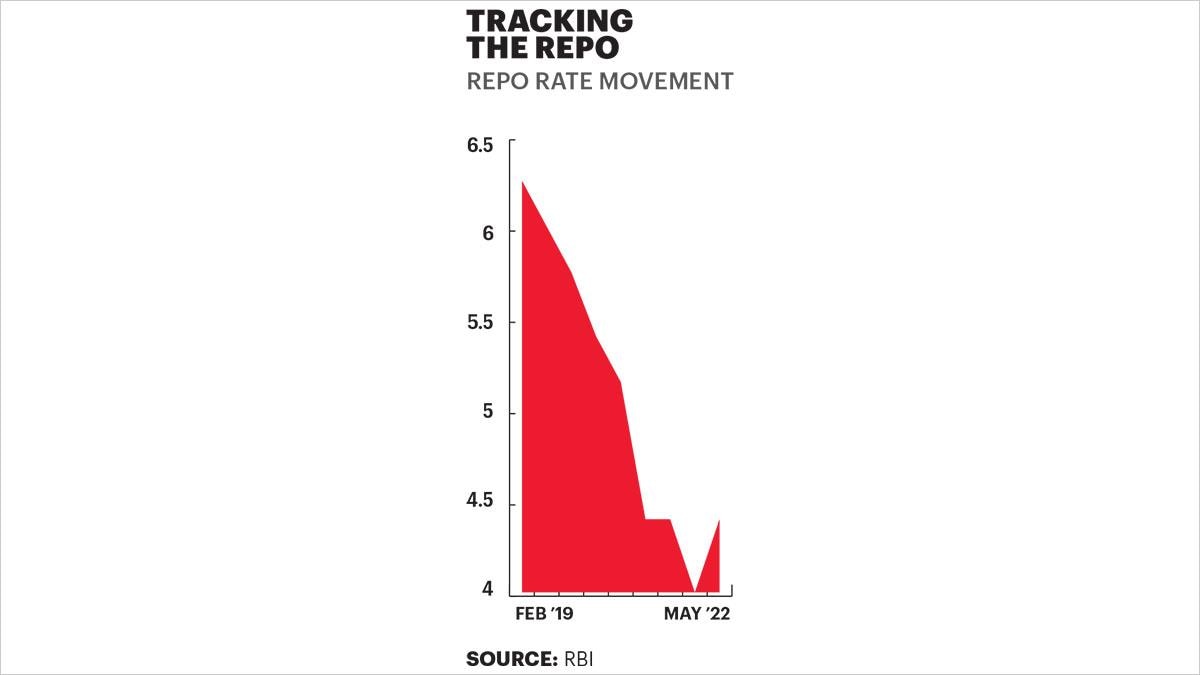

The era of low interest rates is finally over. The Bank of England has raised short-term interest rates for the fourth time in the past five months. The US Federal Reserve has raised rates twice. And back home, the Reserve Bank of India (RBI) recently raised its repo rate—the rate at which it lends to commercial banks—for the first time in two years. That’s not the end of it, though. Expect more hikes from the RBI and other central banks in the days to come. The reason: surging inflation.

Since interest rates are inversely correlated with economic growth, there is a danger that the nascent economic recovery post the pandemic may falter. “The bigger picture is that the monetary experiment [low interest rates and surplus liquidity] which the developed world was running for the last 20 years is winding down and no one knows of the consequences it will entail,” says Abhijeet Awasthi, a currency expert. Many experts fear a recession in the US. India, meanwhile, is facing a double whammy: elevated global interest rates as well as rising domestic interest rates. Aggressive monetary tightening by the US and other central banks will create a spillover risk for emerging economies like India. “There will be a slowdown in growth, but nothing as scary as what experts are suggesting; for example, the likely recession,” says Madan Sabnavis, Chief Economist of Bank of Baroda.

A month ago, the RBI changed track by prioritising inflation over growth. It cut its GDP growth forecast from 7.8 per cent to 7.2 per cent for FY23 and upped its inflation projection from 4.5 per cent to 5.7 per cent. But it refrained from raising the repo rate. What changed between then and now is the US Fed’s decision to raise rates and higher-than-expected domestic retail inflation, which was close to 7 per cent in March.

In a rising interest rate scenario, the government’s cost of borrowing is expected to go up. That’s not all. “Revenues or tax collections would get hit as corporate margins are likely to shrink with higher inflation and interest costs,” says an economist. The rate hike will also have a negative impact on the corporate capex cycle. And global rate hikes are expected to quicken dollar outflows from emerging markets like India. What happens next?

“The repo rate is likely to increase to at least 5-5.25 per cent from 4.4 per cent depending on the inflation trajectory. But we need to look at the aggregate demand in the system, the channel of transmission and the effect of a global spillover for future inflation trajectory,” says Saugata Bhattacharya, Chief Economist of Axis Bank.

@anandadhikari