Over the past month, Pankaj Gadgil has been very busy. Work has seen him spend a lot of time moving between cities. As Head of Self Employed Segment, SME and Merchant Ecosystem at ICICI Bank, he is constantly in touch with customers and looking for ways in which he can be more relevant to them. This is in addition to the constant pressure of increasing the customer base.

Perhaps for the first time in his career, he sees a big cultural shift in SMEs (small and medium enterprises). “A lot of things are being shown with greater levels of transparency in the books. One is seeing the clear emergence of the next generation and that is a good sign,” he says. And in at least eight of every 10 entrepreneurs running family-owned businesses that he has met, the younger lot is very comfortable with the digital world. “Technology comes easily to them; and many of them—in their late 20s or early 30s—have studied overseas before taking charge of their business.”

In many ways, this is the foundation of the SME 2.0 story in India, where digitisation and technology are the critical components. “The difference with the earlier generation is that they dealt with public sector banks, while their children speak of private banks or the fintech world,” says Gadgil. The changes taking place are rapid and in real time. He calls this a “cultural shift”, which seems rather appropriate.

D is for digital

Prashant Patel, President of the Federation of Indian Micro and Small & Medium Enterprises (FISME), says SMEs have “no option but to go digital”. He recalls a time when there was a perpetual shortage of skilled manpower and proprietors ran the businesses. “One never had the required knowledge and with that came non-compliance on taxation issues,” he says. Today’s digital age is quite a contrast, though the initial phase of acclimatisation is not easy. “Owners are hesitant since they find it hard to understand technology, but that is changing. If there is something the government can do for us, it relates to simplifying tax procedures.”

The long-term positive impact of going digital is not easy to quantify but those in the midst of it identify a few key points. Shalini Puchalapalli, Director of Google Customer Solutions, Google India, says research has shown that small merchants adopting digital technology grow twice as quickly and employ five times as many people as their peers who don’t go the digital way. “As internet adoption continues to expand, there is still much-needed headroom for deepening digitisation among small and medium businesses, especially those that address customers, who are newly connected, in non-urban locations and with a language preference,” she says. At the same time, there are businesses that have straightaway become digital payments-first. “Innovating for these merchants will be a priority going forward with many adopting app-based business models,” she adds.

Apart from Google Pay, which covers more than 10 million merchants, the company saw an opportunity in what she calls discovery. “Towards this, we launched free profiles for businesses on Google Search and Maps. Five years ago, over 68 per cent of small and medium businesses had no digital presence. Today, that number is less than 20 per cent.”

This is still the growth phase and the transition cannot be measured only in numbers, say experts. According to Akash Gehani, COO and Co-founder, Instamojo—a multi-channel payments gateway solution provider for MSMEs (micro, small and medium enterprises)—a significant part of its business comes from the smallest segment. “We deal with really small businesses, which have a turnover of less than `40 lakh per annum. In the past, a presence on social media through an Instagram profile was the way to do it. Then, the transition to helping them go online started to take place,” he says.

Gadgil picks out a few key indicators apart from the cultural shift in family businesses. “We are seeing the formalisation of the economy and the adoption of technology. This is not just in banking but investments are being made in sales, marketing and accounting as well,” he says. ICICI Bank has just rolled out a comprehensive open-for-all digital app for SMEs. The user just needs to download the InstaBiz app to get started. The insight came after it was learnt that SMEs are keen to adopt digital solutions that simplify the way they do business—the focus had to be on growth, but they wanted a platform to meet all their requirements.

Playing out well

The need for digitisation varies depending on the industry and also the extent to which the SME owner demonstrates an openness to adopting it. There is an investment that comes with it but it is left to the owner to strike the right cost-benefit equation. So, where does technology come into play? Y.S. Chakravarti, MD & CEO of SME financing major Shriram City Union Finance—which has assets under management of Rs 14,500 crore—says there has been a marked change in the way business is done by SMEs. “Be it having an online presence, adopting cloud solutions, getting on to social media, data tracking with data and analytics tools, or manual operations being automated—the objective is to improve efficiency, productivity and keep up with competitors,” he says. There are such examples across the spectrum—from traditional kirana stores using a spreadsheet program to maintain inventory and manage receivables to an engineering unit digitising its product brochures.

