Don’t look for the needle in the haystack. Just buy the haystack.” John C. Bogle, the founder of Vanguard and inventor of the index fund as we know it, famously said once.

What he meant is simple. Instead of trying to pick individual winners and looking to beat the market, own the entire market through index funds.

Mumbai-based Parth Parikh, 37, who works in the fintech and investment space, seems to have heeded that advice. He keeps a core part of his portfolio in broad market exchange-traded funds (ETFs) like S&P 500 ETF, Nasdaq 100 ETF, and even some exposure to Vanguard Total World Stock ETF. “These give me diversification and keep me aligned with global market growth,” he says.

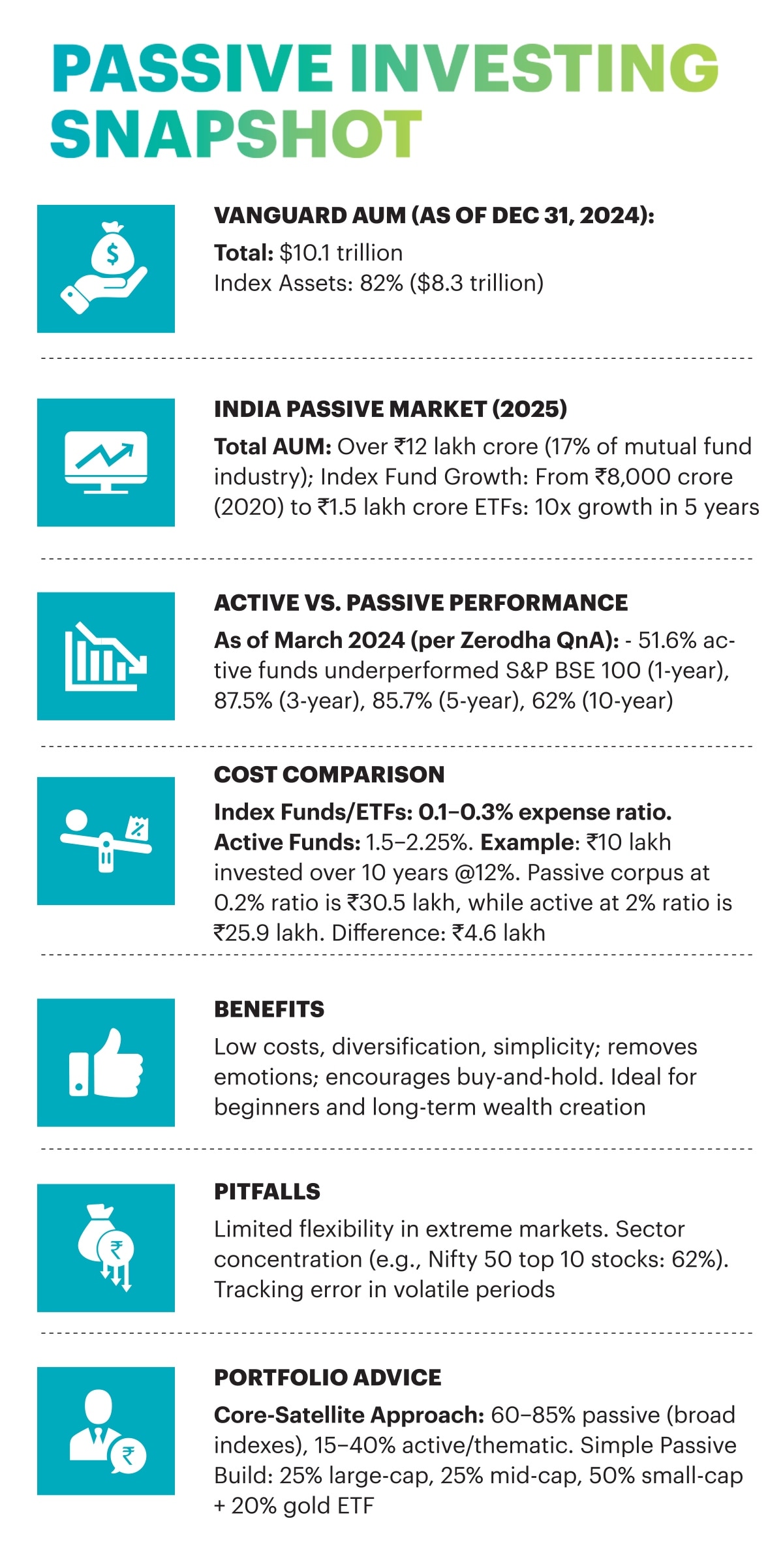

Parikh’s is not an isolated view. Index funds and ETFs have assets of over Rs 12 lakh crore in India and have grown to account for 17% of the total mutual fund industry.

