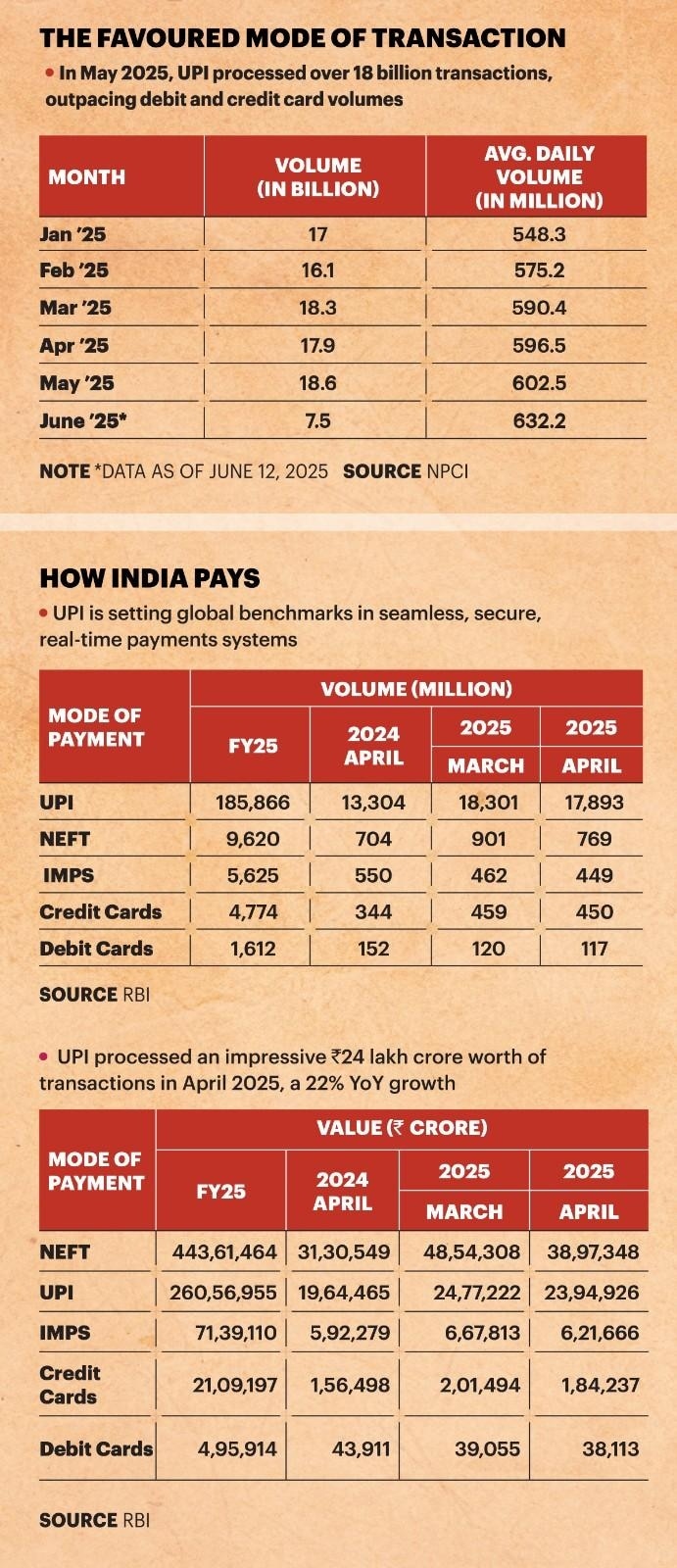

From paying the local vegetable vendor to paying for a luxury bag, UPI (Unified Payments Interface) has drastically simplified digital transactions for billions. Since its launch in 2016, it has emerged as a transformative force in India’s financial system, offering real-time, bank-to-bank transfers through mobile apps. In April 2025 alone, UPI processed over 18 billion transactions, outpacing debit and credit card volumes, which stood at 450 million and 117 million respectively. This meteoric rise highlights UPI’s unparalleled user adoption in India and operational scalability.

