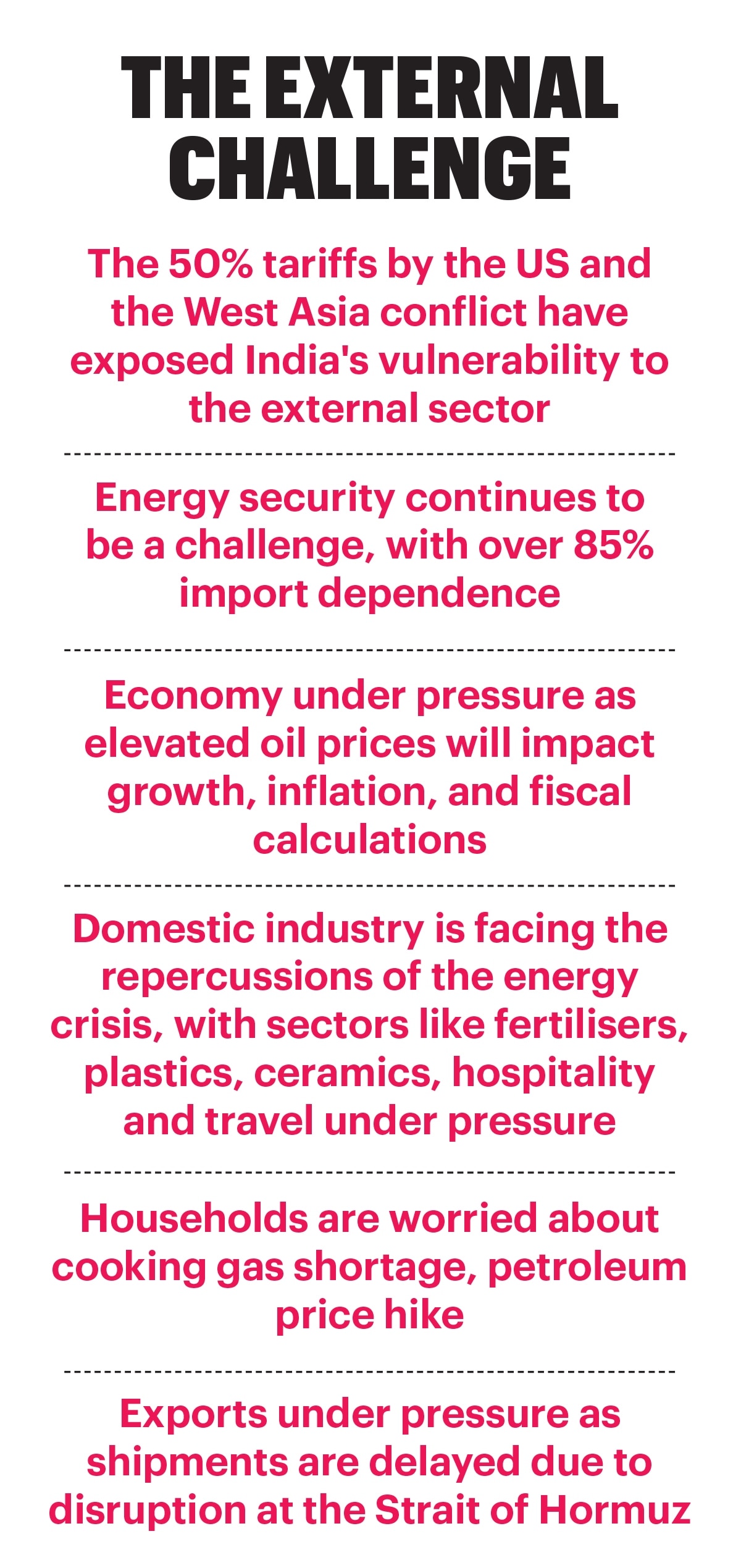

Commerce secretary Rajesh Agarwal s a worried man. The reason: The flare-up in West Asia. Starting off the monthly trade meeting in mid-March, he noted, “One challenge got over, the other started.” He was referring to the conflict in West Asia, which has impacted India’s trade, about a year after reciprocal tariffs imposed by the US, which have since been struck down by the Supreme Court there. While Agarwal was highlighting the challenges for exports, his words also ring true for the entire economy.