In fact, though passive products have been in India for nearly 25 years, they have seen exponential growth in the past five years. In 2020, index funds had AUM of Rs 8,000 crore. Today, it is Rs 1.5 lakh crore. ETFs have grown tenfold in the same period. It’s clear that retail and institutional investors alike have jumped on the passive bandwagon.

And for good reason. As India’s economy accelerates despite global headwinds, passive investing continues to captivate retail investors, who are weary of market turbulence and favour set-it-forget-it approaches. Besides, with the proliferation of digital platforms, investors are exploring passive options like index funds and ETFs that reduce the need for constant portfolio monitoring. In fact, in September the addition of passive accounts, including index funds, ETFs and funds of funds, outpaced that of active equity schemes for the first time in India.

However, that wasn’t always the case. For years, active funds looked good because they were benchmarked against price indices, which ignored dividends. That gave an illusion of outperformance. Once the capital markets regulator Securities and Exchange Board of India (Sebi) mandated total return index (TRI) benchmarking in 2017, the picture changed. A TRI is a better measure of wealth creation since it captures both price appreciation and dividends earned from the underlying stocks.

And when you compare active funds on that basis, very few consistently beat the benchmark. An August 2025 Value Research study of 26 active large-cap funds with over 10 years found that only nine outperformed the BSE 100 TRI, which delivered an average five-year annualised return of 15.5%.