Its domestic dominance stems from features like zero-cost transactions, interoperability across banks and platforms, and an intuitive mobile experience. UPI’s ability to enable peer-to-peer transfers, utility bill payments, and merchant transactions with a single click has made it the go-to platform across urban and rural India alike.

According to the Reserve Bank of India, among all digital retail payment modes, UPI has maintained a steady year-on-year expansion of 34.5% in April 2025, proving that it’s not just popular—it’s essential to India’s digital economy. The Great Indian Wallet Study (2025) by consumer finance company Home Credit reveals the widespread adaptation of UPI for person-to-person transactions, especially among the lower middle-class, with 77% now leveraging UPI as a seamless mode of payment—a significant 5 percentage point increase from last year. This highlights UPI’s role in bridging the financial divide.

With the home market conquered, India is now taking UPI to the world. Seven countries—Singapore, the UAE, Bhutan, Nepal, Sri Lanka, France, and Mauritius—currently accept UPI payments at select merchant locations. Notably, tourists can now pay via UPI at iconic locations like the Eiffel Tower in France.

According to the ACI Worldwide Report 2024, India accounted for about 49% of global real-time digital payment transactions in 2023, highlighting its leadership in digital payment innovation. Moreover, as part of India’s global outreach, Prime Minister Narendra Modi has strongly backed the expansion of UPI within the BRICS bloc, which now includes six new member countries. This move is aimed at boosting remittance flows, increasing financial inclusion, and strengthening India’s position in the global financial system.

Ajay Rajan, Country Head—Government, Multinational and International Business, Transaction Banking at YES Bank, says, “UPI has revolutionised digital payments in India, and its expansion into cross-border transactions presents a transformative opportunity to reshape global remittances and merchant payments.”

Rajan adds that since 2022, UPI Global has made measurable diplomatic and commercial inroads. “These aren’t just pilot projects—they’re state-backed collaborations endorsed at the level of central banks.”

UPI For The World

As UPI expands internationally, it has diversified its offerings to address different user segments. For example, UPI Global allows Indian users to make seamless payments at select overseas merchant outlets using QR codes.

These payments are processed in rupees, with the app handling the currency conversion.

However, its reach is limited currently, says Rohit Chhibbar, Chief Business Officer, Credit Cards at Paisabazaar. “UPI is currently accepted in a few countries. However, even in these regions, usage is limited to select merchants who have partnered with UPI-enabled apps or networks.”