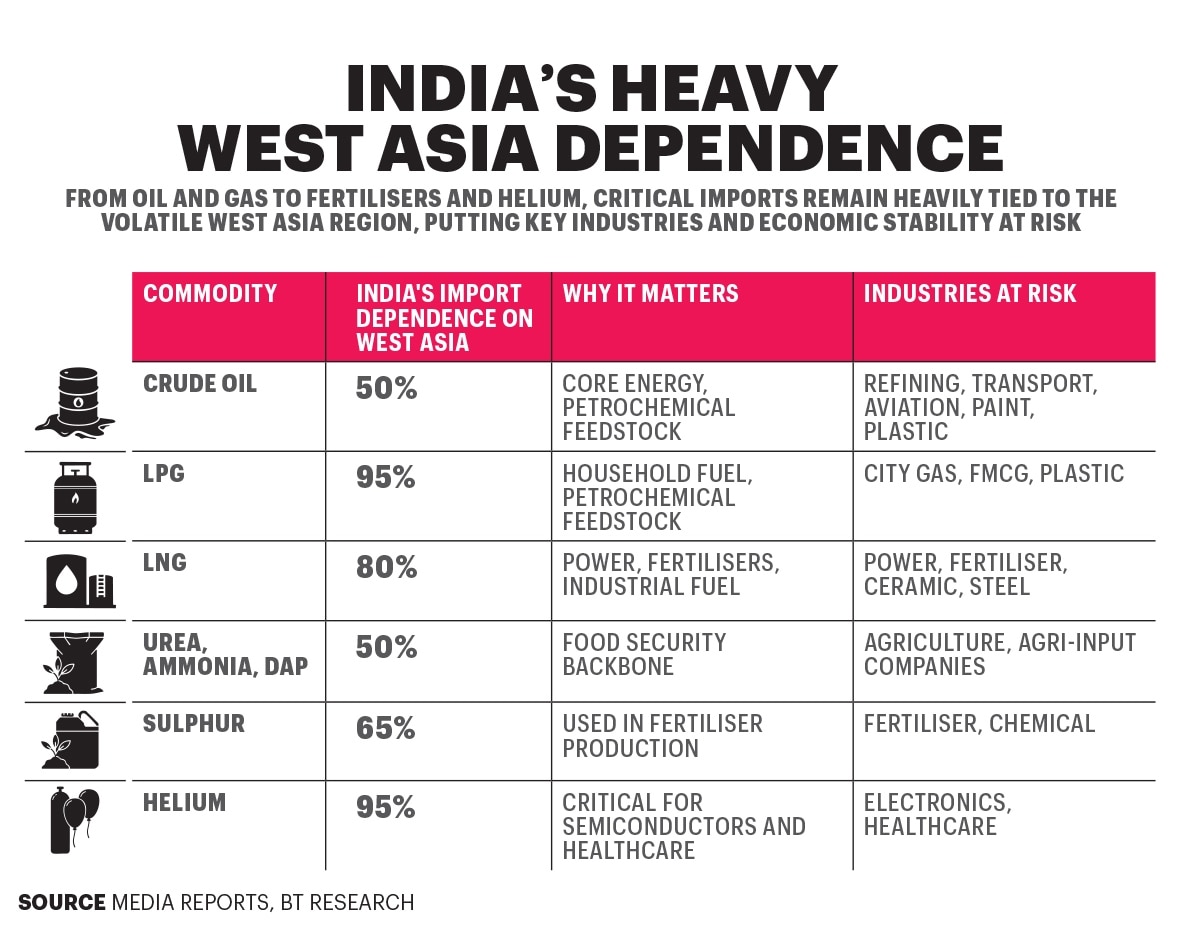

The war between the US-Israel alliance and Iran is creating not just ripples but supply shocks across the world. For India, too, it’s turning out to be a big concern. The country imports over 88% of its crude oil requirements, of which about 55% comes from West Asia. The crucial Strait of Hormuz, through which 20% of the world’s crude oil passes, has been closed, with Iran allowing only a few ships to pass, creating a chokepoint for oil and gas supplies to India as well as exports from India to West Asia, North America and Europe. Attacks at several oil and gas production facilities in the Gulf region have squeezed supplies further.

Rahul Kapoor, Global Head, Shipping and Metals, S&P Global Energy, says the effective closure of the Strait is a black swan event for energy markets with significant impact on both crude and LNG flows. “The escalation in West Asia puts the key oil chokepoint, Strait of Hormuz, at the centre of global geopolitics. Shipping and energy markets are signalling that a prolonged disruption risk is undoubtedly significantly higher than at any point in decades,” he says. Less than 10 vessels are crossing the Strait every day since March 2 compared to an average 135 in February, says S&P.