Low Costs

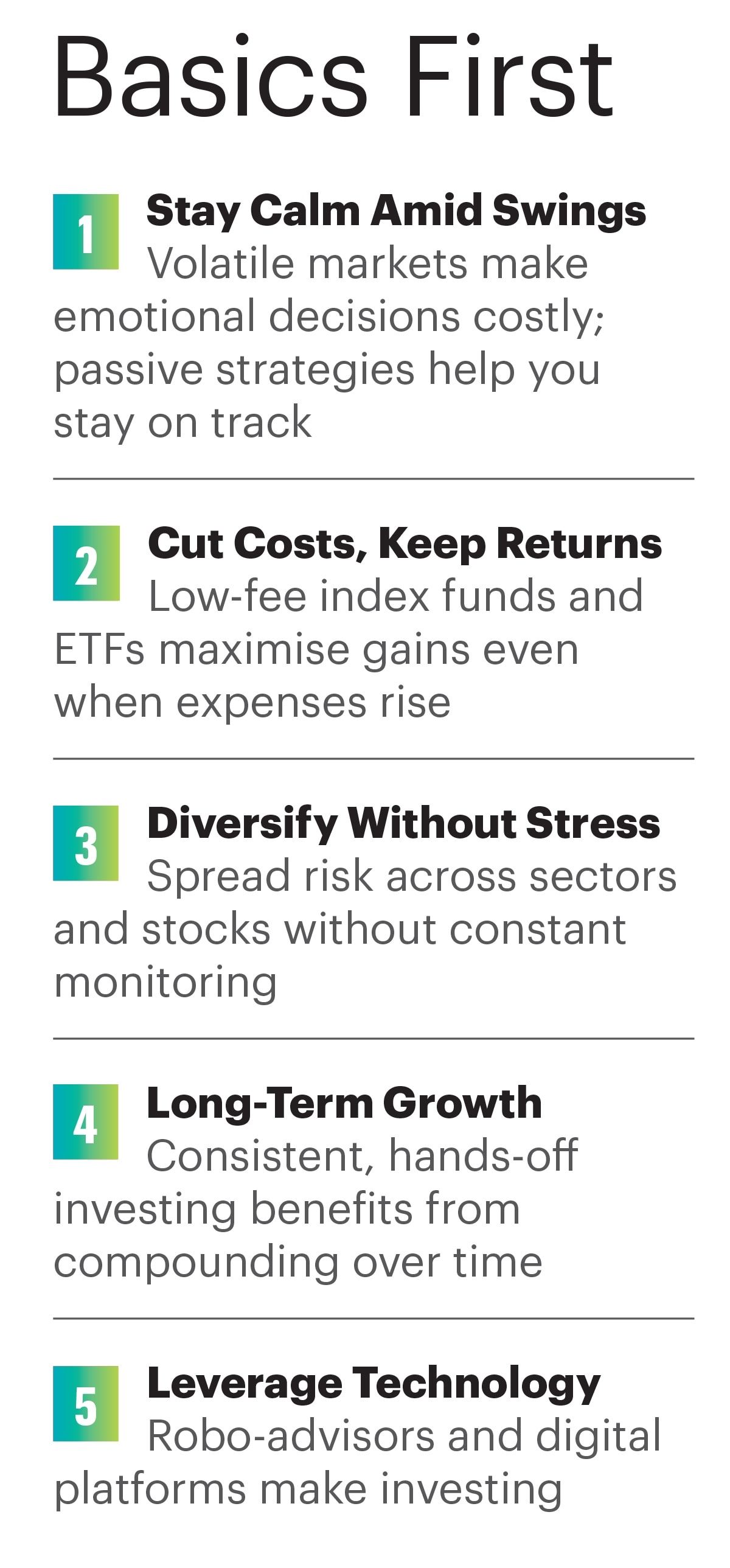

Investors opting for passive funds should realise the numbers game. “As cost and diversification impact the portfolio’s returns and risk, passive funds provide investors an opportunity to get market returns from a diversified set of stocks at very low cost,” says Abhishek Kumar, a Securities and Exchange Board of India (Sebi)-registered investment advisor (RIA), and founder and Chief Investment Advisor of SahajMoney, a financial planning firm.

Index funds are among the lowest-cost products. This is because they simply track a benchmark like the Nifty 50 or Sensex. They don’t require stock selection. As a result, their expense ratios are typically in the 0.1–0.3% range. Actively managed equity funds, on the other hand, employ fund managers and research teams to outperform the benchmark, and their expense ratios usually fall between 1.5–2.25%. This may look small, but compounds substantially over time.

For example, if you invest Rs 10 lakh for 10 years and the fund earns 12% annually before costs, an index fund with a 0.2% expense ratio would deliver about 11.8% net returns, and the investment would grow to about Rs 30.5 lakh. In an active fund with a 2% expense ratio, it would yield about 10% net returns, and the investment would grow to Rs 25.9 lakh.

Keep it Simple

“Passive investing brings simplicity to the investment journey. It’s cost-efficient, easy to understand, and perfect for first-time investors who might be intimidated by complex fund strategies,” says Vishal Jain, CEO of Zerodha Fund House.

Instead of analysing fund managers or chasing past performance, anyone can start by picking a top 100 or top 250 index fund and begin participating in the market.

For someone new to investing, passive funds remove complexity. “You don’t need to worry about fund manager philosophies, past returns, or NAV churn,” says Jain.

“In effect, passives allow the investor to tap into India’s structural growth while curbing emotional decision-making, helping them stay invested through cycles,” says Chintan Haria, Principal–Investment Strategy, ICICI Prudential AMC.

Stress Free

The beauty of passive is that it lets you build a diversified portfolio with minimal effort. For example, by allocating across large-, mid-, and small-cap index funds, an investor can cover the top 500 companies in India. “Add a small allocation to a gold fund or ETF, and you have a portfolio that is simple, balanced, and easy to track,” says Jain.

For Parikh, passive investing is about peace of mind. He does not have to check stock prices every day or worry if he is missing out on the “next big stock.” “The biggest advantages are low fees, diversification, and the fact that they take emotions out of investing,” he says.

Coming back to Bogle, he had said that the two greatest enemies of the equity fund investor are expenses and emotions. We have looked at expenses and now we look at the emotional bit.

