Health is wealth, but poor health need not make you poorer in wealth if you have a smart health insurance plan.

Health Insurance

Life took a nasty turn for Poornima Vyasulu in 2003 when one of her kidneys suddenly stopped functioning. The Bangalore-based management professional was hospitalised for several months and underwent prolonged treatment. Even today, she has to undergo dialysis three times a week at a hospital. Guess how much she has spent on her treatment: not even a single rupee. Her health insurance plan cushioned Vyasulu against the huge medical bill she had run up.

For Vyasulu, renewing the health insurance policy every year has almost become a habit since she first took the plan in 1988 on the insistence of her employer. The small premium she paid for the cover every year eventually saved her an expense of a couple of lakh rupees. “I am a living example of how one can benefit from medical insurance,” she says.

| Between Rs 2.20 and Rs 50 a day is all you need to keep away the worries of meeting medical expenses |

Not many people look at it that way. They insure their cars and their houses. But when it comes to insuring themselves against medical costs, they see it as an unnecessary expense. However, rising medical expenses and increased awareness are now pushing more and more people to take health cover. Says Antony Jacob, CEO, Royal Sundaram Alliance: “There is a significant increase in people seeking health insurance these days and that is good for them.”

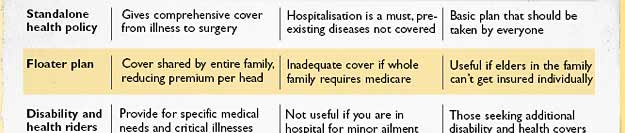

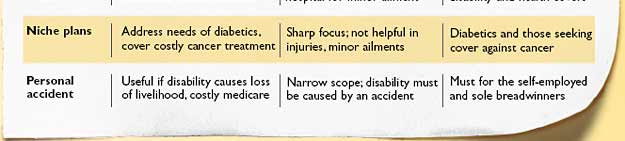

There is a wide variety of health covers available today, ranging from ordinary medical insurance policies to floater plans for the entire family and health riders attached to life insurance policies. There are even policies for specific diseases such as diabetes and cancer.

The traditional health insurance policy for an individual reimburses expenses incurred on medical treatment that required hospitalisation. Expenses incurred on treatment at home are covered in case the patient cannot be taken to a hospital or if there is none nearby.

Then there is a floater plan, where the cover is shared by the entire family. The rationale for a floater plan is simple: the probability of the entire family taking ill together is very low.

You can also insure against medical costs by taking a rider along with a life insurance policy. A surgery rider covers expenses incurred on specified procedures. A critical illness rider provides money for treatment if the policy-holder is diagnosed with any of the diseases specified in the policy. But these riders cannot substitute a basic health policy. If a person is hospitalised for a minor illness— such as mild food poisoning—these riders won’t help.

Shubha Mudgal and her musician husband Aneesh Pradhan coaxed insurers to cover artistes in case an accident or illness prevents them from performing. If she loses her voice and is unable to work for over 15 days at a stretch, Mudgal gets compensated. Likewise, her husband will get compensation if he is unable to play the tabla

"It’s a customised plan, and will be of great value to artistes"

SHUBHA MUDGAL, SINGER |

The government has made health insurance even more attractive by offering income tax benefits. Premium of up to Rs 10,000 a year is fully deductible from your taxable salary under Section 80D. Added to the Rs 1 lakh tax deductible investments allowed under Section 80C of the Income tax Act, this effectively raises the tax deduction in a year to Rs 1.1 lakh. All healthrelated riders also get Section 80D benefits.

If by now you have realised the benefits of health insurance, the next step is to decide how much cover you need. The extent of health cover is usually capped at Rs 5 lakh though some insurers do offer higher covers. But experts say that the treatment of most diseases is possible within the Rs 5-lakh limit. So there is no use in going for an unnecessarily large cover.

There’s another compelling reason for taking a cover early in life. As you age, medical problems become more frequent and medicare costs go up. But it may be too late to buy health cover in old age: with some insurers, pre-existing medical conditions are not covered, and premiums definitely increase with age.

| BREAKING IT DOWN |

In your 20s:

Medical cover of Rs 1 lakh costs Rs 1,150 a year Apprx daily cost: Price of a newspaper |

In your 30s:

Medical cover of Rs 2 lakh costs Rs 2,467 a year Apprx daily cost: 2-minute STD call charge |

In your 40s:

Medical cover of Rs 3 lakh costs Rs 4,648 a year Apprx daily cost: Charges for cable TV |

In your 50s:

Medical cover of Rs 4 lakh costs Rs 7,609 a year Apprx daily cost: Less than price of 2 colas |

In your 60s:

Medical cover of Rs 4 lakh costs Rs 17,365 a year Apprx daily cost: Price of a burger |

In your 70s:

Medical cover of Rs 4 lakh costs Rs 21,714 a year Apprx daily cost: Bill for 2 coffees in a cafe |

There is more to health insurance than merely reimbursement of hospitalisation expenses. What happens, for instance, if a person is temporarily or permanently disabled by an illness or by an injury sustained in an accident? What if the disability—loss of limb, sight or hearing—seriously impairs his capacity to earn? “A life insurance policy only covers the risk of death,” says risk management consultant Swami Saran Sharma. “Health insurance policies cover medical expenses but provide no compensation for the loss of livelihood.” In some cases, that fate can be worse than death.

This gap in an individual’s insurance portfolio can be fixed by taking a personal accident policy. These are policies which compensate the insured person for various problems resulting from an accident. The premium is very low compared with that of a life insurance policy or a health policy. Even so, very few people take personal accident cover. It is not uncommon to find a person with a Rs 50 lakh life cover and a Rs 3 lakh health cover going about life without a personal accident plan.

Broadly, personal accident policies cover you for one or more of four contingencies in the event of an accident: death, permanent total disability, permanent partial disability and temporary total disability (

see Defining Disability). The se are very crucial covers. Even something like temporary disability—a broken leg, a fractured arm—can dent finances. If someone breaks his leg and has to stay away from work without pay for a prolonged period, the temporary total disability cover will pay him compensation for a maximum of two years. Of course, the compensation depends on his salary and has a limit of Rs 5,000 a week.

Taking a health insurance policy does not mean that you can keep illnesses and accidents at bay. But at least you can ensure that if they strike your family, you will be able to avail the best possible treatment without having to worry about the costs.

“My health plan cushions me against the cost of treatment for my kidney and dialysis” “My health plan cushions me against the cost of treatment for my kidney and dialysis”

POORNIMA VYASULU, 53 BANGALORE |