Rule: One should keep enough cash to fund living expenses for three to six months.

Exception: In case of uncertainty in the job market, falling incomes and volatile asset prices, one should have a thicker buffer of 9-12 months’ living expenses to help tide over any financial emergency.

5 lakh: is the number of Indians who have lost their jobs in the past one year due to the slowdown. According to ILO, up to 5.1 crore people could lose jobs worldwide in 2009.

8.2%: was the average pay hike in 2009, according to consultancy firm Hewitt Associates. This is the first time in six years that India has seen single-digit increments.

The past 18 months have been an extraordinary example of how asset prices can come down sharply and lead to severe losses. The period was especially devastating for those who lost their jobs or suffered pay cuts. For many, it was a double whammy as they were forced to liquidate assets at low prices to raise cash for sustenance. This is when a bigger emergency fund can prove useful.

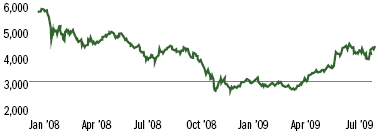

Nifty Movement

After falling to a multi-year low on 27 October 2008, the Nifty closed below 3,000 on 87 of the 100 trading sessions till 27 March 2009. If a person had been forced to sell shares or equity funds during this five-month period, he would have lost out when the markets revived. Similarly, realty prices have slipped. If one sells now, he may end up missing the next bull run in real estate.

It’s better to err on the side of caution and build a big emergency fund. Sure, it might mean an opportunity loss—the cash in your bank will earn a meagre 3.5%, while other options can earn up to four times as much. But it ensures that you are not forced into a distress sale due to the cash crunch.