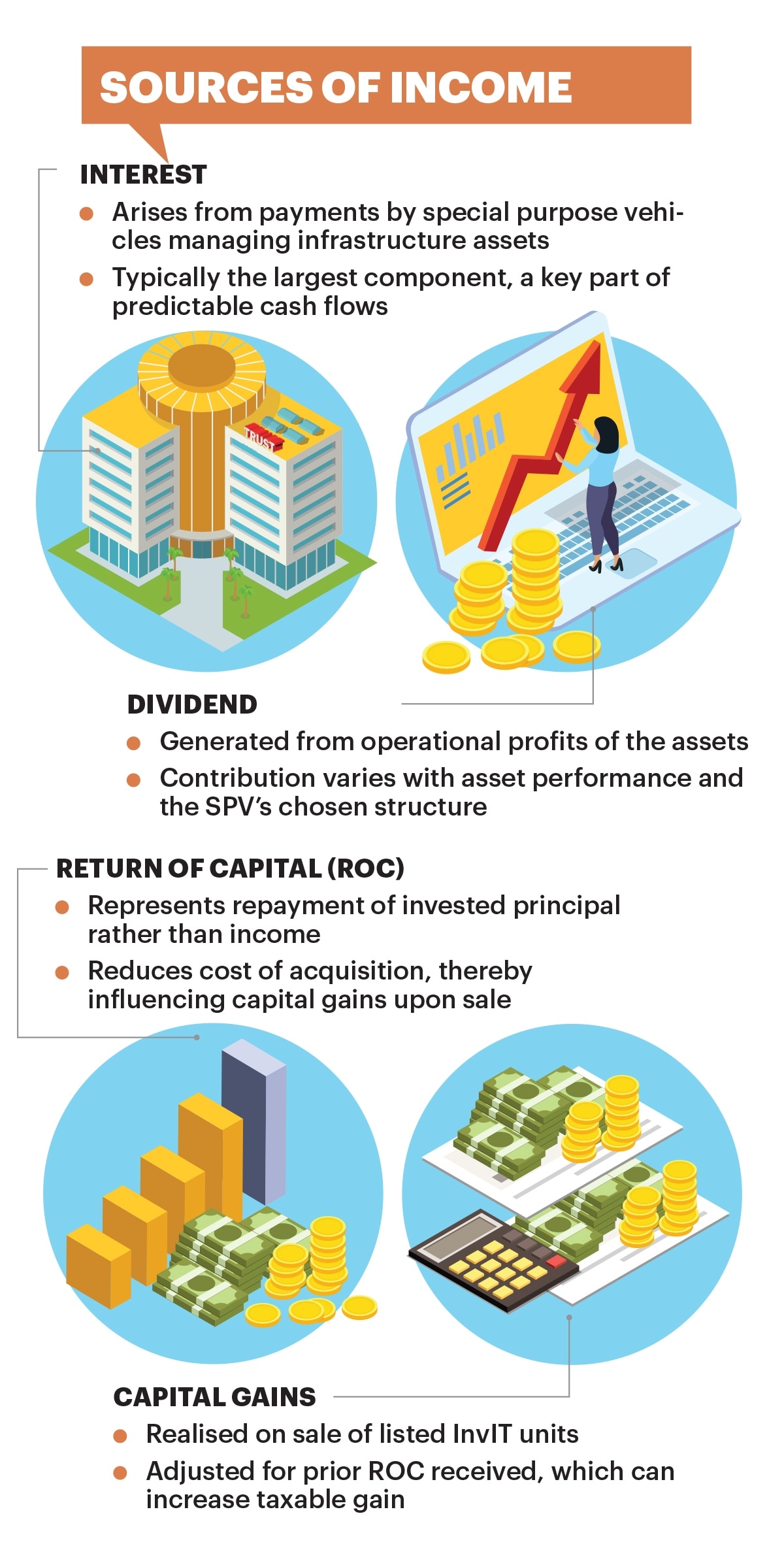

“InvIT distributions are complex as they include multiple components—primarily interest income, dividend income, and return of capital—each subject to distinct tax treatment despite being received as a unified payout,” says Ashish Parwani, Senior Partner at law firm Rajani Associates.

Interest income, typically the largest component, arises from payments made by underlying special purpose vehicles (SPVs) and is fully taxable in the hands of investors at applicable slab rates under “Income from Other Sources.” Consequently, it can reduce post-tax yields, particularly for investors in higher tax brackets.

Dividend income, on the other hand, is subject to differential treatment depending on the tax regime of the SPV. If the SPV has not opted for the concessional corporate tax regime, such dividends may be exempt in the hands of investors. However, in most contemporary structures where concessional regimes are adopted, dividend income is taxable at slab rates, diminishing tax efficiency.

Return of capital (ROC), often the most misunderstood component, is not income but a repayment of invested capital. While it is not taxed at the time of receipt, it reduces the investor’s cost of acquisition, increasing capital gains liability if the units are sold. Accordingly, ROC operates as a tax deferral mechanism rather than a tax exemption.

