One of investors' worst nightmares may be coming to an end. With the Reserve Bank of India reducing the repo rate, at which it lends to banks, by 50 basis points, and hope of reforms and huge investments, the

infrastructure sector looks ripe for a turnaround.

Anything that can go wrong will go wrong. This is what the industry-hit by high cost of debt, shortage of funds and fuel, high coal prices and regulatory hurdles-went through in the last few quarters.

SPECIAL:

Growth-driven stocks hottest in market The

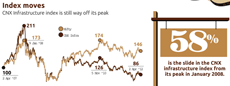

CNX infrastructure index, which comprises stocks of telecom, power, port, air, road, rail, shipping and utility companies, has slumped 58 per cent from its peak in January 2008. The Nifty has fallen 14 per cent in the period.

Between April 2007 and April 2012, the index gave -3 per cent annual return on a compounded basis compared to the Nifty's 8 per cent return.

LOSING THE PLOTBetween 2006 and January 2008, infrastructure was one bet that could not go wrong. In 2007, for instance, funds like Canara Robeco Infrastructure Fund and ICICI Prudential Infrastructure Fund gave returns of 90 per cent and 92 per cent, respectively. Needless to say, scores of such funds were launched to cash in on the euphoria.

Lower import duty on coal will benefit Adani Power, Tata Power and Reliance Power.

"In the pre-Lehman crisis era, funding was easily available and there was boom all around," says IV Subramaniam, director & CIO, Quantum AMC. One reason was that investment growth in five years preceding the 2008 financial crisis was in double digits while the economy grew over 9 per cent for three consecutive years.

However, things changed fast. "In the last one year, there has seen a sharp correction owing to investment slowdown and monetary tightening," says Sivasubramanian KN, CIO, Franklin Equity India, Franklin Templeton Investments.

REFORM TIMEIt is now well-recognised that good infrastructure is a necessary condition for progress. "There is a also a renewed effort to shake off the perception of policy gridlock with announcements on coal linkages," says Sivasubramanian.

For instance, in the Union Budget, the finance minister proposed waiver of import duty on coal, the most widely used fuel to generate power. This will lower costs and benefit Adani Power, Tata Power and Reliance Power.

Index moves: CNX Infrastructure index is still way off its peak

The government has also asked Coal India to sign agreements with power producers to supply coal at 70 per cent less than market prices. This will be a boon for power companies. The decision has revived investor confidence as fuel supply is the biggest problem that power companies face.

Subramaniam says power companies, especially in niche areas such as generators, turbines and transmission, will gain the most from increased infrastructure spending. This is because niche businesses can have 15-20 per cent margins and entry barriers are high.

"Power distribution and generation are great businesses at good valuations considering that the need for power in India is very high," he says.

"Investors will be better off with government power companies as a lot of nagatives have been priced in," says Pankaj Pandey, head of research, ICICI Securities.

INVESTMENT BOOSTThe government aims to spend Rs 50 lakh crore on infrastructure in the 12th Five-Year Plan period (the 11th Plan figure was Rs 20 lakh crore). Almost 60 per cent-70 per cent of this will be on roads and power, which will benefit companies such as L&T (a conglomerate with businesses across the infrastructure space), BHEL (the largest power equipment maker) and IRB Infra (road construction and built-operate-transfer projects).

Another positive is the move to double the limit of tax-free bonds to Rs 60,000 crore this year. This includes Rs 10,000 crore each for roads and power and Rs 5,000 crore for ports. Key beneficiaries of this, say analysts, will be Power Finance Corporation, REC and IDFC.

"The whole value chain in the port sector, right from those who construct ports to operators and logistics companies, too, will benefit," says Subramaniam. Logistics companies include Concor while Gujarat Pipavav, Mundra and Adani are a few big names that operate ports.

Investors will be better off with government power companies since most stocks have priced in a lot of negatives.

PANKAJ PANDEY

Head of Research, ICICI Securities

The cement industry, on its part, will benefit from a pick-up in construction because of the above factors. In 2011, cement was among the better performing sectors after consumer staples.

In 2009-10, there was fear of overcapacity and increase in power and energy costs. However, cement dispatches grew in double digits (12 per cent) in March 2012 for the fourth consecutive month on pick-up in construction activity. But Subramaniam believes that prices of cement stocks have run up considerably.

CAVEATIn spite of all these positives, the sector could face bottlenecks such as high funding cost, fuel supply and delays. Further, lowering of interest rates will ensure cheaper funding and improve margins.

Should you adopt a sectoral approach? Subramaniam says should not go for sector funds. This is because there may be periods when the business will do badly. A diversified fund will give exposure to the infrastructure sector as well.

"Investors are better off focusing on companies with long-term growth potential rather than adopting a top-down approach," says Sivasubramanian of Franklin Templeton.

TOP INFRA PICKS

The Union government aims to spend Rs 50 lakh crore on infrastructure in the 12th Five-Year Plan

Larsen & Toubro

CMP: 1,358 | Target: 1,474

Trading at an attractive valuation of 17.7x 2012-13 and 15.8x 2013-14 earning per share (standalone business). L&T has been able to expand order book consistently despite a weak investment cycle (42 per cent year-on-year growth in the last crisis phase of 2009-10 and 27 per cent in the first nine months of 2011-12).

Presence across segments and geographies, strong balance sheet, reliability in execution and ability to monetise the revival in the investment cycle will ensure that L&T is well-placed to meet its 2011-12 revenue guidance of 25 per cent year-on-year growth where its peers are facing shrinking order books and volatility in earnings. Value unlocking in subsidiaries will offer a huge upside as L&T has invested about Rs 7,400 crore in various strategic subsidiaries.

Jaiprakash Associates Ltd

CMP: 88 | Target: 95

Trading at an attractive valuation of 1.7x 2012-13 price-to-book value (P/BV). Has presence across the value chain of infrastructure, that is, cement, power, roads and real estate, with strong execution capabilities in the construction business. Significant rise in the cement market share (10 per cent). Well-funded Yamuna Expressway with significant monetisation potential in the real estate business (both Yamuna Expressway & Jaypee Sports) and aggressive expansion plans in power (3,800 MW) over the next couple of years will lead to strong earnings growth.

NTPC

CMP: 167 | Target: 185

Trading at 2.1x P/BV FY12E and 1.9x P/BV FY13E. It is India's largest utility with market share of 20 per cent installed capacity. Superior execution (in terms of commercialisation of power capacities) and higher plant availability factor could lead to re-rating of the stock The regulated nature of its business is a positive as all capacity addition plans are backed by fuel security.

*CMP is current market price on 3 April 2012; Recommendations by ICICI Securities