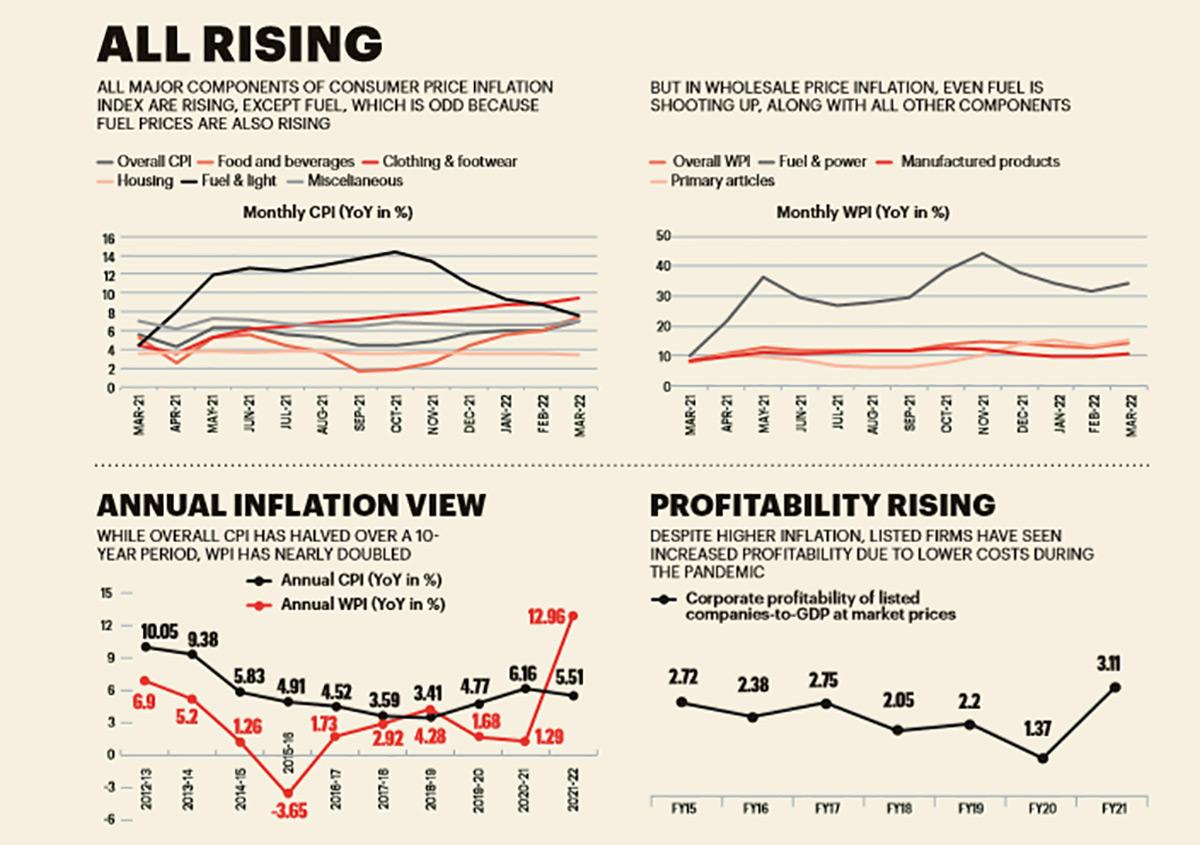

The three witches in William Shakespeare’s Macbeth—representing evil, chaos and darkness—seem the perfect metaphor for the current economic situation. The three witches that can derail India’s and the world’s economic recovery are hardening commodity prices, soaring inflation and unrelenting geopolitical tension, especially emanating from the Ukraine conflict. Countries across the world are bearing the brunt. In March 2022, retail inflation in India was at a 17-month high of 6.95 per cent, while in the US it was at a 40-year high of 8.5 per cent. In India, the wholesale price index (WPI) was also at a 30-year high of 12.96 per cent in FY22, and 14.55 per cent in March.

But it’s not worrying everyone. Former finance secretary Subhash Chandra Garg points out that high inflation has been around under every regime: “India has had episodes of inflation for a very long time. In fact, episodes of not having inflation are smaller. So, if you go to the recent past, from 2008 to 2013-14, we had massive [retail] inflation ranging from 8.35 per cent to 11.06 per cent.” Inflation, which has made governments and policymakers jittery, impacts not only households, but everyone involved in the economy.

The assumption that inflation is evil doesn’t fly when it comes to government finances. From fiscal deficit to tax collection to public debt-to-GDP ratio, inflation has a positive impact on government finances. But it’s not like the government can let inflation rise exponentially, as it runs the risk of an electoral backlash. “Due to inflation, all VATs—GST, excise—will go up,” says Pronab Sen, former chief statistician of India, adding that the rise in GST collections won’t be proportionate to inflation because food inflation wouldn’t impact GST collection. Adds Garg: “Inflation implies the prices of goods will go up, which then yields more indirect taxes; and there is more profitability, which yields higher income taxes. It’s not only the earnings that are impacted by higher inflation. Another vital component of government finances—expenditure—takes a beating because of inflation. The government incurs expenditure in two ways, revenue and capital, and inflation impacts both.”