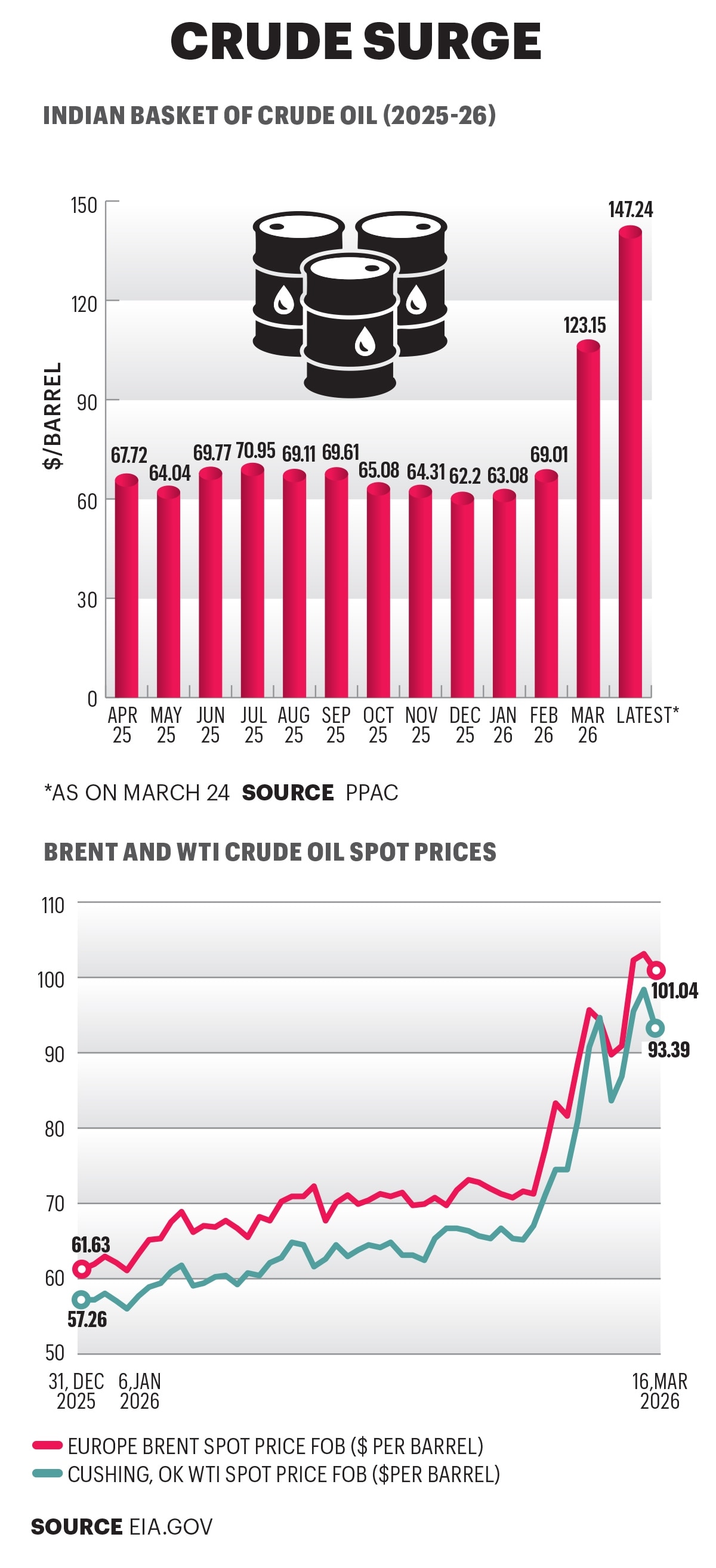

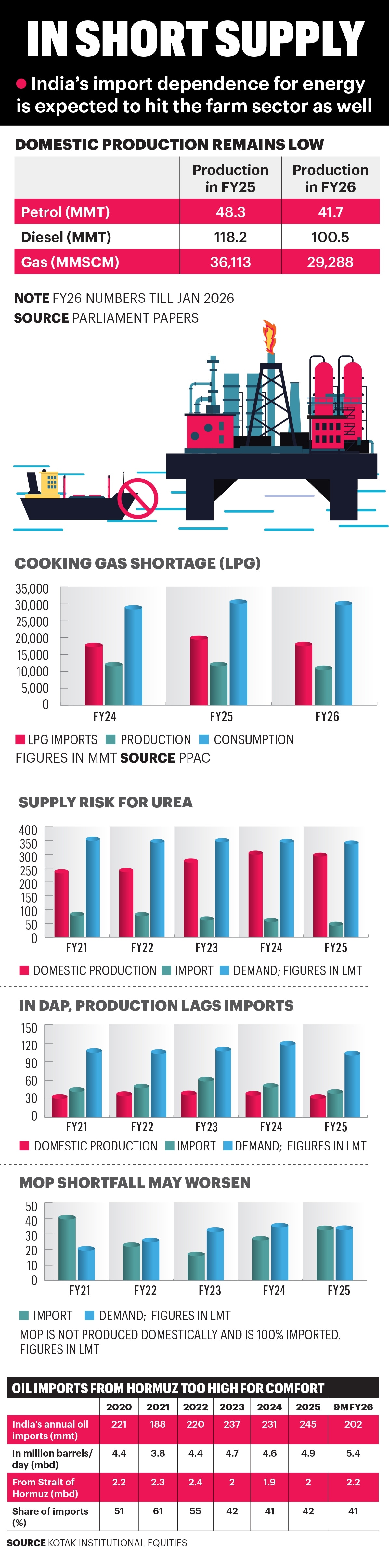

The repercussions for the Indian economy became clear just days after the start of the war on February 28. As the war went on, the Indian basket of crude oil surged to $157.04/barrel on March 23, from just $62.2 in December 2025. The crisis has also disrupted LPG and LNG imports. About two-thirds of India’s LPG needs are met from outside, mostly West Asia. India also meets nearly 50% of its natural gas requirements based on LNG imports out of which nearly 60% comes through the Strait of Hormuz. Following diplomatic discussions, though, some ships have been allowed to reach India.

The Fallout

The shortage of cooking gas has forced the government to come out with directives to ration its usage. Several restaurants have closed or are doing partial business. Crowd-pleasers like bhaturas, dosas, samosas, and even tea, are either off the menu or seeing a rise in prices. Households are hoarding cylinders and induction cooktops are flying off the shelves as families worry about empty cylinders.

There are also concerns over the availability of fertilisers ahead of the kharif season. India imports about a third of its fertiliser requirement; West Asia supplies close to 40% of it, apart from several other inputs, including rock phosphate, phosphoric acid and muriate of potash.

This is not all. Second and third order effects are being felt in sectors ranging from paints and chemicals to tyres and air-conditioners. The supply of Helium, a large part of which comes from Qatar, has hit industries such as semiconductors. Steel and aluminum prices are rising and coal, which is becoming a favourite alternative fuel in kitchens, has become costlier. Even plastic required for packaging is in short supply.

Travel and airline services have been disrupted. Remittances from India’s near 10-million-strong diaspora in the Gulf could fall. And factories have been told to ration gas supplies and reduce production.

