Capital markets the world over are facing extreme volatility after the US-Israel alliance attacked Iran. Fresh fundraising has slowed. Banks remain cautious, keeping an eye on asset quality, even as they look to boost credit growth. All of this appears to have created ideal conditions for growth of private credit in India.

Private credit, or performing credit as some call it, is an instrument where a non-bank lender raises capital—from institutions like insurance companies, family offices, sovereign wealth funds, high networth individuals (HNIs) and ultra HNIs—that is then loaned to companies, often small and medium enterprises, at higher rates than those in the formal banking sector.

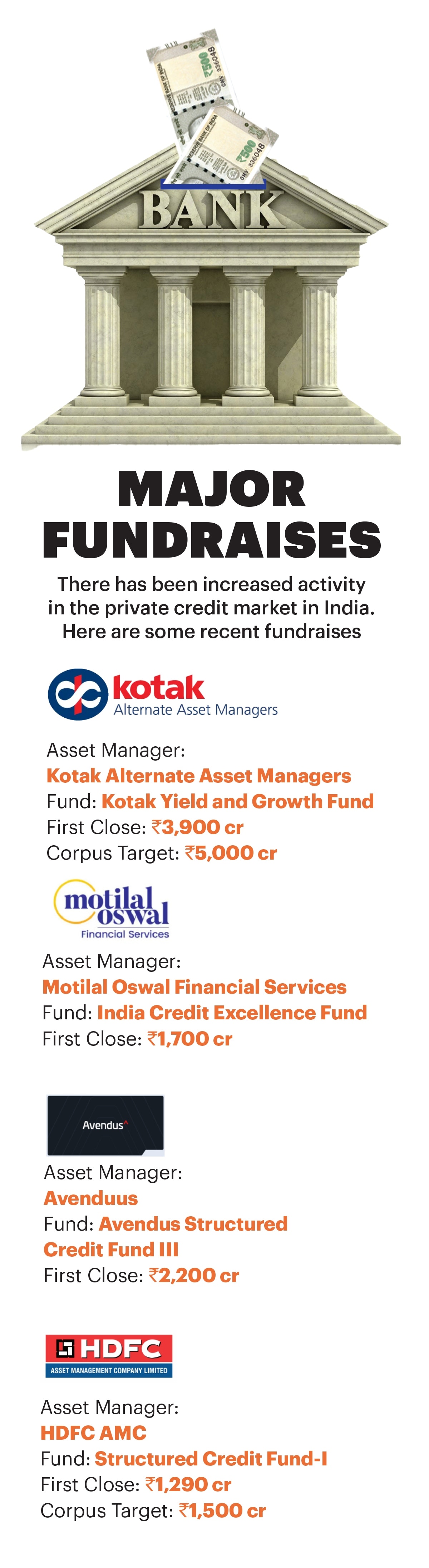

Sample this: In February, Kotak Alternate Asset Managers announced the first close of the Kotak Yield & Growth Fund, a category II Alternate Investment Fund (AIF) with a target of Rs 5,000 crore. The first close of Rs 3,900 crore was the largest private credit fundraise in India.

At the end of that month, the alternative investment arm of Motilal Oswal Financial Services marked the first close of its maiden private credit fund at Rs 1,700 crore. The India Credit Excellence Fund is targeting a corpus of Rs 3,000 crore.

More recently, Avendus secured commitments of Rs 2,200 crore for its Avendus Structured Credit Fund III. The target corpus is Rs 4,000 crore, a four-fold increase over Fund II, which was Rs 1,000 crore.

Elsewhere, International Finance Corp (IFC), a member of the World Bank Group, has signed an agreement to invest in HDFC Asset Management Company’s Structured Credit Fund–I, a category II AIF, to expand private credit to India’s mid-corporates. The fund got commitments of about Rs 1,290 crore out of the targeted corpus of Rs 1,500 crore. As an anchor investor, IFC would contribute Rs 220 crore.

Despite this growth spurt, India’s private credit market is quite small. The global private credit market is pegged at $3.5 trillion, according to The Alternative Investment Management Association (AIMA). In contrast, $12.4 billion was invested in private credit in India last year, 35% year-on-year growth, according to consulting firm EY. Real estate was the dominant sector, accounting for 42% of the total deal value, followed by healthcare and other industrial products, it said.

Crucially, this growth in the domestic private credit market comes against a bleak global backdrop, with funds in the US facing redemption pressures.

Market Growth

One reason for the recent uptick in the private credit market is the passing of the Insolvency and Bankruptcy Code (IBC) in 2016, says Srini Sriniwasan, Managing Director of Kotak Alternate Asset Managers. That, and the government’s proactive approach in amending the law to make it better, created an inflection point for private credit. “The credit environment, which includes the ability to recover your money, has changed,” he adds.

Plus, there is a structural opportunity in the country because of a persistent funding gap. “As banks stay selective and skewed towards higher-rated exposures, mid-market, cash-flow positive companies continue to seek customised, flexible capital for refinancing, capex and acquisitions,” Vishal Bansal, Partner, Debt and Special Situations at EY India, tells BT.