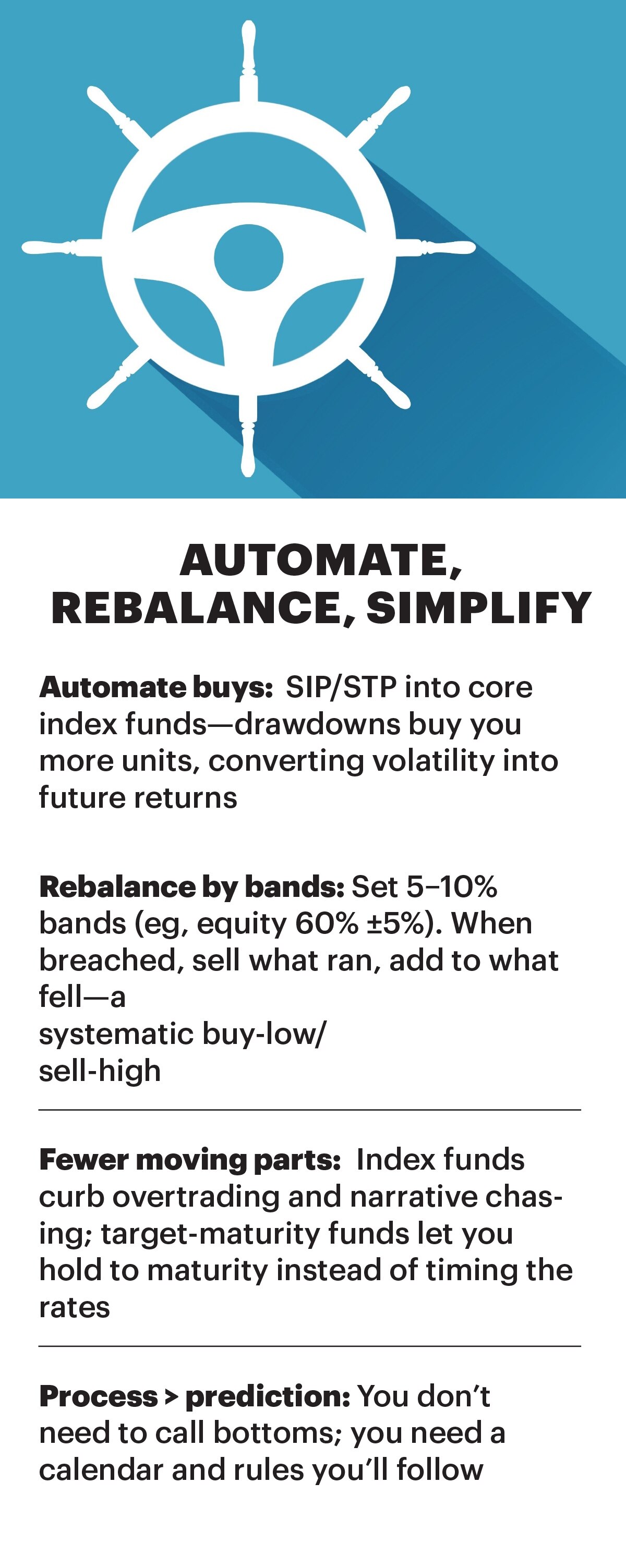

“Passive investing follows a rules-based approach (such as tracking an index), which discourages investors from reacting emotionally to market swings,” says Aditya Agarwal, Co-Founder, Wealthy, a wealth-tech platform.

It also requires long-term commitment and rewards those who stay invested over medium to long durations with focus on a buy-and-hold strategy.

