"I am an irrepressible optimist, but I always base my optimism on solid facts”

- Shaktikanta Das quoting Mahatma Gandhi in June 2021 after the MPC policy statement.

Sixty-nine-year-old Shaktikanta Das landed at the Reserve Bank of India (RBI) in December 2018 like a new batsman walking in after a sudden batting collapse. The pitch was unpredictable; there were visible rough patches from the recent default of non-banking financial company IL&FS.

His predecessor, Urjit Patel, an economist and outsider, had resigned in a huff nine months before his term was to end. Before Patel, another independent economist, Raghuram Rajan—an appointee of the Congress-led UPA government—had made a quiet exit, returning to academia after completing his three-year term.

During those two tenures, the relationship between the RBI in Mumbai and the finance ministry in Delhi had become increasingly strained. It was up to Das to read the conditions, boost the confidence of the RBI’s top brass, and rebuild the relationship with the government. A 1980-batch IAS officer of the Tamil Nadu cadre, Das arrived with a reputation for working seamlessly across political dispensations, having served finance ministers from both the UPA and the BJP.

Reflecting on the transition, he explains that the years in public service prepared him to step into new responsibilities at a very short notice. “The key is to begin functioning without overthinking,” he says. Das compares the experience to a batsman: think too much about the next delivery, and the ball would have passed by you and hit the stumps.

Over his six-year tenure, the relationship with the government remained smooth. What did the 25th RBI Governor do differently? Das admits that differences of opinion between the finance ministry and the central bank are natural, given their distinct responsibilities and priorities. “Such differences, however, are best resolved through direct and internal discussions rather than through the media,” Das tells BT at the PMO’s South Block office. Das became Principal Secretary to the Prime Minister after his RBI tenure.

The NBFC Crisis

Just months before Das took charge, IL&FS—one of India’s largest NBFC groups—began defaulting on its obligations, triggering a broader liquidity shock. In 2019, the RBI superseded the board of another NBFC, Dewan Housing Finance Corporation.

His first task was restoring normalcy, infusing liquidity and, above all, building back confidence. In one press conference, Das went so far as to say it would be the RBI’s endeavour to ensure that no NBFC of reasonable size failed. Afterwards, his Deputy Governors told him he had made a very big promise and “stuck his head out.” He replied, “Yes, I have stuck my head out, but you have to make sure my head is protected,” grins Das.

“By emphasising stronger governance, risk management, and capital discipline, Das had made NBFCs more stable while still ensuring that credit reaches underserved economic segments. His leadership balanced caution and practicality, greatly enhancing the long-term stability and reputation of India’s NBFC sector,” says Mehul Pandya, Managing Director & Group CEO at CareEdge.

That was visible in the years that followed. In 2020, the RBI imposed a moratorium and forced the reconstruction of YES Bank. It also placed a moratorium on Lakshmi Vilas Bank in 2020. The RBI stepped in again, superseding the boards of SREI Infrastructure Finance and Reliance Capital, and appointing an additional director at RBL Bank as part of a supervisory intervention.

Das built a knack for unconventional resolutions. Unlike past practice of a stronger bank acquiring a bank in crisis, the YES Bank resolution was unique in that it was reconstructed using private capital, led by State Bank of India and a consortium of private banks and financial institutions. “We did not want to burden a single PSB, so the resolution had to be led by multiple banks,” underlines Das.

The Lakshmi Vilas Bank–DBS merger, in 2020, was also a path-breaking shift in RBI’s resolution playbook—a foreign bank was allowed to acquire a private bank. “We reached out to all Indian private sector banks, including DBS Bank, which had set up an Indian subsidiary. They showed strong interest, and we were confident about DBS’s strong parentage and deep pockets,” recounts Das.

There were other measures too, like introducing funding access for NBFCs and liquidity risk management frameworks. The RBI divided NBFCs into four groups based on size from a base layer to systemically important ones. It was a structural shift, with large NBFCs regulated almost like banks.

The Covid Crisis

Just as the RBI was getting on top of the NBFC crisis, the pandemic struck in March 2020. “That was the beginning of another period of crisis of a completely different nature,” recalls Das. There was a serious risk of getting engulfed in a systemic crisis. Das had to ensure that banking, payments, money markets and credit flows continued even as the economy came to a standstill.

There were few historical parallels and no playbook to rely on. The RBI had to prioritise financial stability, liquidity, and boosting confidence—often ahead of short-term growth considerations.

“Das’s monetary policy actions, including interest rate cuts and targeted liquidity injections, not only ensured credit flow to key sectors like real estate but also helped stabilise inflationary pressures amidst global uncertainties and geopolitical tensions,” says Niranjan Hiranandani, Chairman of the real estate major Hiranandani Group.

When asked about those unconventional measures, Das jokes, “Leave something for my book.”

