Insurance and investment finally seem to be parting ways — in the financial portfolio of a small but growing number of Indian investors. Having blindly put money in endowment and money-back policies for decades, people are beginning to realise that these policies combined the smallest of insurance cover with the lowest of returns. Financial planners can’t stop praising term policies, which are pure insurance plans with no survival benefits — just as in the case of vehicle or medical insurance. “An individual should first opt for a pure protection plan. Other forms of insurance such as endowment policies can follow once the family’s protection has been taken care of,” says S. Krishnamurthy, MD and CEO of SBI Life Insurance.

Life insurance is the first among all investments because it protects other forms of investments. A term plan is life insurance in its simplest form: it covers the risk of a person dying early, before he has accumulated enough capital to leave for his dependants. It is a no-frills, lowcost pure risk cover. Says Rajesh Relan, managing director, Metlife: “Everyone’s insurance portfolio should comprise a term cover.”

But insurance agents are not too keen on selling term plans. Instead, they brandish money-back and endowment policies that earn them fatter commissions. Insurance companies too don’t advertise these plans aggressively because there is very little difference in basic premium rates. “I had to do a lot of scouting before I bought a Kotak Preferred Term Plan which rewards my non-smoking habit with a lesser premium,” says George Koshy, a manager in a private company.

What kinds of term plans are on offer? What should you look for when you buy one? And which is the cheapest plan? To fill the information gap on term plans, MONEY TODAY prepared a ready reckoner.

Before you buy a term plan, define the need for insurance which will define the tenure of your policy. Even if you are adequately insured, there may be circumstances in which it would be prudent to go in for an additional term cover of a shorter tenure. “When you are buying a house, especially on a huge loan, there is need to cushion the loan with a term-type insurance plan,” says Krishnamurthy.

If your insurance need goes up later in life, you can take more term plans for additional cover. For instance, if you are relying on the life insurance cover offered by your employer, a change in job could leave you uninsured. That’s when you could take a term plan to act as a bridge till you join your new employer. The minimum term for such plans is five years. But the best part is that you can terminate a term plan anytime — just don’t pay the next year’s premium and the plan ends. In endowment policies, a premature termination results in heavy losses for the policyholder. The flexibility offered by term plans is a big plus.

You can also enhance the scope of cover by attaching riders to your term plan. “You can add a health rider to a base policy and accident cover in most cases,” adds Relan. Though term-plans do offer you the cheapest insurance cover, they also come with limitations. For instance, given the nature of the policies, they do not cover you beyond the tenure of the policy. If you need an indefinite tenure policy then a whole life plan is better.

Term plans get more expensive as you age. Moreover, with age the rigours of medical tests set in too, which can hike your premium above the standard rates. Though some insurers offer to renew term policies without a medical test, they do not guarantee doing away with the medical tests completely. So, if you think you will be able to buy a term plan when the existing one expires, think again.

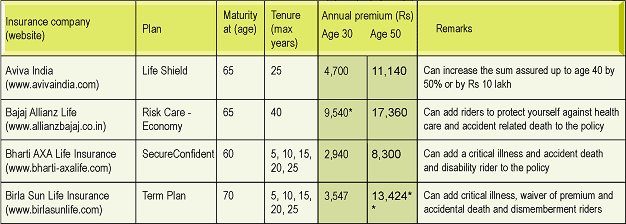

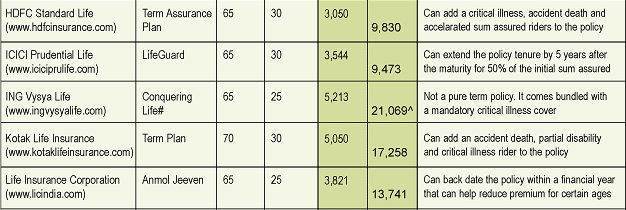

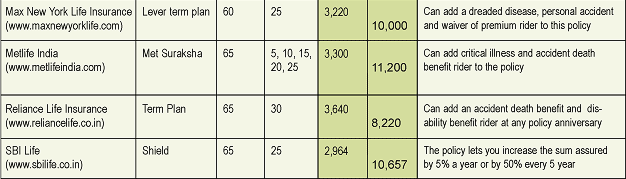

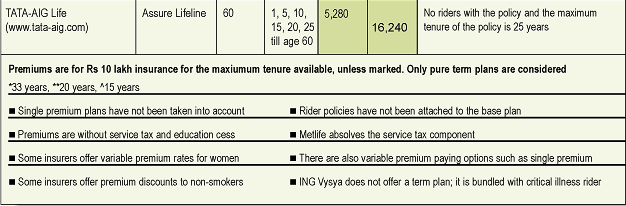

Term Insurance Options