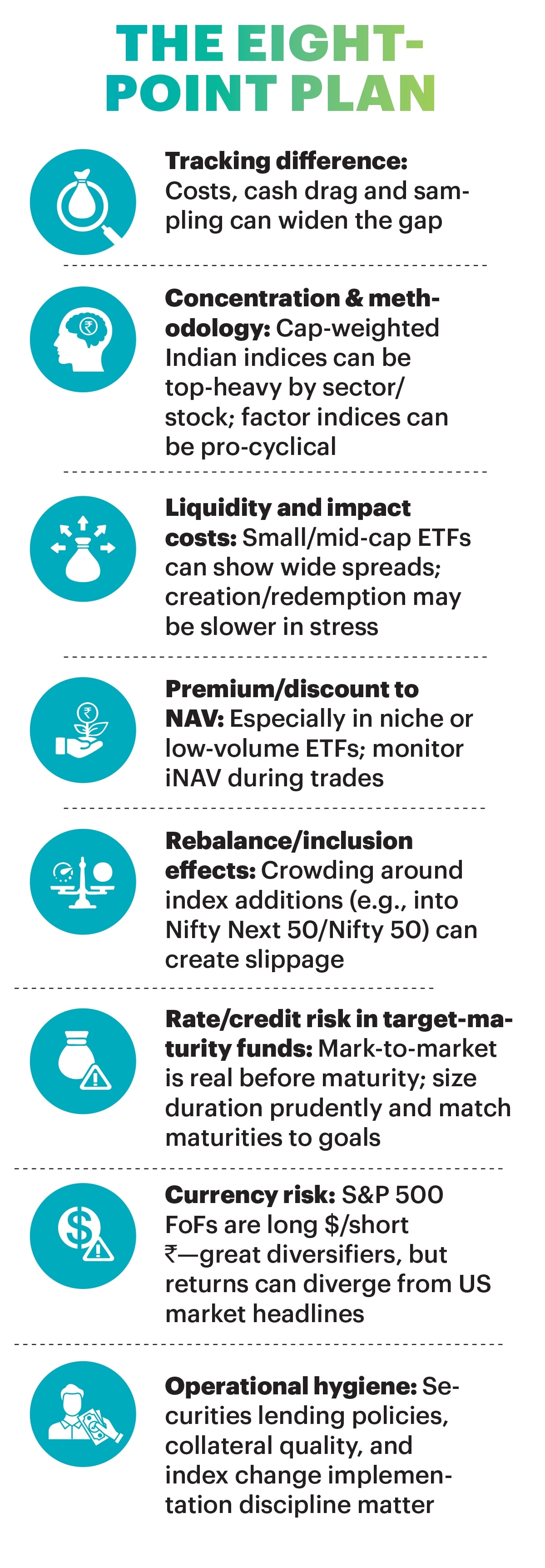

Passive Pitfalls

Every investment comes with its own set of risks. “With passive, there is often limited flexibility during extreme market conditions, and investors may also miss out on opportunities that active stock selection can offer,” says Agarwal.

Some investors may not conduct a thorough analysis of whether it matches their goals or risk appetite.

Another risk is that of sector concentration. “In the Nifty 50, the top 10 stocks now make up over 62% of index weight, exposing passive investors to shocks (if any) in those names,” says Vikash Wadekar, Head of Passive Business at Axis Mutual Fund. Many indices, such as the Nifty50, are heavily skewed towards sectors like BFSI and IT.

Tracking error can cause passive funds to deviate from index performance, especially during volatile markets or due to fund expenses.

