If the economy is on a path to revival, as many believe, it is definitely not showing in corporate earnings. After many quarters of slowing down, the profit after tax (PAT) of Sensex and Nifty companies fell 6.4% and 4.8%, respectively, in the third quarter of 2014-15.

"Fading out of gains from rupee fall, which aided performance between Q2 of 2013-14 and Q1 of 2014-15, and sharp fall in commodity prices caused sales to fall for the first time since Q2 of 2009-10," says Dhananjay Sinha, head of research and strategist, Emkay Global Financial Services.

Vinay Khattar, associate director and head of research, Edelweiss, says almost all sectors lost momentum during the quarter.

"Top line of consumer goods companies is growing in single digits and HUL gained market share with just 3% volume growth. On the investment side, L&T cut its revenue guidance and highlighted weak execution," he said. Growth in key export sectors, namely information technology (IT) and pharmaceutical, also faltered due to strengthening of the rupee and slowdown in emerging markets and Europe. In banking, asset quality worsened, with managements saying stress will continue for a couple of more quarters.

Let's analyse the third quarter results of various sectors to get a better view of the corporate universe.

AUTOMOBILES

Emkay's Sinha says managements are hopeful and expect the demand momentum to continue in 2015-16. With most original equipment makers launching new platforms and products and macro environment improving, Sinha expects the coming two financial years to be even better. The top picks of most experts are Tata Motors (due to JLR launches and turnaround in the domestic commercial vehicle business), Mahindra & Mahindra, Maruti Suzuki (five launches in the coming year) and Eicher Motors (growth in Royal Enfield sales).

BANKING AND FINANCIAL SERVICES

Although earnings growth of private sector as well as PSU banks slowed, there was a wide divergence between the two categories. "The reason was 6% fall in earnings of PSU banks, even though the contribution of treasury to profit before tax was significantly higher at 35% (owing to fall in interest rates) compared to -5% in the third quarter of 2013-14. Earnings growth of private sector banks was in line with expectations at 19%," says Sinha. High provisioning, sticky operating expenditure and higher tax rate squeezed the PAT of PSU banks (except State Bank of India) by more than 50%. Bank of Baroda, for instance, saw net interest margins, or NIMs, fall by 20 basis points, or bps, to 2.2% due to rise in stressed assets. It was followed by Bank of India, whose NIMs fell 36 bps to 2% and NPAs rose to 3.5% compared to 3.2% in the second quarter of 2014-15. Punjab National Bank reported gross NPAs of 6% compared to 5% in the third quarter a year ago. Khattar says managements of PSU banks have guided for another couple of quarters of stress.

As one enters 2015-16, one can expect traction on the execution front as the government frontloads expenditure. Further, monetary easing should lower cost of funds. Some preferred stocks in the space are Cummins (ramp-up in exports and improvement in market position) and L&T (diverse skill sets and strong execution capabilities).

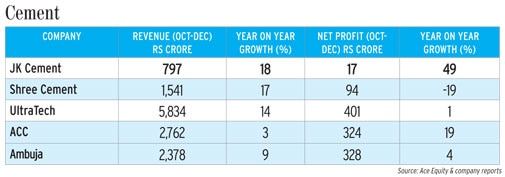

CEMENT

South-based companies (India Cement & Ramco Cement) saw 9.7% fall in sales. JK Cement reported 14% volume growth. Khattar says volumes of JK Cement, Shree Cement and UltraTech rose on account of capital expenditure and acquisitions. Drop in diesel prices reduced freight costs. Demand is expected to rise in 2015-16 and provide the companies pricing power. The top sector pick is UltraTech due to efficiency of operations and management quality. In the mid-cap space, the top pick is JK Lakshmi Cement, which has one of the most efficient operations and operates in east India, one of the most profitable regions.

INFORMATION TECHNOLOGY

"Pharmaceutical companies reported poor revenue growth due to foreign exchange volatility, instability in emerging markets of CIS, Brazil and Venezuela and regulatory issues in the US," says Sinha. But gross margins rose due to improved product mix. Lupin and Cipla saw rise in EBITDA margins due to low base. Dr Reddys' margins fell due to high base of last year. Going ahead, sales are expected to gradually recover given the positive signals from Sun Pharma and Lupin.

CONSUMER GOODS

The consumer goods sector continued to take a hit as volumes fell and consumer sentiment remained subdued. However, lower costs helped most companies expand gross margins. Growth in rural areas was higher than in urban areas. Khattar says growth for paint and chemical companies was poor due to sluggish demand in urban areas. However, the fourth quarter of 2014-15 and the first quarter of 2015-16 will see the companies expand margins as they replace their high-priced inventory.

LOOKING AHEAD

Sinha says weak earnings over the past two quarters and continued market buoyancy has created a conundrum of rising multiples even with earnings downgrades. With 5.5-6% earnings growth of Nifty and Sensex companies in the first three quarters, it is unlikely that the full-year average will be higher than 5%, much lower than the FY12-FY14 average of 10% and consensus expectation of 17-20% six months back.

R Sreesankar, head, Institutional Equities, Prabhudas Lilladher, says economic recovery is expected to happen only from the first quarter of 2015-16 and, hence, India Inc's earnings will disappoint in the next quarter as well.

"Further, with the government adhering to fiscal discipline, it will spend less in the next quarter, which could lead to disappointment in earnings across sectors, postponing recovery to the second quarter of 2015-16," he says.

All in all, what will aid earnings in 2015-16 is improvement in incomes, rise in government expenditure and lower interest rates. If these things fall into place, Khattar believes earnings could grow at 18%-20% in 2015-16 and 2016-17.