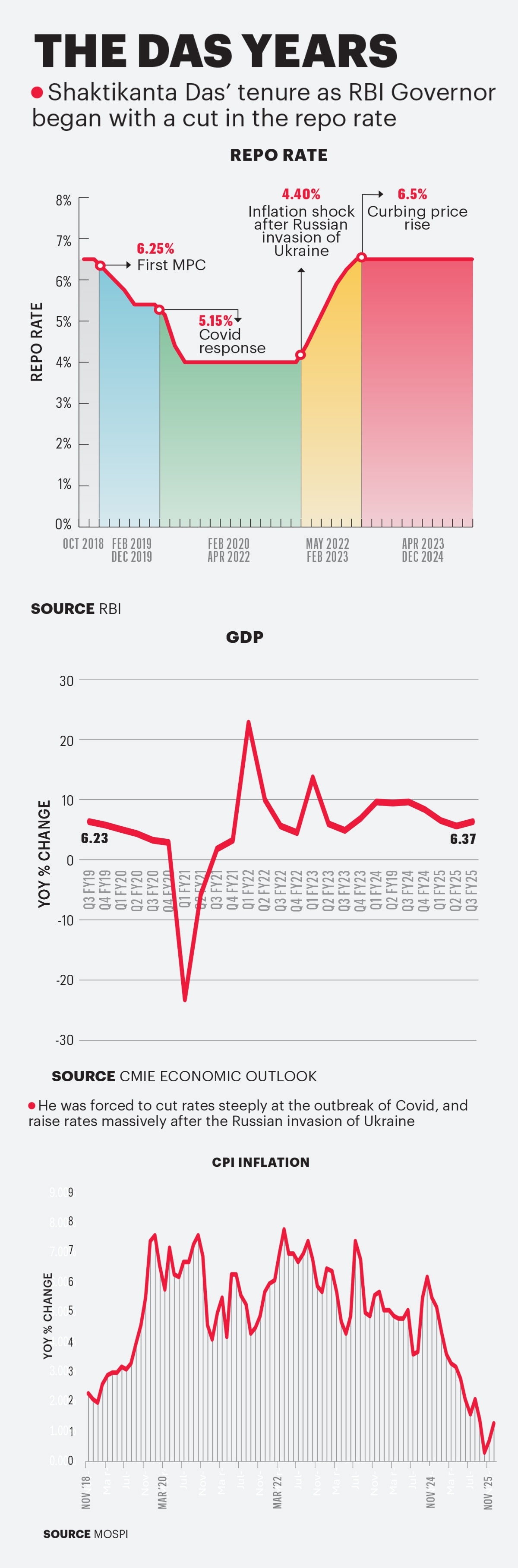

Inflation vs Growth

As the Covid waves seemed to be ebbing and domestic growth was rebounding, a series of global shocks triggered by the war in Ukraine threatened to upend the system once again. The US Federal Reserve tightened monetary policy aggressively in response to the inflationary spike after the invasion, a situation worsened a year later by the Israel–Gaza conflict. Spikes in global food and crude oil prices added to the complexity, turning monetary policymaking particularly challenging.

“Every day turned into an exercise in anticipating where the next challenge might emerge. The only way forward was to stay proactive, prepare for every possible risk, and build resilience strong enough to withstand whatever came next,” observes Das.

The situation called for close coordination between the RBI and the government. The RBI focused on anchoring inflation expectations and managing demand through monetary policy, while the government addressed supply-side pressures.

“I do not see growth and inflation as conflicting objectives. For long-term growth to be sustainable, inflation must remain under control. High inflation erodes people’s purchasing power and, over time, discourages investment,” says Das.

Building Buffers

Scarred by the crises Das inherited, the RBI focused on strengthening India’s resilience to external events. It built up foreign exchange reserves to around $700 billion by the end of his tenure, with an increase of nearly $65 billion in 2024 alone—second only to China among major reserve-holding economies. This allowed the RBI to manage external shocks while ensuring the rupee was among the most stable emerging-market currencies.

The payoff was evident after the Russia-Ukraine war: despite outflows, there was no panic. “The market knew the RBI was sitting on a pile of reserves and that India could meet its external payment obligations,” he adds.

The RBI pursued a calibrated approach. It curbed excessive volatility in the rupee while allowing a gradual, orderly depreciation to preserve export competitiveness.

A key element of this strategy was diversification. After a long pause following the 2011 IMF gold purchase, the RBI resumed buying gold in December 2018; it has since added steadily. Gold, viewed as a long-term hedge against global uncertainty, became an integral part of reserve deployment. From its gold reserves held abroad, the RBI bought 100 tonnes of gold in 2023 and another 100 tonnes in 2024. It felt there was no need to keep such large quantities abroad, beyond a minimum buffer. It repatriated a portion to India, given the country's storage capacity.

Beyond UPI and digital-payment initiatives, the RBI moved ahead of many advanced economies in exploring a central bank digital currency (CBDC). It launched a pilot, with the e-rupee made interoperable with UPI. “We wanted to be among the pioneers—ready early rather than starting after others had already moved ahead,” he says.

A Tough Central Banker

During Das’s tenure, the RBI signalled a shift towards tough regulatory enforcement. There were unprecedented actions against banks, card networks, NBFCs, and fintech firms. The message was clear; compliance is non-negotiable, and customer interest is paramount.

Das also simplified the central bank’s messaging, making complex monetary policy concepts more direct, accessible, and understandable to the wider public. The idea was to demystify monetary policy and other regulatory actions.

With the distance of time, his six-year innings looks steady and well-managed. Das—the second-longest serving Governor after Benegal Rama Rau—faced bouncers, swing, and was constantly under pressure, yet remained calm and guided the economy through some of its toughest phases.

@anandadhikari, @szarabi