Index Play

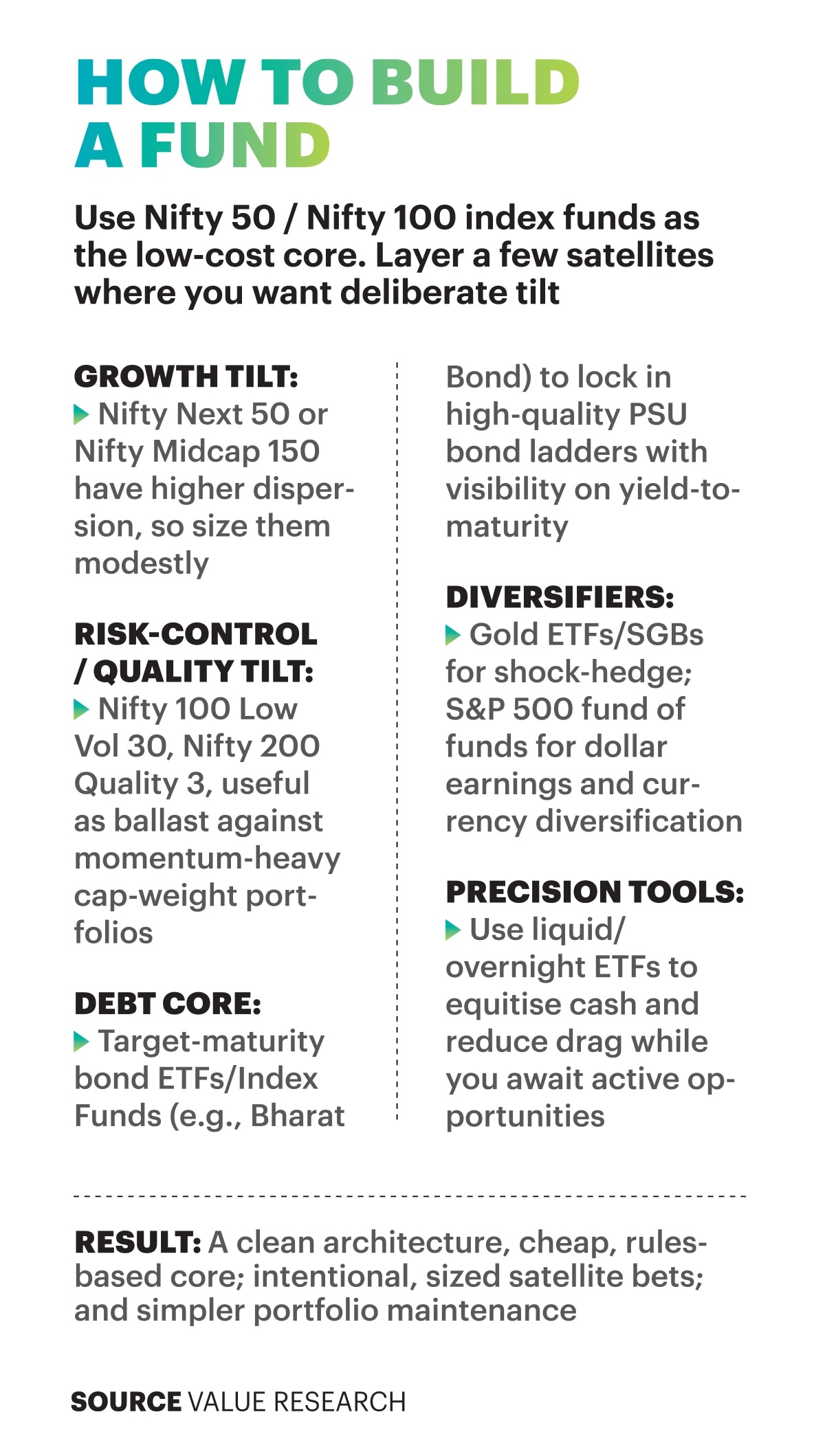

Whether you invest in a large-cap active or passive fund, your underlying exposure is equity. The risk doesn’t change. The only way you can cushion your portfolio is by diversifying across asset classes. If you have equity, gold, and some debt, you protect yourself. “Passive is the easiest way to build such a portfolio,” says Jain.

If you were building a passive portfolio, the easiest way is to invest 25% in a large-cap, 25% in a mid-cap, 30% in a small-cap index fund. Then add maybe 20% in a gold ETF to diversify.

But your investment strategy should be a mix of active and passive. “Investing in broad-based passive funds with low-cost fee structure combined with active funds from exceptional managers is what one should aim for,” says Rohit Beri, CEO & CIO, ArthAlpha, an AI-driven investment firm.

A core-satellite approach works best for balancing risk, growth, and oversight. “The core of the portfolio can be built with low-cost passive index funds or ETFs, providing broad market exposure, cost efficiency, and long-term stability,” says Himanshu Srivastava, Principal Analyst, Morningstar Investment Research India.

Around this, investors can add a satellite component consisting of actively managed funds, thematic strategies, or alternative assets to capture alpha opportunities and participate in emerging trends. “This allows investors to keep costs low, benefit from steady market-linked returns through the core and use the satellite portion for tactical plays and growth opportunities, ensuring a well-diversified and resilient portfolio,” says Srivastava.

“For me, I would do 85% core and 15% satellite. Someone more aggressive may do 60–40. The problem otherwise is people end up with 30–40 entries in their DEMAT account, with no control, and in bad times they’re down 50% while the index is down 20%,” says Jain.

Dhirendra Kumar, Founder & CEO, Value Research, an independent investment research firm, sums it up best: “Cost is certain, alpha is not. Treat passive as the default, not the afterthought.”