Energy sector expert Dinesh Sarraf, the former Chairman-cum-Managing Director of ONGC and former Chairperson of the Petroleum and Natural Gas Regulatory Board, says the energy shortage will be felt differently across segments.

“This is the biggest challenge for India. LPG is a byproduct of crude oil; and just 4-5% of crude processed becomes LPG. While India is surplus in refining crude oil, domestic production of LPG is just about 35% of our requirements,” he says. About 90% of our LPG is consumed by households. To make matters worse, almost 90% of our LPG imports come through Hormuz, though India is now diversifying LPG sourcing.

In LNG and natural gas, about 50% is domestically produced. Of the imports, 60% pass through the Strait. Gas supply to urea plants is likely to be curtailed, but for now, India has adequate urea stocks, he says, and Indian urea producers have advanced their annual maintenance. “I don’t think urea will be an immediate concern unless the war continues for long,” he says. But gas-based petro-chemical industries will be hard-pressed, he warns.

India’s reliance on imports for crude oil is well known, and while India has largely diversified its supplies in recent years, West Asia still caters to a substantial chunk of our resources, he says.

For now, the economic fallout of this crisis is somewhat contained in the short term, but if the war gets prolonged, all bets will be off. “We have improved our economic resilience and are in a much better situation that in the past due to our policy choices. Economic growth is robust, fiscal and current account deficits are contained, inflation is low and bank balance sheets are much stronger today,” says DK Joshi, Chief Economist, Crisil, pointing out that even with the US tariffs, the Indian economy performed much better with an improved growth-inflation mix. GDP is estimated to grow 7.6% in FY26 and between 7.1% and 7.4% in FY27.