According to Bansal, the underlying need for private capital remains structural in India. As per a recent EY India survey, 55% fund managers expect $10–15 billion deployment in 2026, while 28% expect over $15 billion.

Sriniwasan says India’s banking industry is not large enough to meet the credit requirement of the economy in its entirety. To become a developed country, India will need other forms of lending like private credit. He pegs the non-bank credit requirement over the next five years at $150 billion.

“India has let the entrepreneurship genie out of the bottle, with newer entrepreneurs investing in hard assets, from electronics manufacturing to solar panels,” he says. Large businesses can raise money easily. “The new guys are getting crowded out by banks, which typically lend based on corporate or personal guarantees,” says Sriniwasan. Kotak Alternate Asset Managers is planning a third fund in its strategic situations fund series (KSSF III) this year, aiming to raise money from foreign investors, with a target of $2 billion. Separately, it is discussing a $300 million specialised fund specifically targeting the energy transition theme.

Private credit is neither long-term patient equity, nor long-term patient debt, says Rakshat Kapoor, Head and CIO–Private Credit of Motilal Oswal Alternates. It is an interim financing solution for one to three years.

The fund manager is focused on sectors like healthcare, pharmaceuticals, life sciences and the broader manufacturing theme. However, he is staying away from greenfield infrastructure development and many new-age technology businesses, says Kapoor.

“Ours is not an early-stage fund, so we are looking at more mature, established businesses,” says Kapoor.

Considering the needs of the economy, the strong deal activity in the space is not surprising. Last year, the Shapoorji Pallonji Group secured $3.1 billion private credit funding, in the largest such transaction in this space in India. Other major deals in this space have included GMR Group’s $182 million and a Pharmeasy Group entity raising $193 million, according to data from EY.

And it’s not just Indian asset managers that are stepping up. Henry McVey, Chief Investment Officer of KKR’s Balance Sheet and Head of Global Macro and Asset Allocation, says he sees significant opportunities to both deploy and monetise capital across private equity, infrastructure, climate and credit franchises, aided by favourable macro tailwinds in India.

“Control deal activity is more robust, local capital markets are deeper, the policy backdrop is more cooperative and local business leaders are more engaged. In private credit, the opportunity set feels much more disciplined than what we saw during the non-bank financial company heyday just prior to Covid,” says McVey.

KKR has been investing in private credit opportunities in India through its Asia-Pacific funds. For instance, it has extended $600 million credit financing to Manipal Education and Medical Group for expansion.

In January, the US-based global investment giant completed a $2.5 billion private credit fund raise. This included $1.8 billion in KKR Asia Credit Opportunities Fund II and $700 million raised from separately managed accounts focused on same types of investment opportunities. At close, this fund will be the largest pan-regional private performing private credit fund in the Asia Pacific.

Higher Yields

Depending on the due diligence, such funds may lend to companies whose credit rating is below investment grade, the kind of firms that traditional lenders usually avoid. Since such loans involve higher risk, the interest rate is higher.

Yields in private credit funds can range between 12-13% and 17-18%, depending on the fund manager, the underlying risk and strategy. That’s perhaps one reason why some investors are increasingly looking at this asset class amid the current equity market volatility.

“If you make early double-digit returns in a fixed income asset class, which is well collateralised, well secured, well covenanted, especially at this point of time, you get a very resilient portfolio,” says Kapoor of Motilal Oswal Alternates.

Of course, it goes without saying that when higher risk is involved, returns may not be guaranteed. “Like in any other product, past performance is not an indicator of future returns. Experience and knowledge of providing credit to corporates in different economic cycles is critical,” says Sriniwasan.

Global Headwinds

The frenetic activity in the domestic private credit market, though, comes against a backdrop of global turbulence. In recent weeks, the $2-trillion private credit market in the US has been in the spotlight as some asset managers restricted investor withdrawals after a surge in redemption requests. Some reduced exposure to the private credit industry by marking down the value of some loans in their portfolios.

The situation escalated after geopolitical shocks hit global trade. Partly spurred by the uncertainty, investors in the US started placing redemption requests. Analysts, however, don’t see this as a systemic risk.

Back home, fund managers feel the developments in the US stem mainly from the way semi-liquid funds are structured.

“These vehicles offer periodic liquidity even though they invest in illiquid assets, which can lead to asset-liability mismatches during periods of high redemptions. In such situations, managers may have to restrict withdrawals to protect investors,” says Kotak’s Sriniwasan.

The India market is structurally different. Importantly, most private credit funds here are close-ended. Also, these funds don’t use structural leverage, apart from short-term operational lines. Under regulatory guidelines, Category II AIFs in India are not allowed to take long-term loans. Except for meeting routine operational expenses, they generally don’t borrow. In the West, private credit funds may use bank borrowings to increase their investment size and in turn boost investor returns.

More importantly, says Sriniwasan, credit demand in India is driven by strong economic growth, and the need for long-term capital continues to exceed supply.

“This creates a naturally resilient environment, making a US-style redemption stress unlikely to occur here.”

@thenachiket