Capital gains on sale of listed InvIT units broadly follow equity taxation principles with rates based on the holding period. However, the cumulative effect of ROC adjustments may significantly enhance taxable gains at the time of exit.

From an investor’s perspective, the composition of the payouts is critical in determining real returns. “Headline yields may be misleading, as interest-heavy distributions result in lower post-tax income, whereas ROC-heavy structures may enhance near-term cash flows while deferring tax liabilities,” says Parwani. Additionally, taxability of dividends and the investor’s tax bracket play a decisive role in overall returns.

In this context, investors must avoid common pitfalls such as treating all payouts as uniform income, ignoring the breakdown, or comparing InvIT yields directly with traditional fixed-income instruments without adjusting for taxes. A prudent evaluation requires a careful analysis of distribution mix, historical consistency, and effective post-tax yield.

Sebi, too, is contemplating a number of changes to facilitate ease of doing business. “For instance, it has been proposed that privately listed InvITs be allowed to invest in under-construction projects up to 10% of the value of their total asset base in line with publicly listed InvITs,” says Janhavi Manohar, Partner, Cyril Amarchand Mangaldas.

Investment Checklist

InvITs offer more stability than equities and better yield potential than traditional fixed-income products. “InvITs can be used as a diversification tool, especially for investors looking for an income and risk trade-off. The medium- to long-term perspective of three-five years provides investors an opportunity to enjoy the stability of distribution as well as incremental upside from scale-up or acquisitions of assets,” says N. Amrutesh Reddy, Director of NDR InvIT.

However, investors must conduct their own due diligence before investing. Crucially, past performance cannot be the sole criteria for investment decisions.

Investors must recognise that an InvIT is not a single operating entity but a multi-layered structure comprising various entities involved in owning, managing, and overseeing assets and cash flows. This layered structure, while efficient, introduces additional complexity and potential points of failure.

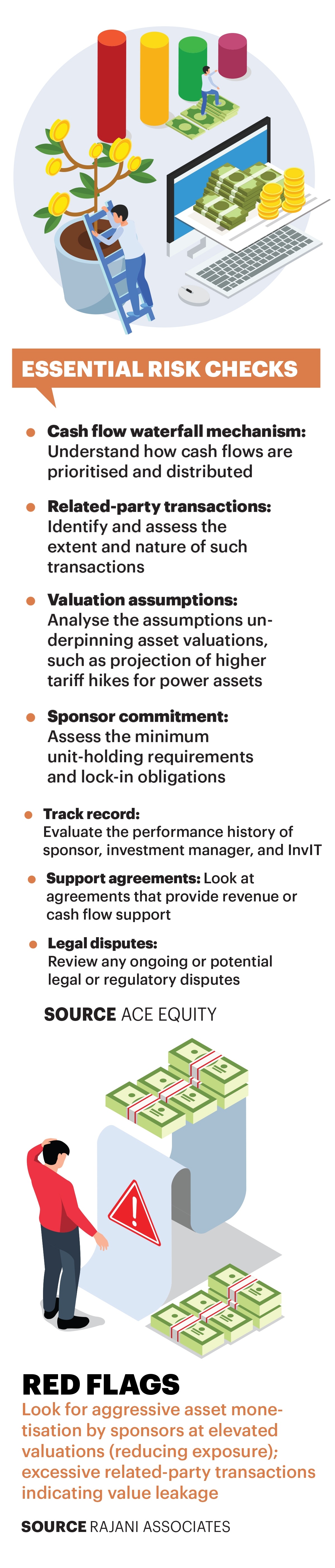

“Keeping that in mind, retail investors should undertake due diligence on aspects such as the cash flow waterfall mechanism, that is, understanding how cash flows are prioritised and distributed to different stakeholders; sponsor commitment, including minimum unitholding requirements and lock-in obligations; and support agreements that may provide revenue or cash flow backing,” says Parwani.

A cash flow waterfall is a structured system that allocates incoming cash in a fixed order—first expenses, then debt obligations, followed by reserves, and finally investor payouts.

In addition, investors should evaluate the track record of the sponsor, the investment manager, and the InvIT itself where applicable, while also assessing related-party transactions (RPTs) to understand the nature of dealings with connected entities. In the case of InvITs, this would mean the trust dealing with its own group entities. Investors should watch these closely, as unfair pricing or excessive fees can reduce returns.

It is equally important to analyse the assumptions underpinning asset valuations and review any ongoing or potential legal or regulatory disputes that may impact performance.

Careful evaluation of these factors enables investors to identify red flags such as aggressive asset monetisation by sponsors at elevated valuations while simultaneously reducing their own exposure. Similarly, excessive related party transactions (RPTs) may indicate a risk of value leakage from unit holders.

“Investors who combine a clear understanding of regulatory safeguards with thorough due diligence and ongoing monitoring are better positioned to make informed decisions and manage risks,” says Parwani.