Joshi says the impact of the conflict on GDP growth in the fourth quarter of FY26 will be marginal given that it started on February 28. “Inflation and industrial production data will have to be monitored for March,” he says.

However, several agencies have begun scaling down India’s GDP estimates. Goldman Sachs has lowered India’s GDP growth forecast for 2026 to 5.9%, from 7% before the conflict. Emkay Global Financial Services has trimmed its FY27 GDP growth estimate by 0.4 percentage points to 6.6% and raised inflation and current account deficit estimates to 4.3% and 1.7%, respectively.

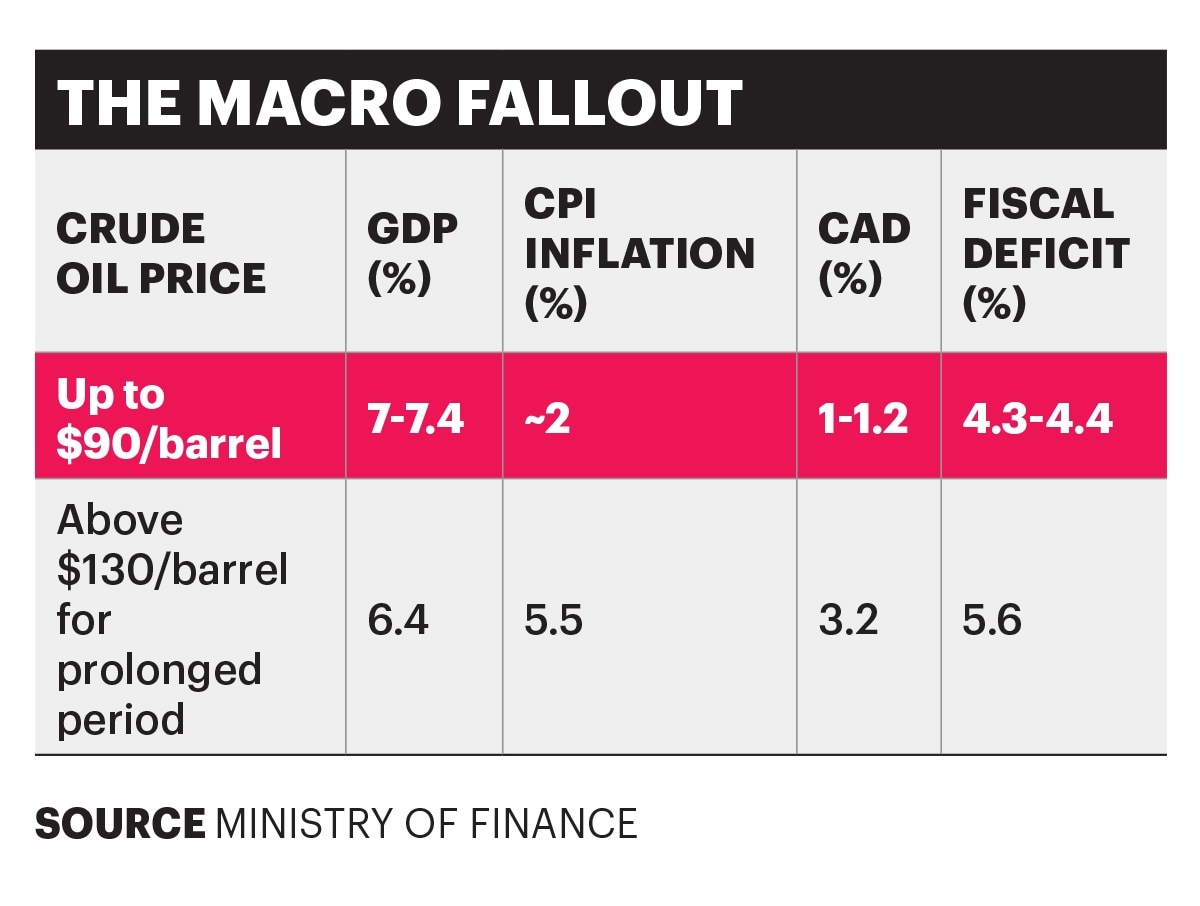

The finance ministry, while seeking Parliamentary approval for Rs 57,381 crore towards a Rs 1 lakh crore Economic Stabilisation Fund, remains confident that in the short term, the conflict and rising oil prices will not impact the economy. As per an internal analysis, the ministry believes that crude oil prices at $90 per barrel will not have a significant impact on the economy. But oil at $130 per barrel for two to three quarters would shave off 100 basis points from GDP growth and push up inflation.

