It’s deja vu again. At the close of yet another year you find that your money hasn’t grown as much as you had hoped. You take a deep sigh and hope to do better next year—and do nothing to ensure you really do better in the New Year. This is where we come in. To tell you ways that will make your wealth grow faster.

|

| Click here to see what your financial resolutions should be |

Indian middle class has seen an unprecedented prosperity surge in recent years. Along with pay cheques, aspirations have also spiralled. Today your monthly purchase list does not stop at the grocery and occasional suit/sari. It also has the latest iPod, better car accessories, a designer party outfit...The “more” syndrome has caught on: more money, more assets, more investments, more expenditure, more wants. To make sure you have more money for years financial planning becomes both critical and complex.

Help is just a page away. Turn over to find how by making — and adhering to — 10 simple financial resolutions you can move towards your goals. Some resolves are those that you had always wanted to follow, others that you probably never thought of. And yet others are those sneaky ones that may have fleetingly crossed your mind, but you banished them out of embarrassment.

MONEY TODAY rings in the New Year re-affirming its promise: Makes you richer.

RESOLUTION 1: I will not keep more than one month’s salary in my savings account.

What would you do if somebody stole the money in your bank account? Raise a ruckus, call the police, file a report? Well, there’s a thief who robs millions of bank accounts every day and nobody even comes to know about the theft. The culprit is inflation and its victims are people who keep large balances in their savings bank accounts. Inflation erodes the value of money. If it is cash, the value erodes faster. But savings bank accounts are only a tad better. With inflation raging at 6%, the 3.5% that your money earns in a savings bank account translates into an annual loss of 2.5% for you. The longer money stays idle in the account, the fatter the loss.

What’s the way out? If you are risk averse, go for a sweep-in account where excess money over a specified amount is put into a fixed deposit and earns a higher rate of interest. If you can stomach some risks, invest in a good mutual fund through a systematic investment plan. A one-time instruction to your bank is all it takes.

If you are too tied up in work to write out a cheque or fill up a mutual fund application form, don’t despair. Netbanking now allows you to buy and sell mutual funds from within the air-conditioned comfort of your office. So, kick the hoarding habit this year. You work hard to earn your money. Now make it work as hard.

RESOLUTION 2: I will not invest in insurance to save tax.

Seven out of 10 people don’t know what kind of insurance policy they have. Five of them don’t even know how much insurance cover they have. All they know is how much premium they pay every year and how much tax they save. That’s because most of them never bought an insurance policy—it was sold to them. And one compelling reason for taking the policy was that it would help save tax. True, the tax breaks on life insurance are very generous— there is a tax rebate on the premium paid, maturity amount is completely tax free and even the sum received by the nominee in case of death is not taxed.

But that should not be the reason for buying an insurance policy. Many people make the common mistake of combining insurance with investment by going in for money-back or endowment plans. The truth is they are neither adequately insured nor do their investments earn good returns. They pay a huge premium but the cover is abysmally low. And the returns are lower than even FDs.

So, from this year onwards, treat insurance as a raincoat for the monsoon. Not an all-purpose garment you wear the year round.

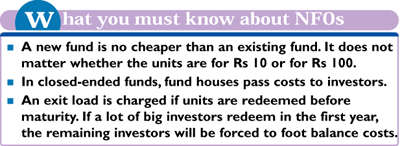

RESOLUTION 3: I will not invest in a new fund unless it offers something different and better.

Whenever a mutual fund comes out with a new fund offer (NFO), agents and distributors go into overdrive. “This new fund is bound to do well.” “It is cheap. The NAV is only Rs 10.” “It’s a great opportunity.” Don’t believe in this hogwash. A new fund is no cheaper than an existing fund. The NAV does not matter. Whether you buy a fund priced at Rs 50 a unit or at Rs 10 a unit, your money will be used to buy shares from the same market at the same price. What matters is what the fund manager is buying. If he picks gems, your fund will do well. If he is so-so, so will be the returns. How do you judge a fund manager? Go by the fund’s performance. A new fund has no track record. So, think twice before investing in an NFO. It could be riskier than an existing fund.

