Talk of taking someone to the cleaners! A judge in the US has filed a $67 million lawsuit against his dry-cleaning service, which lost his favourite pair of pants. Then, of course, there’s the famous case of a woman suing McDonald’s after she spilt hot coffee over herself. Most of us laugh off these stories as urban legends. But don’t laugh too soon; this litigious culture has crept into India, and professionals— particularly doctors, lawyers and accountants—could face the wrath of unhappy clients.

Recently, the All India Institute of Medical Sciences in Delhi was ordered to pay Rs 5 lakh in damages after one of its doctors wrongly diagnosed a woman with cancer and surgically removed the “affected” part. Several other patients have taken hospitals and doctors to court for malpractice or negligence. And the courts have been ordering doctors and hospi -tals to pay up.

So far, only medical practition -ers have been at the receiving end, but it’s only a matter of time before a disgruntled client sues his audi -tor for filing a wrong statement of income. A lawyer or an architect can just as easily be taken to court. And more often than not, the courts will order them to cough up large sums as compensation.

So far, only medical practition -ers have been at the receiving end, but it’s only a matter of time before a disgruntled client sues his audi -tor for filing a wrong statement of income. A lawyer or an architect can just as easily be taken to court. And more often than not, the courts will order them to cough up large sums as compensation.

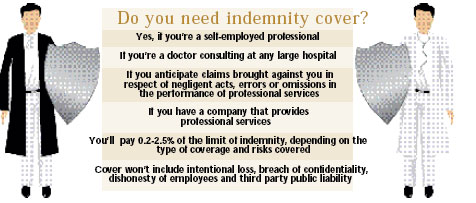

Even if the doctor, lawyer or engineer had acted with the best of intentions, he might still end up paying the price for any mistake. Which is why it makes sense to take professional indemnity insurance. Ask Dr Naresh Dang, consultant physician and cardiologist, Max Balaji Hospital, who has had professional indemnity cover for some years now. “In the profession of medicine, nobody can guarantee 100% successful treatment.

Therefore, it is always better to take this cover, even though one may not use it.”

What it is Broadly speaking, professional indemnity insurance covers the insured against finan -cial loss resulting from a claim brought about due to an error or omission that occurs while performing a service contracted for. The loss must be to a third party who has suffered injury or property damage.

“This is similar to product liability except that this protects the buyer against negligence in servic -es provided. For individual professionals, this policy can ensure personal as well as professional survival should they have to pay a claim,” says Pavanjit Singh Dhingra, vice-president, Prudent Insurance Brokers.

The cover is needed especially as the insured may not be able to bear the loss if a claim is brought against him/his company, as also to comply with contractual obligations and sometimes with statutory mandates. “Most prestigious hospitals today have made it mandatory for their doctors to take at least Rs 20 lakh indemnity cover,” says Dang.

The cover is needed especially as the insured may not be able to bear the loss if a claim is brought against him/his company, as also to comply with contractual obligations and sometimes with statutory mandates. “Most prestigious hospitals today have made it mandatory for their doctors to take at least Rs 20 lakh indemnity cover,” says Dang.

Almost all general insurance companies offer indemnity cover to professionals. Some insurers have separate policies for doctors, CAs, engineers, lawyers and architects against unintentional errors and omissions that may cause damage, loss or hardship to their clients.

What’s covered The scope of cover varies with each profession. For instance, registered medical practitioners, such as physicians, surgeons, cardiologists and pathologists, as well as medical establishments, are protected against legal liability claims made by any of their patients. The policy also pays for the cost incurred in defending the case, and can be extended to other partners or consulting doctors as well as employed assistants.

Unqualified staff like peons and sweepers working in the clinic can also be covered for errors, omissions and negligence on their part. Likewise engineers and architects are protected against liability arising out of design defect, inappropriate design leading to damage and loss of life to third parties.

For accountants and lawyers, the policy covers the legal liability incurred by way of losses to clients arising out of omissions or errors on the part of the insured or his paid employees named in the proposal. For instance, if your lawyer fails to file a paper before a deadline, resulting in the decreased value or complete loss of your case, he would be liable for an errors and omissions claim.

What’s not Indemnity insurance does not cover liabilities aris -ing out of criminal acts or any act committed in violation of any law or ordinance, besides services rendered while under the influence of intoxicants. Fines, penalties, punitive or exemplary damages, or third party public liability or loss arising out of war and nuclear per -ils are also not covered. Each insurer has a list of exclusions, which must be taken into consider -ation before taking any cover.

There is no fixed sum assured or limit of indemnity, which gener -ally depends on the insured’s per -ception of risk. “There are no min -imum or maximum limits. The insured is free to propose any sum insured based on the estimation of risk associated with professional services,” says  , head-underwriting, Bajaj Allianz General Insurance.

, head-underwriting, Bajaj Allianz General Insurance.

The limit is fixed per accident and per policy period, called Any One Accident (AOA) limit and Any One Year (AOY) limit, respectively. The AOA limit, which is the maxi -mum amount payable for each accident, should be fixed taking into account the nature of activity of the insured and the maximum number of people who could be affected and maximum property damage that could occur in a worst-case scenario.

What it CostsThe premium rates are based on the risk profile of the insured. “The premiums can range between 0.2% and 2.5% of the limit of indemnity depending upon the type of coverage and the quality of risk,” says Rahul Aggarwal, CEO, Optima Risk Management Services. For instance, while a surgeon needs to cough up Rs 10,000-20,000 for a Rs 20 lakh cover, a general practitioner needs to pay only Rs 600-6,000. Engineers and architects, who carry a higher risk, are charged Rs 20,000-30,000 for the same cover.

Whatever be the case, the sum insured should be chosen in a manner that it covers any legal obligation that the insured may face. “The adequacy of sum insured and the coverage, including optional extensions, are the most important factors to be borne in mind while taking the cover,” says Ramalingam.

One of the interesting features of the professional indemnity cover is that it works even after you let it lapse. If a claim is filed in respect of an error or omission that occurred when the policy was in force, the insurance company is liable to pay, even if you no longer practice or the policy is no longer valid.