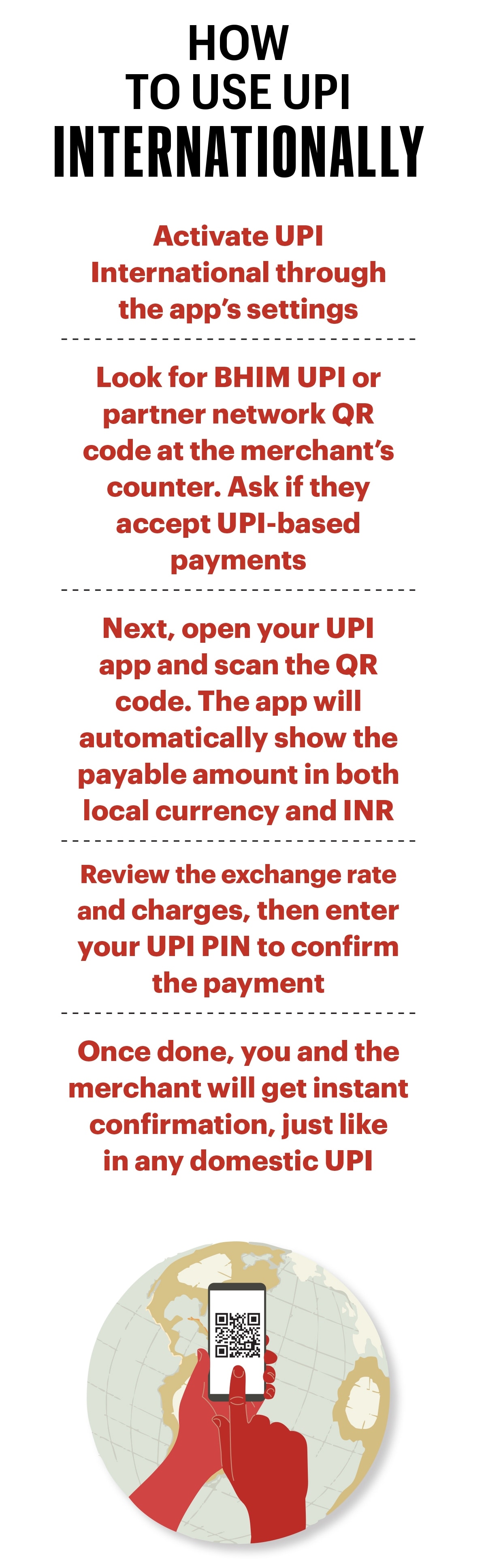

To use UPI internationally, you must first activate ‘UPI International’ for your bank account under the Payment Settings of your preferred UPI app. Note that payments will be deducted in Indian rupee (INR), and foreign exchange conversion rates will apply.

Additionally, your bank may charge an international transaction fee, which may vary based on the transaction amount and destination currency.

Similarly, UPI for NRIs now supports NRE/NRO accounts and international mobile numbers. This has unlocked access for millions of NRIs to use UPI for peer-to-peer payments and merchant transactions, just like residents in India.

UPI One World is designed for inbound international travellers. It enables them to load INR into a digital wallet linked to UPI and spend it easily while visiting India. This eliminates the need for forex cards and reduces the dependence on cash.

Rajan describes UPI One World as more than a product—it is a strategic innovation.

Cross-Border Remittances

India is the one of the world’s top recipients of remittances, with over $121 billion received in 2024. Yet, the cost of sending money through traditional channels remains high.

According to the World Bank, the global average cost of sending $200 is 6.2%, whereas UPI-enabled corridors can slash this cost down. Merchant transactions made abroad using UPI incur no upfront fee, and only foreign exchange conversion charges are applied by the bank. “UPI Global reduces the cost of international transfers by up to 70–90% compared to traditional systems,” Rajan of YES Bank notes. This makes it a powerful alternative for low-value, high-frequency payments, like remittances and tourist spending.

Can UPI emerge as a seamless cross-border payment solution, reducing costs and friction in international transactions? Yes, it can, but not without challenges. Ranadurjay Talukdar, Partner and Payments Sector Leader at EY India, explains, “The cross-border opportunity for UPI is huge, given India’s massive inward and outward forex remittance volumes. But it will always require individual tie-ups with countries.” Talukdar adds that each tie-up will require a separate settlement bank to be appointed, and UPI will need to connect to the real-time payment networks of individual countries.

He adds that while several MoUs have been signed, only the India-Singapore UPI-PayNow link is fully operational. Integration with platforms like FedNow (US) or the Gulf Payment Company (Middle East) could unlock new corridors—these networks are still developing, adding a future-proof solution could be India’s participation in Project Nexus, a BIS-led initiative aiming to create an interoperable hub between domestic real-time payment systems.

Regulatory alignment is another bottleneck. “There are also concerns around how KYC and anti-money laundering guidelines will be adhered to in case of RTP integrations,” Talukdar warns.

UPI’s domestic success was never just about convenience—it was about reimagining finance for a billion people. Its global push is no different.

Through innovations like UPI Global, UPI for NRIs, and UPI One World, India is not just solving payment problems—it’s reshaping how countries think about inclusive digital infrastructure.

“UPI can emerge as the interoperable digital plumbing enabling bilateral and multilateral corridors—sans the legacy cost structures,” Rajan says, much like how SWIFT, or Society for Worldwide Interbank Financial Telecommunication, once standardised international banking messaging.

With sustained policy focus, technology innovation, and collaborative diplomacy, UPI is no longer just India’s pride—it’s fast becoming the world’s blueprint for real-time, low-cost, and people-first payments.

Can the cross-border opportunity be harnessed?

@teena_kaushal