“At $130 dollar per barrel, if the price of oil remains at that level for two-three quarters, the macroeconomic impact will be significant. CPI inflation will rise towards 5.5%. Real GDP growth will decrease from 7.4% to 6.4%. The current account deficit will increase from 1.2%, where we currently are, to around 3.2%. The fiscal deficit may rise from 4.4% to 5.6%,” Chief Economic Adviser V. Anantha Nageswaran recently informed the Parliamentary Standing Committee on Finance.

According to RBI estimates, if crude oil prices are higher by 10% than the baseline, and assuming full pass-through, inflation could rise by 30 basis points and growth dip by about 15 basis points. For now, there are no plans to hike fuel prices, which observers note could also be due to the upcoming assembly elections in five states. LPG prices have been hiked by Rs 60 for a 14.2-kg cylinder. Then, on March 21, oil companies raised the price of industrial diesel by 25% and of premium petrol by Rs 2 per litre.

Exporters are also bearing the brunt of the closure of the Strait of Hormuz. Shipments of items ranging from basmati rice, fruits and vegetables to textiles and diamonds are either being sent back or getting stuck. The Department of Commerce on March 19 rolled out a Rs 497 crore package for consignments to countries in the region.

Policy Pivot

Almost all experts agree that the crisis calls for a policy pivot by India to ensure greater energy security for a country that hopes to become developed over the next 20 years.

India’s strategic petroleum reserves can last for about 74 days; about 5.33 million tonnes are held underground. The government has also approved two new strategic petroleum reserves at Chandikhol in Odisha and Padur in Karnataka. These are yet to become operational.

Ausaf Sayeed, former Secretary, Ministry of External Affairs and former Ambassador to Saudi Arabia, Yemen and High Commissioner to Seychelles, underlines the need to build strategic reserves and diversify oil supplies. “While we have diversified actively, making Russia our largest supplier and scaling up volumes from the US, Nigeria, West Africa, and Latin America, West Asia remains our primary source. Despite logistical and sanctions-related hurdles, Russian crude oil has served as an effective buffer, complemented by rising imports from Guyana, Nigeria, and other non-Hormuz routes,” he says. He calls for accelerating the build-up of Strategic Petroleum Reserves. “Phase I facilities hold 5.33 MMT of crude, with the UAE already storing crude at Mangaluru and offering to expand its participation. Constructive engagement with Saudi Arabia for Phase II—envisaging an additional 6.5 MMT at Chandikhol, Odisha (4 MMT) and Padur (2.5 MMT)— must be fast-tracked,” he says.

Equally critical is prioritising alternative connectivity corridors: reviving the India-Middle East-Europe Economic Corridor, completing the Chabahar–Zahedan rail link, and fully operationalising the International North-South Transport Corridor, he says.

Joshi of Crisil says India must work towards lowering energy dependence and improving energy security.

Sarraf underlines the wneed to invest more in oil exploration. “The government must improve policies to get more foreign expertise along with investment in the sector. We need more participation from foreign investors who are likely to have more capital and will undertake greater due diligence for potential oil and gas reserves.” He, however, says that strategic petroleum reserves have a cost, which will ultimately have to be borne by the consumer. “Storage capacity can always be created. But holding stocks worth, say, 200 days, will involve capital expenditure and inventory carrying costs, including the risks and rewards from oil price volatility. In a developed country, consumers can bear such costs, but in India, one must take price sensitivities into account,” he says.

The Centre has implemented measures to increase domestic crude production such as permitting up to 100% foreign direct investment in exploration and production. It is also using enhanced oil recovery methods in aging fields. But the results are yet to be seen.

Expansion of pipeline and city gas distribution networks has increased the use of natural gas and focus on renewable energy and electric vehicles have to some extent reduced the consumption of petrol and diesel. There is also work underway to improve LNG stocks.

None of these measures will provide solutions in the short term but building domestic capabilities in the long term would, especially at a time when Aatmanirbhar Bharat has become a clarion call for becoming self-sufficient in manufacturing. Policy nimbleness and reforms undertaken last year to offset the 50% tariffs by the US are a clear example of that.

@surabhi_prasad