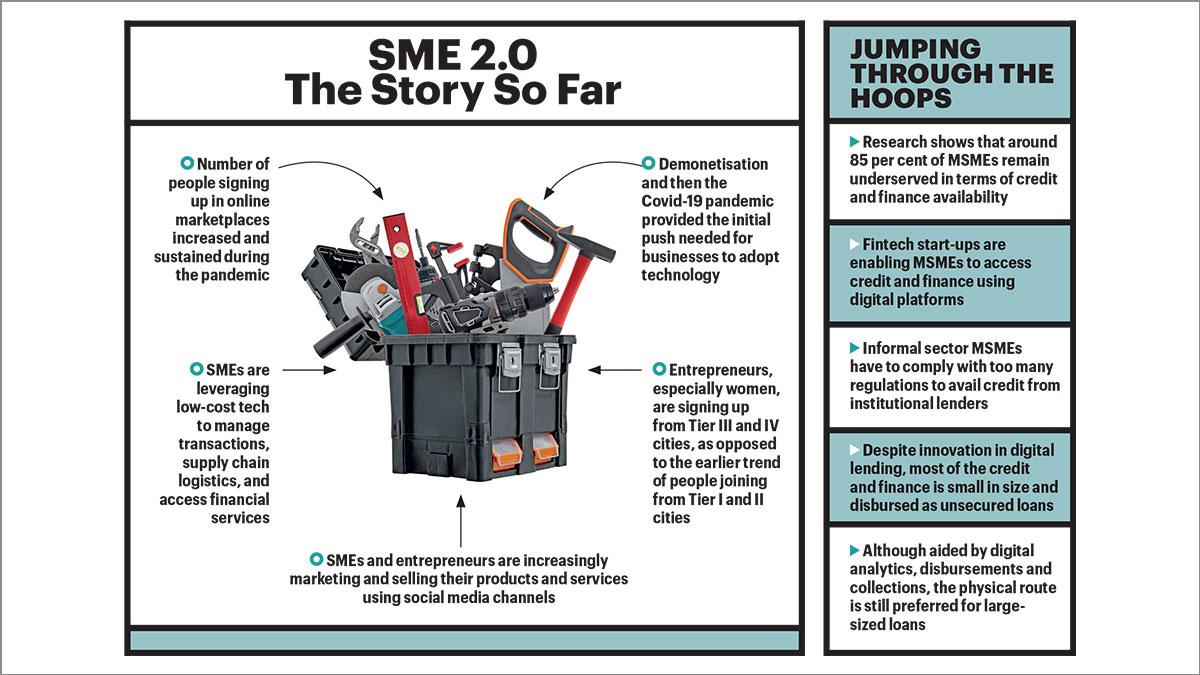

Industry experts say what has transpired over the past five to six years has been unprecedented. Instamojo’s Gehani says e-commerce taking off in a big way was the first big event. “We then saw demonetisation followed by the pandemic. All that expedited the belief that an online presence was a must.” There were a few takeaways through the process, he adds. While the number of people who signed up on Instamojo shot up from less than 1,000 to over 1,500 per day, that growth has sustained, indicating that the change is clearly underway. That’s not all. The composition of those who came aboard was now vastly different—around two-thirds were from Tier III and IV towns, while in the past, that proportion was from Tier I and II towns. Finally, the direct-to-consumer (D2C) story had women entrepreneurs, which took off sharply—from around 30 per cent in the past to 60 per cent now.