But why are agents and distributors bleating buy, buy, buy? That’s because they get a higher commission for selling NFOs. Fund house offer up to 5% commission on NFOs compared with around 1.5% for existing funds. And guess who foots the bill? Why, you, of course.

RESOLUTION 4: I will buy health insurance for my family.

Good health is perhaps one of your biggest assets. How do you protect this invaluable treasure? Well, eat right, sleep well and exercise a bit. But sickness and accidents can strike anyone. Anywhere. Anytime. With staterun hospitals too overburdened and private healthcare too expensive, medical insurance has become crucial today.

Many people don’t buy medical insurance because they feel it’s an unnecessary expense. It’s not. In fact, it may be one of the most important components of financial planning, second only to life insurance. For it protects your wealth when you are hospitalised, providing you with money for medical treatment. A surgery and a three-day stay in a hospital can cost Rs 40,000-50,000.

Then there are those who don’t buy medical insurance because their employer gives them health cover. What happens when they change jobs? Between the time they leave their previous employer and till they join the new job, they will be without any medical cover. Even if they don’t intend to switch jobs, they will eventually retire one day. It may not be possible to buy health insurance at that age. Or it would cost the earth.

Buy health insurance early in life if you have a history of diabetes, heart ailments and blood pressure in the family. After three years of not making a claim, your health insurance will continue even if symptoms of the disease show up. What’s more, premium of up to Rs 10,000 in a year is deductible from your taxable income. That effectively means a discount on the premium you pay for the health insurance cover.

RESOLUTION 5: I will not roll over my credit card bills

You splurged at the shopping fest, ran up a big bill at the Christmas party, and bought yourself that slick iPod—all thanks to the convenience of plastic. And what do you do when the bill comes? It is tempting to pay the minimum amount, which is 5% of the total bill, and roll over the balance for a month. Your credit card company will love you for it.

That’s because if you roll over your credit card bill, you pay 2-3% a month on the outstanding amount. That works out to 24-36% a year, and is perhaps the most expensive form of lending in the organised sector today. The billing meter doesn’t stop there. If you are rolling over credit, you do not get the normal 30-45 day interest free credit on the subsequent use of the card. Fresh purchases attract a monthly interest of 2-3% from the date of transaction.

So, use plastic for the convenience of not carrying cash and for the interest free credit for up to 45 days. Not as a means of borrowing. And don’t get lured by offers of free credit cards. You don’t have to take them just because they are free. Just two or three cards — at least one of Visa and one of MasterCard — are enough. Anything more will give you a credit limit which you probably won’t utilise.

RESOLUTION 6: I will not get caught in the ‘Rush of March’

In a financial year, one can invest up to Rs 1 lakh in tax saving instruments under Section 80C. You could invest that sum in one or two big chunks in February and March or you could invest it in convenient instalments through the year. It is one of those things you keep reminding yourself of every March. Only this year, do so in January and continue doing it through the year. Not only will it save you the last minute hassles and anxiety, your investments will also grow that bit faster. That’s because each monthly investment earns interest through the year.

In many cases, last month tax saving investments have to be made in tight financial conditions. There is a shortage of funds for the salaried, what with hefty deductions, while the business class is busy putting accounts in order.

The good news is that technology has lightened our concerns. You can now instruct your bank to debit a specified sum from your account every month for investment in a mutual fund. This way even if you forget to make your monthly investment, your bank doesn’t.

RESOLUTION 7: I will pay attention to allocation of my savings.

In the World of finance, everything doesn’t go right or wrong at the same time. So while the romance of money making might lure you into putting all your earnings together, it might so happen that you lose everything together. So vow to leash your greed and be more phlegmatic.

