Every so often, I hear 30-somethings, maybe a decade into their career, longingly talk about retiring by the time they are 45 or 50 years old. I always ask them what they are doing to make that happen? Pat comes the reply: “I’m going to start planning soon” — by which they mean after they turn 40! Possibly the most underestimated power when it comes to financial planning, particularly retirement planning, is time. Today I find that most salaried individuals are aware that they will have to save for their own comfortable retirement. But what they do not know is how much they will need and why time is their biggest advantage.

Every so often, I hear 30-somethings, maybe a decade into their career, longingly talk about retiring by the time they are 45 or 50 years old. I always ask them what they are doing to make that happen? Pat comes the reply: “I’m going to start planning soon” — by which they mean after they turn 40! Possibly the most underestimated power when it comes to financial planning, particularly retirement planning, is time. Today I find that most salaried individuals are aware that they will have to save for their own comfortable retirement. But what they do not know is how much they will need and why time is their biggest advantage.

The first question requires one to take some decisions about how they want to lead their retired life and then derive a value for their retirement kitty, after factoring in inflation. It’s a simple exercise that a financial planner or retirement planning calculators, available on websites, can help one with. Put simply, there are three reasons why one should begin saving towards retirement in their 20s or early-30s. They are all simple, well-established rules for financial success but ones that are often sacrificed in the pursuit of more immediate pleasures, be it the EMI on the expensive watch or dinner at the new restaurant in town.

Make the power of compounding work for you: The power of compounding certainly makes the old adage come alive — time, indeed is money. Today, any money you put aside compounds every year, so you earn returns not only on your principal but on your returns as well. Let’s suppose Ramesh and Vikram want to retire at the age of 60. Towards this, Ramesh invests Rs 1 lakh each year for his retirement corpus from the age of 25 up to 59 years — a total of Rs 35 lakh. On the other hand, Vikram, to compensate for lost time, saves Rs 2 lakh every year from the age of 35 up to 59 — a total of Rs 50 lakh. Both earn the same returns; yet, despite investing less, Ramesh accumulates Rs 2.98 crore, compared to Vikram’s kitty of Rs 2.16 crore.

Make the power of compounding work for you: The power of compounding certainly makes the old adage come alive — time, indeed is money. Today, any money you put aside compounds every year, so you earn returns not only on your principal but on your returns as well. Let’s suppose Ramesh and Vikram want to retire at the age of 60. Towards this, Ramesh invests Rs 1 lakh each year for his retirement corpus from the age of 25 up to 59 years — a total of Rs 35 lakh. On the other hand, Vikram, to compensate for lost time, saves Rs 2 lakh every year from the age of 35 up to 59 — a total of Rs 50 lakh. Both earn the same returns; yet, despite investing less, Ramesh accumulates Rs 2.98 crore, compared to Vikram’s kitty of Rs 2.16 crore.

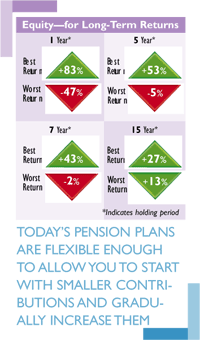

Slow and steady wins the race: Because of the power of compounding, the earlier one starts to save, the lower the amount to be contributed to earn a specific retirement kitty. Today’s pension plans are flexible enough to allow you to start with smaller contributions when you begin your career and gradually increase them as you grow.

Take a calculated risk: The buoyancy of the equity markets hold a mix of promise and peril, depending on your risk profile and outlook. True, in the short term a hot stock gone cold can turn your dream retirement into a nightmare. But it’s well recorded that investing in a diversified portfolio over 10-15 years, gives high returns and hence a healthy retirement kitty. One caveat: unless you understand the markets well, avoid a direct investment. Instead invest fixed amounts systematically over the years through a trusted pension plan.

(The author is a Executive Director, ICICI Prudential)