The pandemic push

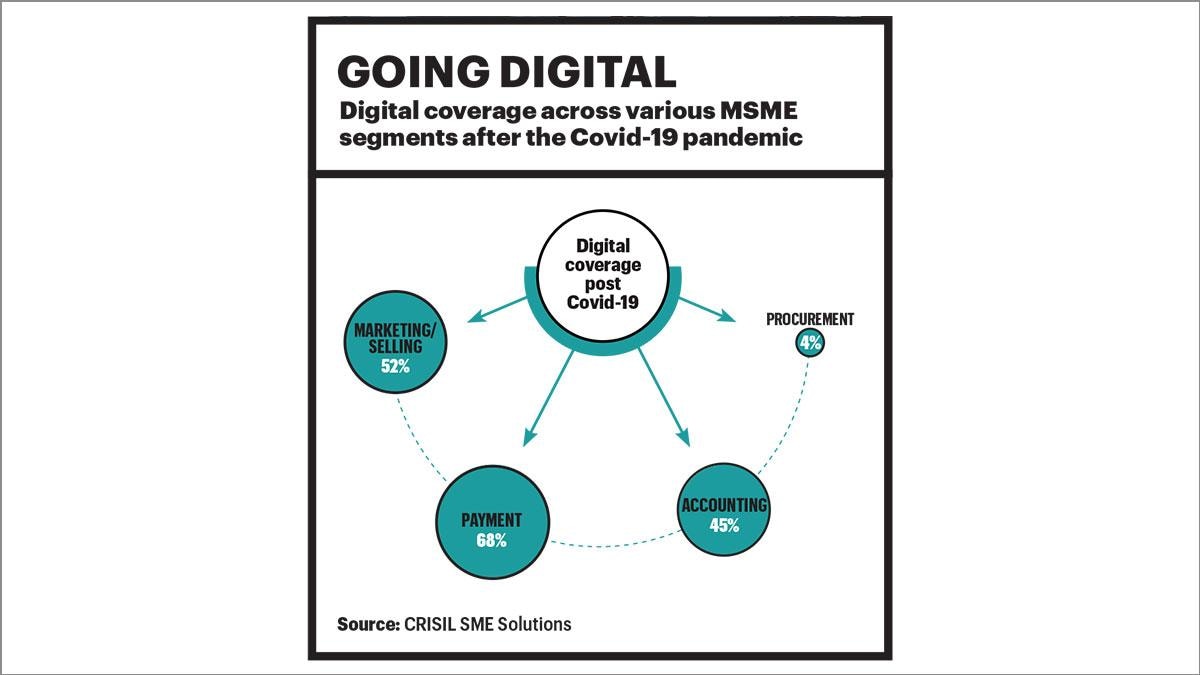

In many ways, while demonetisation set the pace, the pandemic hastened the process of digitisation. A CRISIL report says over 65 per cent of the respondents in a survey of 540 MSMEs upgraded their “digital landscape”. The report, based on the survey, goes on to explain how going digital benefitted the respondents in the “immediate-to-short run by helping them manage transactions at a distance, deliver goods efficiently and facilitate access to financial services, apart from bringing in tangible benefits such as enhanced customer acquisition, operational efficiency, workforce enhancement, risk management, innovation and reduction in manpower requirement”. Of the enterprises covered, 59 per cent had revenues of less than `5 crore; the rest had Rs 5-25 crore. The report also points out that today, about 52 per cent of the respondents use social media to market their products. “A well-integrated and connected digital ecosystem is optimal to build connections and drive transformation of these enterprises. Increasing digitisation also augurs well from a financial inclusion perspective,” the report notes.

This could well be the next round of the SME 2.0 story. Shriram’s Chakravarti cites an IFC report which says that 85 per cent of MSMEs remain underserved in terms of credit, and only one-fifth of these gaps were fulfilled by formal credit. “As a consequence, the MSME lending sector in India faced a credit deficit of `16 lakh crore. Thus, there is enough demand for finance from small businesses and we see adequate opportunities for lenders. The challenge is in the form of rising interest rates and inflation, which might disturb their profit margins.” On the digital lending part, he acknowledges the role of fintech. “This has largely been restricted to relatively smaller ticket sizes and unsecured loans. Though we have incorporated digitisation into core MSME processes such as analytics, disbursements and collections, we continue to follow the physical route for matters related to collateral, since a bulk of our lending is secured against collateral,” he explains, adding that the objective is to digitise this over time.

Now, from a fintech point of view, the opportunity is simple. According to Harshvardhan Lunia, Founder & CEO of Lendingkart, a fintech lender, it has been working on digitising the lending process to enhance customer experience and make transactions easier during the loan journey. “We have gained experience in lending through providing credit access to more than 130,000 customers across the country with disbursements of around Rs 10,000 crore and in the process have evaluated over 110,000 loan applications.”

Of course, getting all this right will also mean getting the other pieces together. FISME’s Patel thinks the younger generation is not keen on a career in SMEs and prefer corporate jobs. “If we pay Rs 40,000 a month for a particular job, large companies will give them twice as much.” He also speaks of sourcing funds as being a hurdle, since lenders always ask for collateral. “Also, SMEs have to comply with too many regulations since not all of them are from the organised sector,” says Patel.

In the midst of all this, the process of transformation is fascinating; SMEs, too, are acutely aware that this could lead to a huge upside for them. With disruption being the name of the game, SMEs recognise the need to look at their own business differently and objectively. Google’s Puchalapalli speaks of the D2C model before emphasising how “businesses have an opportunity to build greater customer affinity than even their larger peers and own the end-to-end experience”. It is just one of the many opportunities staring at the SMEs in their face. Going digital is a natural progression for the SME 2.0 story. That said, the window it opens up to the world that lies outside is too big to miss. It is left to SMEs to make the most of it.

@krishnagopalan