Allocate your assets in the right mix of high-risk high-returns and low-risk low-return investments, spreading the risk across debt and equity and the whole class that comes between these two. This diversification will lower your portfolio’s vulnerability to ups and downs in the market.

At the high end of the risk spectrum are equities, artefacts and real estate that do not guarantee any return. But when they do, the benefits are very high. The next level of products are mutual funds and company fixed deposits. For the risk averse, SIPs are the best way to begin. At the lower end are fixed income options, such as PPF, NSC and bank deposits. Conservative portfolios would allocate a major chunk of such instruments.

Typically, you should begin your career with a heavy equity portfolio and slowly temper it with debt instruments so that by retirement you have a majority of secure investments to dip into.

RESOLUTION 8: I will check all my bills for discrepancies and incorrect charges.

It always pays to read the fine print. And if you’ve been paying for cell phone services that you never asked for or find in your grocery bill items you never consumed, it’s high time you start reading your bills carefully.

Thankfully consumer courts have taken care of some issues like over billing. No more can a multiplex charge Rs 25 for a litre of mineral water or an insurance firm deny a valid health insurance claim.

Yet there is no substitute to individual scrutiny. In many cases, this verification is not a matter of being extra careful. You are supposed to make the checks. For instance, all quarterly bank statements come with a disclaimer that leaves the onus on you to point out any discrepancy in the statement within three weeks. So if there is a charge on a transaction that you did not make, and you do not report it, the bank assumes you agree with the charge being levied.

That’s not all. Keep a hawk-eye to spot those credit card transactions that you did not make, the surcharge that was not reversed though the card came with the offer to waive such charges and the double withdrawal that sometimes shows up on bank statements.

Start by combing through the bill of your New Year bash. Is the tip included in it as service charges or are there delicacies on paper that you don’t remembering tasting?

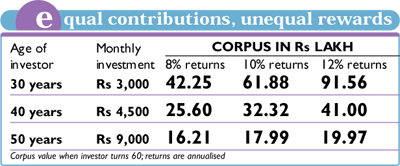

RESOLUTION 9: I will put at least 10% of my income in retirement planning.

The mantra in investment is that it’s never too early. And even though you can’t imagine yourself at 60 now, the truth is that someday you will be. Then, as now, you will be looking to maintain the standard of living for which you have toiled away years. So don’t delay in planning your retirement.

A retiree needs about 60% of his last drawn salary to maintain his pre-retirement lifestyle. Assuming that his last salary would be Rs 2 lakh, he would require Rs 1.2 lakh a month—and a corpus of Rs 2 crore. This rather daunting task is easier if you work in the organised sector. The compulsory savings in Provident Fund through both employee and employer contributions plus the gratuity payment offers some cushion. But you still need to invest more to bridge the gap between needs and means.

So, make it a habit to invest at least 10% of your monthly income in any long-term savings option. We suggest well performing mutual funds. It is the most tax efficient way of creating wealth.

RESOLUTION 10: I will write down my financial goals once a year.

If you have made all the nine preceding resolutions, congratulations. You have a comfortable financial future ahead. But making a resolution is easy. Adhering to it is the difficult part. People soon forget what they had resolved to do and their finances return to the doldrums.

You can break free of this monotonous order of things by writing down your financial goals. These could be anything—buying a house, saving for your child’s education or marriage, even going on a holiday abroad. The point is, if you have written down your goals as also the investment plan for achieving them, you are less likely to lose sight of your target.

As a first step, list out your financial goals, the year you want to achieve them and what they would cost today. So, if you have not yet worked out how much you want to spend on a second flat or sending your son to a foreign university, now is the time to begin. Assuming a conservative 10% return on investment with 6% inflation eating into your wealth, you can accomplish your goal by making small contributions towards it right away. Do this simple exercise and you will find that you are firmly moving towards your financial goals, not taking a random walk.

(With Kamya Jaiswal)