The government allocated Rs 31.95 lakh crore as revenue expenditure in the Union Budget 2022-23, which is expected to rise as a result of rising inflation. And capital expenditure, which has been substantially increased to Rs 7.5 lakh crore in the Budget, will also get impacted and may overshoot the Budget estimate. “The government incurs expenditures on infrastructure creation in the form of capital expenditure,” says Garg. “If inflation goes up, then the cost of steel, cement and other inputs goes up, and therefore capital expenditure also goes up.”

Madan Sabnavis, Chief Economist at Bank of Baroda, believes that inflation will have two kinds of impact on the budgeted numbers this year. One, with high inflation, nominal GDP growth would also tend to be higher, which would support the Budget in terms of the statistical ratios. And two, there will be a downward bias on the fiscal deficit and the revenue deficit, as they are calculated as a percentage of GDP. “The major pain point for the government is subsidy. The government is quite aggressive when it comes to subsidies on fertilisers. Now, because of inflation, the government will have to spend more on fertiliser subsidy allocations, because natural gas prices have gone up internationally, and imports are also going to become more expensive,” says Sabnavis. Aditi Nayar, Chief Economist at ICRA, also expects the fertiliser subsidy to be substantially enhanced over the budgeted level. The government allocated Rs 1,05,222.32 crore for fertiliser subsidy in this year’s Budget.

But, what about the debt-to-GDP ratio? Sen says, with rising inflation, nominal GDP goes up, whereas debt-to-GDP ratio remains lower. N.R. Bhanumurthy, Vice Chancellor of B.R. Ambedkar School of Economics University, says that public debt-to-GDP ratio depends on the quality of expenditure. “What the government has done since the past two years is that they’re reducing the revenue deficit component and increasing the capital expenditure component. So, by that mechanism, the public debt-to-GDP ratio should come down by 2025-26.”

Rising inflation will also lead to an increase in the cost of borrowing for the government. Bhanumurthy expects government expenditure to shoot up against the budgeted numbers. Even though the RBI has not increased the interest rate to tame inflation, he believes that the government securities market has already factored in the increase in inflation irrespective of any RBI action. India’s benchmark 10-year government securities rose to a three-year high of 7 per cent as on April 12, 2022. “This increase in the government bond yield means the cost of government borrowing will increase, which will lead to an increase in interest payments as happened in the current year’s Budget. Under the expenditure component this year, the interest payment component had risen by Rs 3 lakh crore because of soaring inflation,” says Bhanumurthy.

A sharp spike in WPI, which is dominated by raw materials and intermediate goods, to a 30-year peak of 12.96 per cent in FY22 unravels India Inc.’s struggle with soaring input prices. This March, semi-finished steel, textiles, basic metals, chemicals, rubber and vegetable oils witnessed wholesale inflation of 12-26 per cent. Plus, any potential hike in interest rates by the RBI will lead to an increase in borrowing costs, eating into companies’ profitability. Amid a sagging economy and slackening demand, manufacturers finds it difficult to pass on the spike in input cost to customers, which can erode their profitability.

Of course, some pass-through of price rise has indeed taken place, resulting in the surge in retail inflation in March. Even a recent CRISIL report said that corporate profitability, or the average Ebitda margin, may have dropped by 200-300 basis points (bps) YoY and 40-60 bps sequentially in the fourth quarter of FY22. According to the report, this trend may exacerbate in the coming quarters unless inflationary pressures abate. However, India Inc. witnessed historic corporate profits in FY21, so much so that the corporate profit share in India’s GDP hit a 10-year high of 3.11 per cent in FY21.

Sabnavis says that in Q3FY22, some corporates had started passing on higher input costs to consumers. “Now, the question is, will they have a second round of increase, which will show in very good results in terms of corporate profitability for the fourth quarter,” he adds. But Garg sees inflation and commodity prices impacting different companies differently due to the interplay of input prices they face and their output prices. Amidst all this, he expects some corporates to stay put and some may even get their margins squeezed.

The biggest impact of inflation is on the middle-income- and lower-middle-income households. Between March 2021 and March 2022, food & beverage inflation rose from 5.24 per cent to 7.47 per cent, whereas oil and fat prices spiked 18.79 per cent in the same period. This is the highest price rise among the food basket items used to measure the consumer food price inflation.

“The middle class has a fixed budget and spends more on food items, therefore they may have to cut back on savings or discretionary expenditure. In the lower-income groups, consumption will get tightened even further because they typically spend more money on food items. And that could create problems in terms of overall growth and consumption,” says Sabnavis.

The bigger danger is that higher prices tend to erode the value of real wages and savings. CRISIL said in a note: “We estimate the rural bottom 20 per cent and middle 60 per cent of the income segments faced the highest inflation at 7.7 per cent. In urban areas, the bottom 20 per cent also faced higher inflation than other income segments. However, the burden was slightly less than their rural counterparts given the sharper rise of inflation in rural areas.” In particular, as Bhanumurthy says, two-thirds of India’s population is part of the unorganised sector where salaries are not indexed to inflation. “So, that will eat away their household budgets and erode their real wages.”

@RajatMishra9518